The fertilizer market has been volatile in 2026, with prices moving higher due to geopolitical tensions affecting key shipping routes like the Strait of Hormuz. These disruptions have raised concerns about supply and pushed up costs for agricultural inputs.

At the same time, strong crop prices, solid farm margins, and low inventories have kept global demand firm for nutrients like phosphate and potash. Nitrogen products such as ammonia have also seen strong price gains in the first quarter. Higher fertilizer costs are now feeding into grain and oilseed markets, raising production expenses and highlighting the advantage of efficient North American producers.

Yet even in this difficult environment, CF Industries Holdings (CF), a leading North American nitrogen fertilizer producer, recently raised its quarterly dividend by 20% to $0.60 per share (annualized $2.40, up from the prior $2.00 run rate). The new dividend is payable on Aug. 31, to shareholders of record as of August 14. The stock has also delivered strong returns, climbing 55% year-to-date (YTD).

With that kind of performance and a higher dividend, what is driving CF Industries, and can it keep going?

Financial Strength Behind the Surge

CF Industries is one of the major producers of nitrogen fertilizers, making products like ammonia and urea that farmers rely upon. Its costs are closely tied to natural gas, which plays a big role in its profitability.

The stock has reflected that strength. Shares are up 22.3% over the past year and have jumped 55% so far in 2026.

Even after that run, valuation still looks reasonable, with a forward price-to-earnings ratio of 7.19 times compared to the sector average of 15.45 times.

And, CF Industries is returning more cash to shareholders. It raised its dividend by 20%, bringing the quarterly payout to $0.60. That puts the yield around 1.71%, below the sector average of 2.82%.But the payout ratio is just 19.22%, which leaves room for sustainability. The company is also buying back stock, spending $15 million to repurchase about 155,000 shares in Q1.

Results remain strong. First-quarter 2026 net income came in at $615 million, or $3.98 per share, with EBITDA of $1.01 billion and adjusted EBITDA of $983 million, helped by a $170 million litigation gain. Over the past 12 months, the company generated $2.66 billion in operating cash flow and $1.65 billion in free cash flow, even while investing in projects like the Blue Point joint venture. Production has also been solid, with ammonia output at 2.5 million tons and operating at 99% capacity, though full-year production is expected at 9.5 million tons due to the Yazoo City outage.

Core Drivers Powering Growth

CF Industries is working with POET and several major U.S. agricultural cooperatives on a pilot program for low-carbon fertilizer. The goal is to track the fertilizer from CF’s production sites through distributors and retailers to corn farmers in Iowa, Minnesota, Missouri, and Nebraska. POET will then use corn grown with CF Industries' low-carbon ammonia at its plants in Minnesota, Iowa, and Nebraska. POET expects this corn to produce an estimated 555–666 million gallons of lower-carbon ethanol. The first shipments and applications of the low-carbon ammonia were completed in late 2025, giving the partners an early test of the effectiveness of the supply chain's work.

CF Industries is putting capital behind lower-emission ammonia production. In Q1 2026, the company directed $65 million of its $223 million in total capital spending to the Blue Point joint venture. The project involves an autothermal reforming ammonia plant at the company’s Blue Point Complex in Louisiana. It is designed to produce ammonia with lower emissions while adding production capacity. Announced in 2025, the project gives CF Industries a way to meet demand for lower-carbon fertilizer and ammonia used in industrial markets without losing its focus on keeping costs competitive.

What Analysts Are Saying

CF Industries will report its next earnings after the market closes on Aug. 5, 2026. Analysts expect the company to earn $5.71 per share for the June quarter, up 140.93% from $2.37 in the same period last year. For full-year 2026, the consensus estimate is $15.86 per share, up 69.26% from $9.37 in 2025.

Some analysts remain bullish. Wells Fargo analyst Michael Sison kept an “Overweight” rating in March and raised his price target from $113 to $150, a 32.74% increase and the highest target on Wall Street at the time.

