Bloom Energy (BE) has been one of the standout stocks in clean power, despite a short seller trying to dim the spotlight last week. On July 8, shares dropped about 12% after Hunterbrook released a report titled “Bloom’s Big Lie.”

In the report, Hunterbrook accused Bloom of downplaying how much it relies on Chinese supply chains for scandium oxide, a key input for its fuel cells. That hit follows Bloom signing big fuel‑cell and clean‑power deals with AI hyperscalers like Oracle (ORCL) earlier this year.

The market’s reaction to the report was quick and surprisingly forgiving. After Bloom firmly rejected the allegations as “false and misleading,” BE stock bounced back with a solid move higher on July 9.

The short attack still exposed possible weak spots in its supply story, so investors are right to pause. Now the real question is whether Bloom is genuinely in the clear or if some bigger risks are still hiding beneath its big run. Let’s dive in.

Bloom’s Price Runway

With a market capitalization of about $70 billion, Bloom Energy makes solid‑oxide fuel‑cell systems that supply on‑site electricity to commercial and industrial clients. The company is based in San Jose, California.

On July 9, BE stock closed at $257.02, adding a modest 1% that day. Despite falling in the two trading sessions since then, share are still up 169% year‑to‑date (YTD) and 819% over the past 52 weeks.

Bloom Energy does have a premium valuation, trading at 514 times trailing earnings and 184 times forward earnings. But it also helps to look at what the business reported before the narrative shifted.

The quarter ended March 2026 delivered diluted EPS of $0.23. The same report also showed sales of about $751.1 million, with sales declining about 3% sequentially, so revenue dipped even as the share price climbed. Net income for the period reached roughly $70.6 million, representing huge growth from a net loss of $23.8 million in the prior-year period.

Finally, quarterly cash figures add an important final detail to Bloom's financial picture. Operating cash flow came in at about $73.6 million while net cash flow was roughly $36.7 million.

Hunterbrook’s Claims Versus Bloom’s Expansion

The recent Hunterbrook report claims that Bloom Energy has told investors it has “no China supply chain” and is “not dependent on China for scandium,” yet still uses scandium linked to Chinese sources. The report also argues that Bloom’s 5 GW production goal would see the company run into scandium oxide supply issues, which naturally raises doubts about how realistic that target is.

Bloom has pushed back hard. In an 8‑K filing, the company called the allegations “false and misleading" and said it holds enough scandium inventory that does not depend on China, going straight at the heart of the short thesis. The filing pointed to a diversified supply base built over many years instead of relying on one country, and is clearly meant to reassure investors that Bloom can meet demand.

The growth story sitting behind this fight is tied closely to AI infrastructure. Bloom and Brookfield (BN) have put together a financing framework of up to $25 billion for fuel‑cell projects that power AI data centers, up from an earlier $5 billion agreement. That setup is meant to support the fast buildout of Bloom systems at AI sites around the world, with Brookfield bringing the capital.

Another big piece is Bloom’s work with Oracle. Under an expanded deal, Oracle plans to buy up to 2.8 GW of Bloom fuel‑cell capacity for its AI and cloud data centers, with an initial 1.2 GW already signed and moving into deployment. The arrangement is built to give Oracle on‑site, dispatchable power that can speed up how quickly new sites get energized.

This kind of large‑scale rollout is exactly what makes Hunterbrook’s questions about scandium sourcing and long‑term supply availability so important for investors.

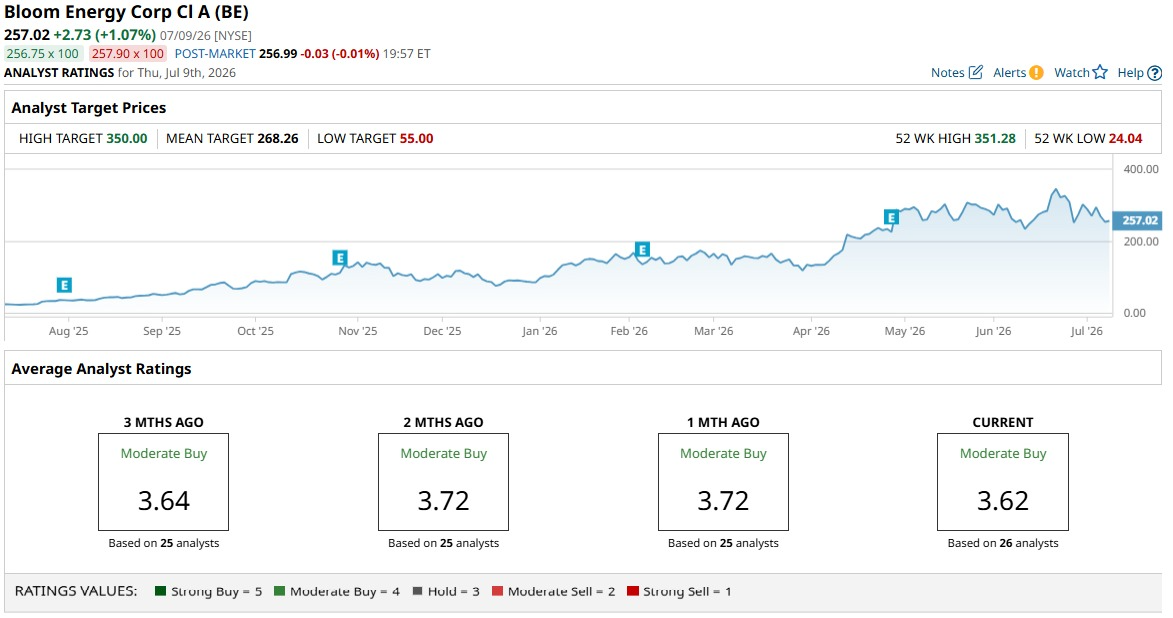

Wall Street Still Leans Bullish on BE Stock

The next big check‑in for this story is already set. Bloom Energy will report its next quarter on July 28, and analysts are looking for EPS of $0.23 for the June 2026 quarter. That would flip from a loss of $0.03 a year earlier and work out to an expected year‑over‑year (YOY) growth rate of more than 860%.

That kind of jump helps explain why some firms are sticking with bullish calls even after the scandium noise. Baird recently reiterated an “Outperform” rating on BE stock and kept a $310 price target, while still noting the supply‑chain concerns in the background. UBS also weighed in this month and raised its target to $350, keeping a “Buy” rating in place.

Putting all of that together, the overall view from Wall Street is still fairly positive. Bloom Energy stocks holds a consensus “Moderate Buy” rating based on 26 analysts. The average price target sits at $271.74, implying roughly 16% potential upside from current levels.

Conclusion

Right now, Bloom Energy looks bruised but not broken, and the market’s reaction backs that up. Hunterbrook has hit a real pressure point around scandium, yet fundamentals, AI upside, and analyst support still lean toward the bull side. BE stock is more likely to drift higher than unravel from here, with headlines and the next earnings report doing most of the steering.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.