UBS raised its price target on Bloom Energy (BE) shares to $350 while maintaining a “Buy” rating on Wednesday, a move driven by the firm’s expanding financing partnership with Brookfield Asset Management. Brookfield has raised its committed funding framework to $25 billion, representing a five-fold increase since the original partnership was established in October 2025.

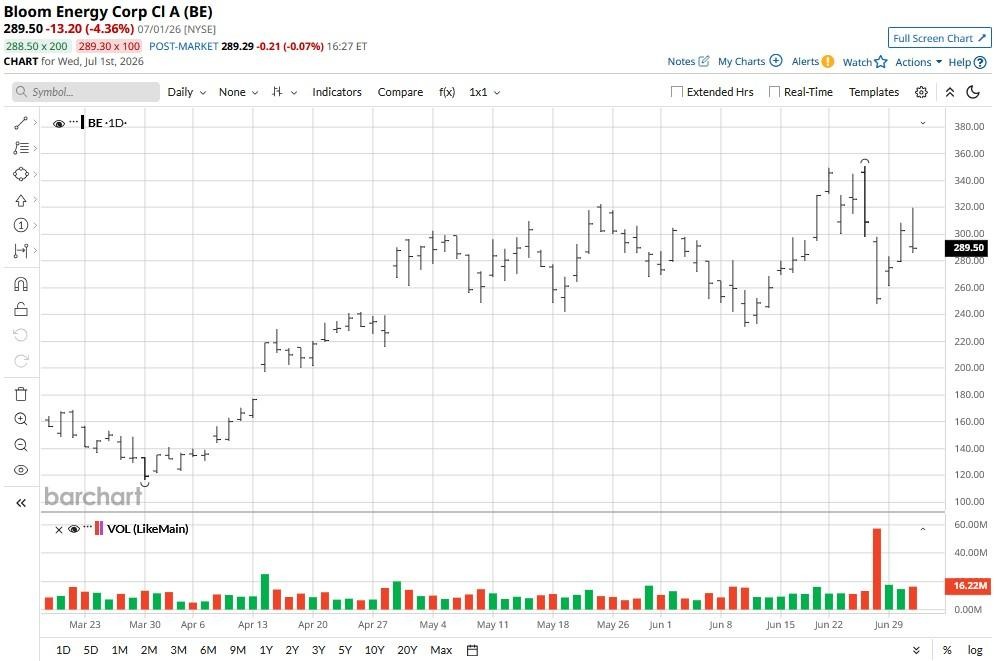

This expansion signals growing institutional confidence in BE’s position as a critical infrastructure provider for the AI data center buildout. Bloom Energy stock is currently trading at nearly 3x its price at the start of 2026.

What UBS’s Bullish View Is Based On

The core thesis behind UBS’s bullish stance centers on Bloom Energy’s ability to deliver reliable, dispatchable power through its solid oxide fuel cell tech, which converts natural gas or hydrogen into electricity through a non-combustion process.

This onsite power generation capability addresses a fundamental bottleneck for hyperscalers and AI infrastructure developers who need fast, dependable energy without relying on increasingly strained electrical grids.

UBS also referenced regulatory modifications enabling faster connection of major energy consumers to the national transmission infrastructure as supportive of Bloom’s growth trajectory.

Financials Warrant Buying BE Shares

Bloom Energy’s financial performance validates the optimism, with Q1 sales surging 130% year-over-year to $751 million and management raising full-year guidance to a minimum of $3.4 billion.

The company’s product backlog stands at $6 billion, with a total backlog of a whopping $20 billion, underpinned by major partnerships with Oracle (ORCL), Nebius (NBIS), and now the significantly enlarged Brookfield arrangement.

BE demonstrated execution capability by delivering its first fuel cell system to Oracle in 55 days, well ahead of the 90-day target, which convinced ORCL to expand its agreement to acquire up to 2.8 gigawatts of capacity.

Valuation Remains an Overhang on Bloom Energy Stock

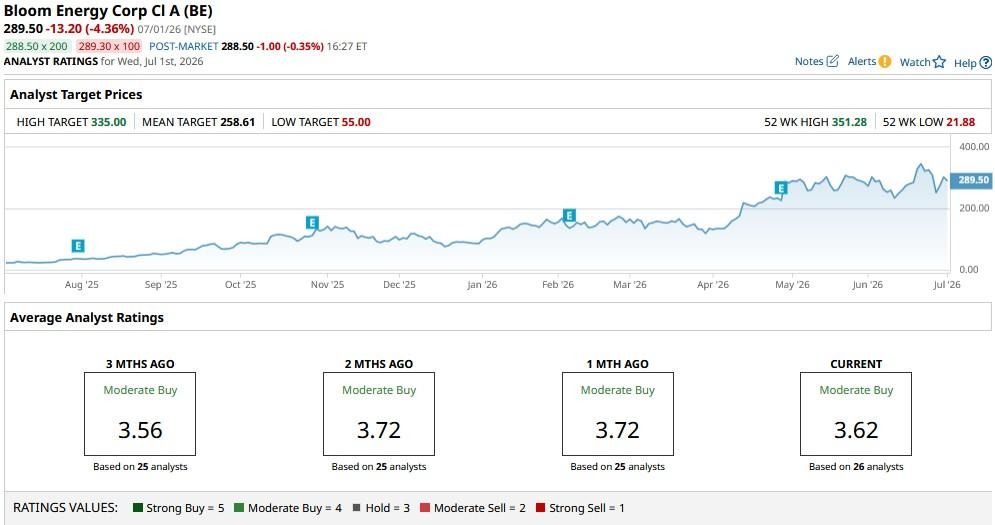

UBS was not alone in raising its target for the clean energy company, as Evercore ISI also moved to $350 with an “Outperform” rating, while Clear Street raised to $290 from $250 but maintained a “Hold” because of valuation concerns.

The $25 billion Brookfield framework, sourced from its AI Infrastructure Fund targeting $100 billion in total deployments, positions BE as a preferred tech partner in what Brookfield estimates will be a multi-trillion-dollar AI infrastructure spending cycle.

However, BMO Capital cautioned that the commitment represents a programmatic financing framework rather than confirmed immediate backlog, reiterating its “Market Perform” rating with a $279 target.

All in all, the valuation debate remains intense, with BE stock trading at about 39x sales and over 210x forward earnings — levels that some analysts consider unsustainable despite the exceptional growth rate.

While the consensus rating on Bloom Energy shares remains at “Moderate Buy,” the mean price target of nearly $259 actually signals potential downside from current levels.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)