On June 29, Scotiabank analyst Ben Isaacson upgraded CF Industries from “Sector Perform” to “Sector Outperform” and raised his target from $120 to $125. He expects reduced planted acreage to support grain and oilseed prices, which could help fertilizer demand. Isaacson also said urea prices had fallen too far, leaving room for a rebound, while ammonia demand remains strong. His call came just days before CF Industries raised its dividend.

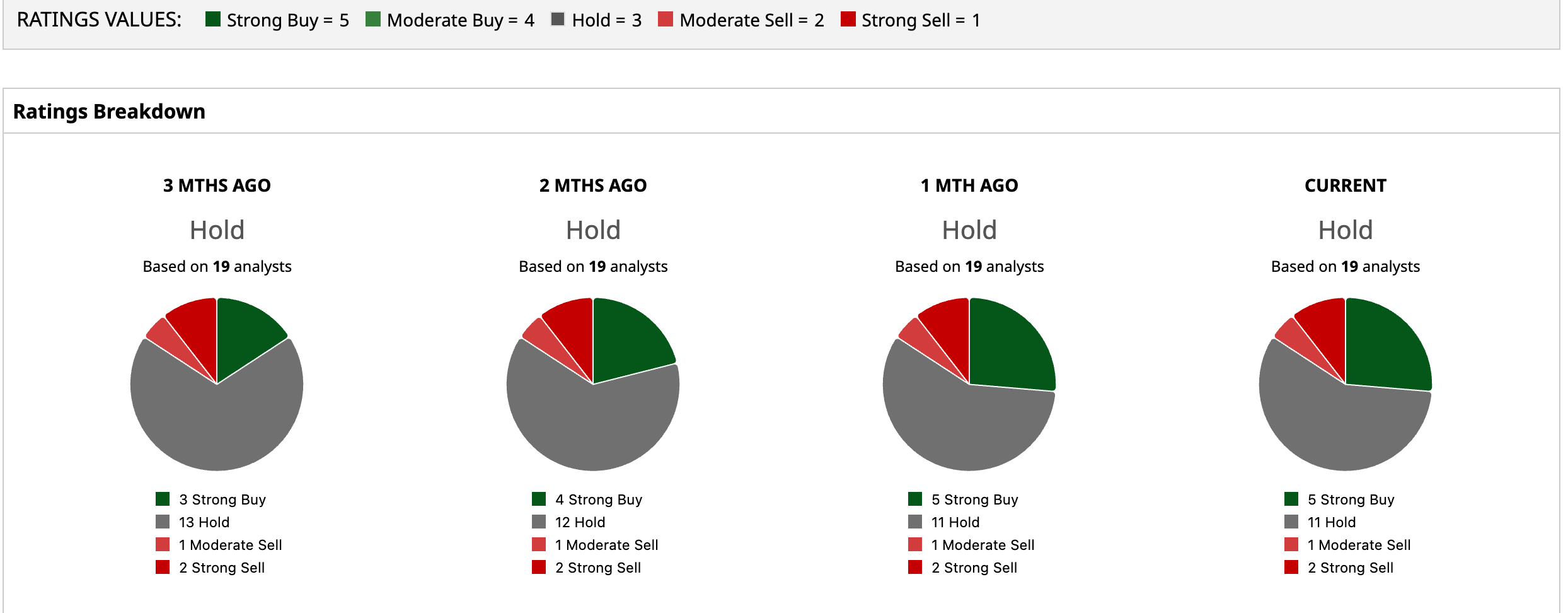

Still, the broader analyst view is cautious. All 19 analysts covering CF Industries rate the stock a consensus “Hold.” Their average price target is $120.37, nearly in line with recent price levels.

Conclusion

CF Industries is delivering exactly what this cycle rewards: strong cash flow, disciplined capital returns, and clear exposure to tight fertilizer markets. The dividend hike reinforces confidence, but with the stock already up 55% this year and analysts largely neutral, much of that strength looks priced in. Near term, shares likely to move sideways with a slight upward bias if nitrogen pricing and farm economics stay supportive. The bigger upside case depends on sustained pricing power and execution on low-carbon initiatives, while any pullback in fertilizer prices could quickly cap further gains.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)