/Phone%20and%20computer%20internet%20network%20by%20Pinkypills%20via%20iStock.jpg)

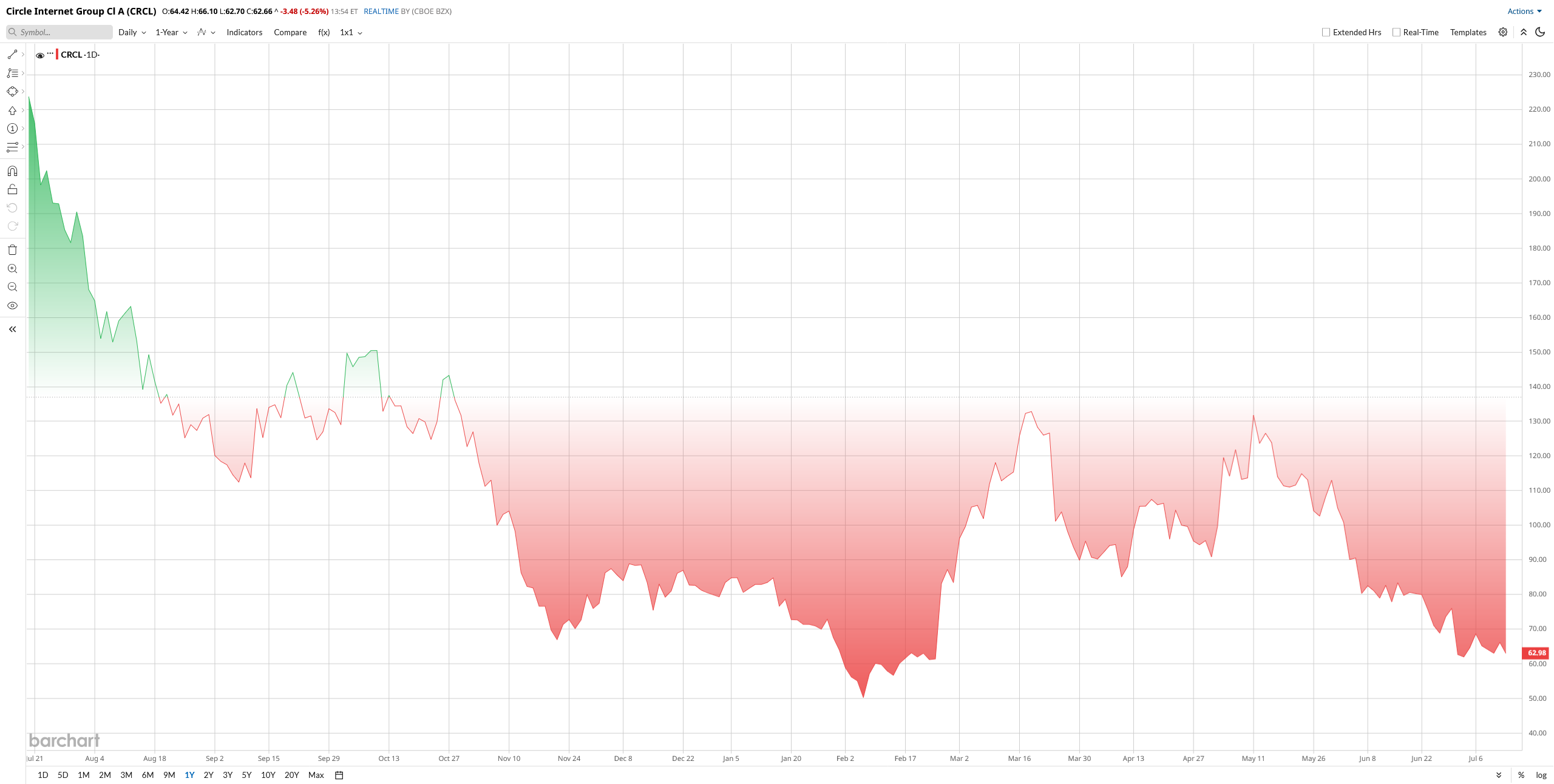

Circle (CRCL) stock is back in the spotlight after the Office of the Comptroller of the Currency (OCC) approved the company's application to establish Circle National Trust. The regulatory milestone sent shares up about 5% on Friday's trade as investors welcomed the prospect of Circle operating a federally regulated trust bank that can directly custody USDC reserves.

The move will further bolster Circle's market share in the fast-growing stablecoin segment and has sparked renewed hope in its future expansion. For investors, however, the crucial question is whether this is a sea change or a trend that will keep going higher.

Despite the positive news, CRCL stock remains down 66% over the past year and has dipped another 5% today, significantly underperforming the broader market.

The OCC Approval Could Strengthen Circle’s Competitive Position

The new trust charter represents one of the biggest developments for Circle since becoming a public company.

Once operational, Circle National Trust will allow the company to safeguard USDC reserves under federal oversight rather than relying entirely on third-party custodians. That should improve transparency, strengthen institutional confidence, and make Circle more attractive to banks, payment providers, and large enterprises looking to adopt stablecoins.

