Insurance company Progressive (NYSE:PGR) will be reporting results this Wednesday before market open. Here’s what to look for.

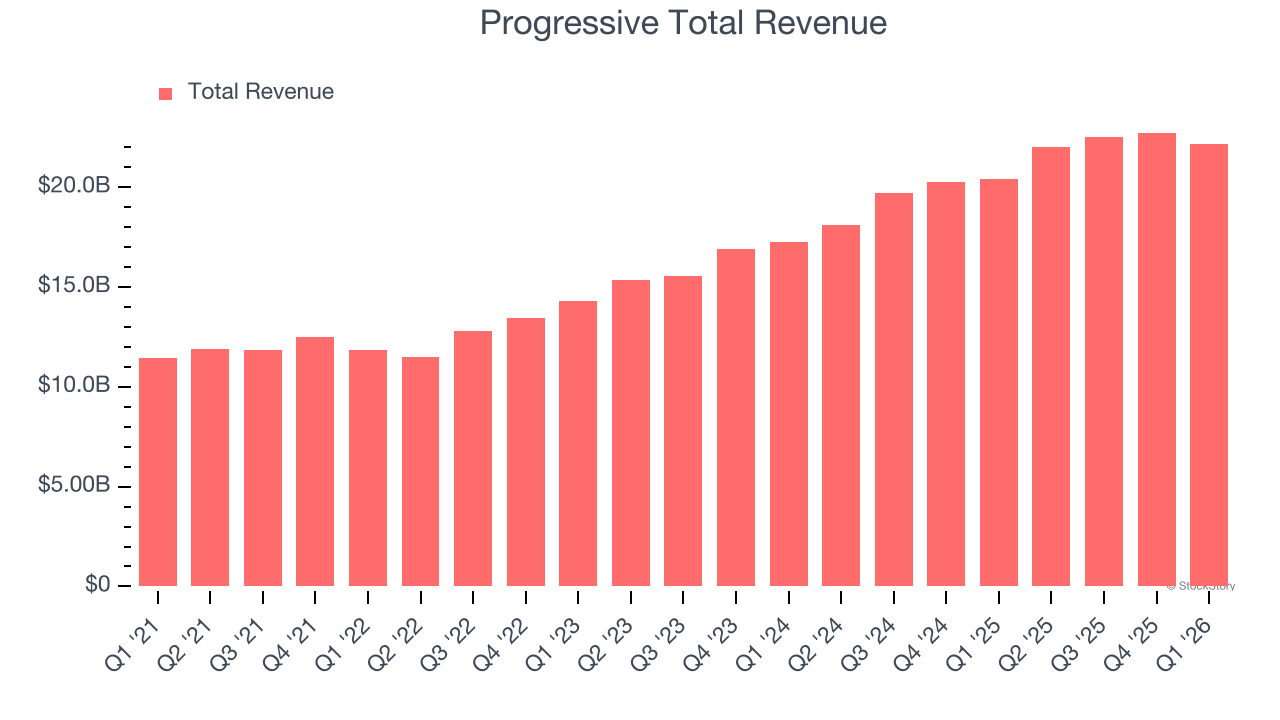

Progressive met analysts’ revenue expectations last quarter, reporting revenues of $22.19 billion, up 8.7% year on year. It was a slower quarter for the company, with a miss of analysts’ book value per share estimates and a narrow beat of analysts’ EPS estimates.

Is Progressive a buy or sell going into earnings? Read our full analysis here, it’s free for active Edge members.

This quarter, the market is expecting Progressive’s revenue to grow 7.8% year on year, slowing from the 21.3% increase it recorded in the same quarter last year.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business will stay the course heading into earnings. Progressive has missed Wall Street’s revenue estimates multiple times over the last two years.

With Progressive being the first among its peers to report earnings this season, we don’t have anywhere else to look to get a hint at how this quarter will unfold for insurance stocks. However, there has been positive investor sentiment in the segment, with share prices up 9.9% on average over the last month. Progressive is up 15.5% during the same time .

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)