CEO Jeremy Allaire called the approval a defining moment that brings blockchain-based financial infrastructure closer to the traditional banking system. The charter also arrives as regulators become increasingly supportive of stablecoin oversight, giving Circle an advantage as institutions look for compliant digital payment solutions.

Quarterly Results Showed Growth, Although Profitability Remains Under Pressure

Circle's first-quarter 2026 results demonstrated that demand for its business continues to expand.

Revenue climbed 20% year-over-year (YoY) to approximately $694 million, driven primarily by higher reserve income from USDC and continued growth across its services business. Adjusted EBITDA increased 24% to roughly $151 million, reflecting healthy operating momentum.

However, higher distribution costs tied to expanding USDC circulation, along with increased operating expenses and stock-based compensation, weighed on the bottom line. Net income declined to $55 million from $65 million a year earlier, while adjusted earnings per share of approximately $0.21 came in slightly below Wall Street expectations.

Circle also finished the quarter with around $1.5 billion in cash and equivalents, leaving the company with a solid balance sheet as it continues investing in future growth initiatives.

Circle Is Building Far More Than Just a Stablecoin Business

The OCC approval is only one piece of Circle's broader strategy. The company continues expanding beyond USDC through its Arc blockchain network, which recently completed a successful token presale raising roughly $222 million ahead of its expected mainnet launch later this year.

International expansion remains another priority. Earlier this year, Circle signed a memorandum of understanding with Nomura to explore blockchain-powered payments, settlements, and collateral management using USDC.

All these, combined with regulatory approvals in markets including Singapore and the UAE, mean the company is steadily building a global digital financial infrastructure business rather than relying solely on stablecoin issuance.

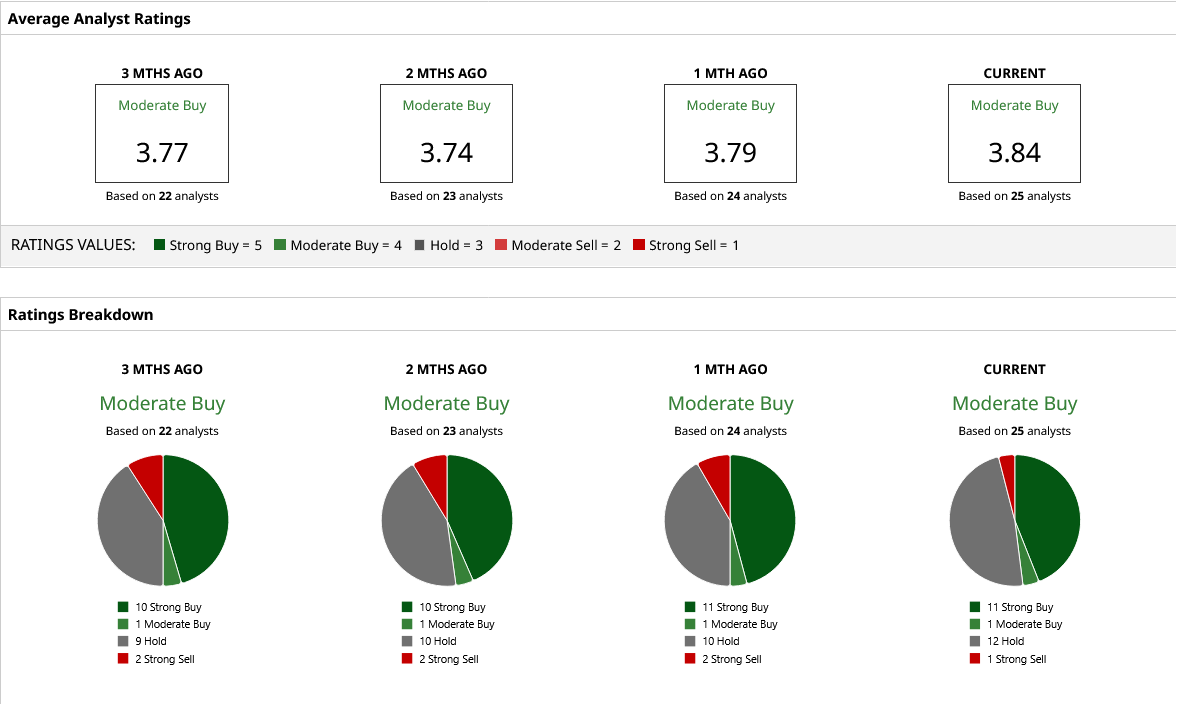

Wall Street Remains Optimistic About CRCL Stock

Wall Street generally believes the OCC approval strengthens Circle's long-term investment case.

The consensus rating remains a “Moderate Buy,” with analysts' average 12-month price target sitting around $135, implying significant upside of 114% from current trading levels.

Separately, Morgan Stanley maintained an “Equal-Weight” rating with a $106 target, while H.C. Wainwright raised its target to $150 after becoming more constructive on the company's outlook.

Needham also raised its price target to $150, pointing to Circle's expanding product portfolio and banking ambitions. Aletheia Capital is even more bullish with a target near $160, citing the company's growing platform, regulatory progress, and expanding institutional opportunity.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)