/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

Salesforce (CRM) has landed another high-profile government contract, adding fresh momentum to its growing presence in the defense sector. The cloud software giant has been selected by the U.S. Air Force's 441st Vehicle Support Chain Operations Squadron to modernize and manage its $13.5 billion fleet of more than 84,000 vehicles using its Missionforce National Security platform. The deployment will replace legacy systems with artificial intelligence (AI)-powered, cloud-based applications designed to improve fleet visibility, predictive maintenance, logistics, and mission readiness, highlighting Salesforce's expanding role in mission-critical government operations.

Moreover, the award reinforces Salesforce's strategy of diversifying beyond enterprise customer relationship management software into the lucrative public-sector and defense markets, where long-term contracts can provide durable, recurring revenue streams. Coming alongside other recent Department of Defense wins, including Air Force and Army agreements, the latest contract underscores the company's growing competitive position in government cloud and AI solutions.

So, now let’s analyze whether this defense momentum can become a meaningful catalyst for CRM stock after its recent stressed performance and whether investors should view the shares as a buying opportunity.

About Salesforce Stock

Headquartered in the iconic Salesforce Tower in San Francisco, California., Salesforce is a leading global provider of cloud-based customer relationship management software.

Salesforce’s market cap stands at $133.1 billion, reflecting its status as one of the most valuable enterprise software companies globally. With its comprehensive platform, innovative technology, and scalable business model, Salesforce remains at the forefront of enterprise digital transformation.

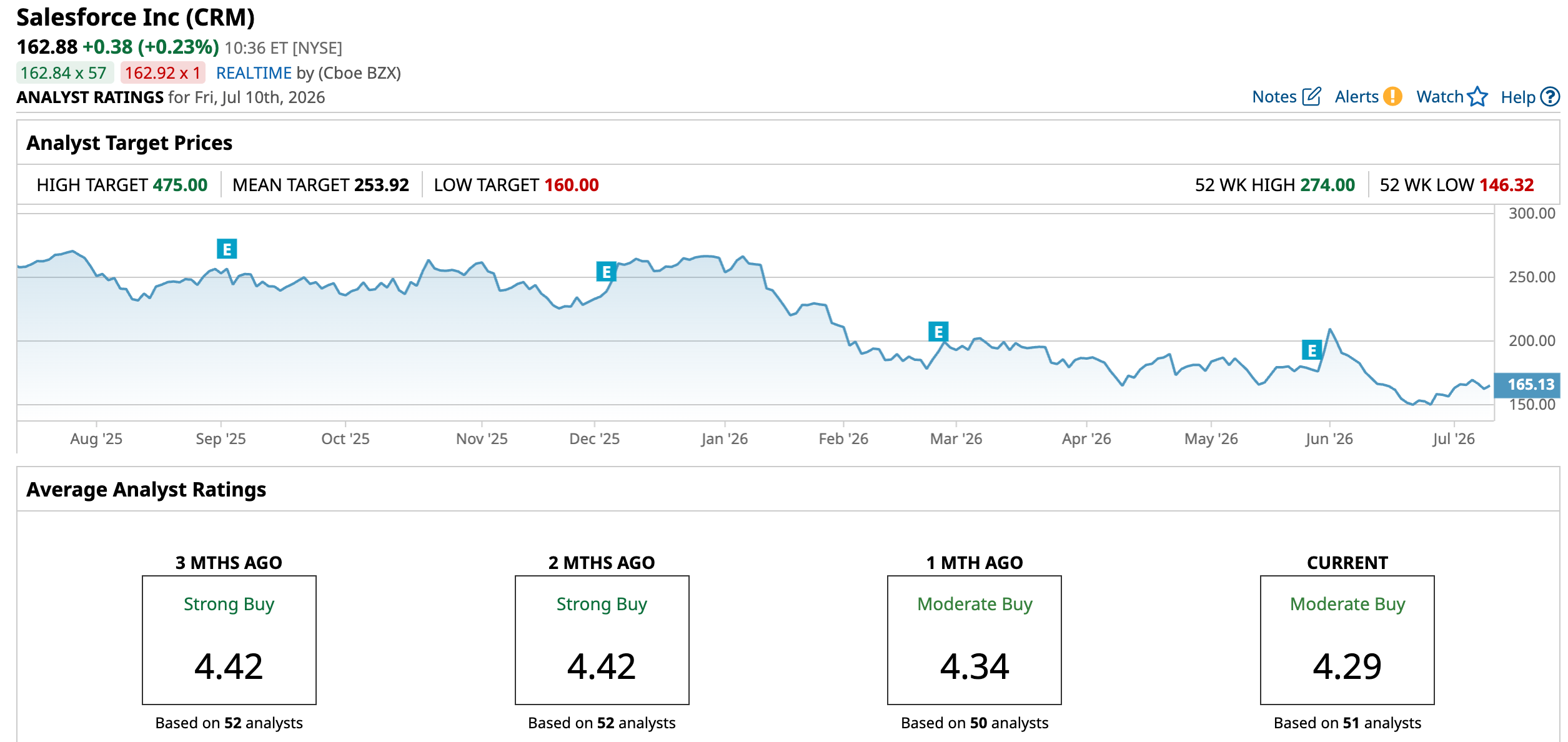

Salesforce shares have been under significant pressure in 2026, reflecting broader investor concerns over slowing software spending and the long-term impact of generative AI on the enterprise software industry. The stock has fallen 37.57% over the past year and is down about 37.8% year-to-date (YTD), making it one of the weakest performers among large-cap software companies. After an extended sell-off, CRM hit a 52-week low of $146.32 on June 22, as investors rotated away from software stocks despite the company's solid fundamentals and AI initiatives.

Notably, Salesforce's selection by the U.S. Air Force to modernize its $13.5 billion vehicle fleet failed to spark a meaningful rally in the stock. The stock has instead dipped 1.7% on July 8 and again 2.5% on July 9.

Despite the contract reinforcing Salesforce's growing presence in the government and defense markets, investor sentiment remained focused on broader concerns surrounding AI monetization, enterprise software demand, and competitive pressures.

CRM currently trades at a discount compared to the sector median and its own historical average at 16.18 times forward price-to-earnings.

Steady Q1 Results

Salesforce reported first-quarter fiscal 2027 results on May 27, delivering double-digit revenue growth and strong margin expansion, driven by continued enterprise demand and accelerating adoption of its AI offerings, including Agentforce and Data Cloud.

Total revenue increased 13% year-over-year (YOY) to a record $11.1 billion, while subscription and support revenue, the company's largest business rose 14% to $10.6 billion. Current remaining performance obligation (cRPO), a key indicator of future revenue, climbed 14% to $33.6 billion, while total remaining performance obligation (RPO) increased 11% to $67.9 billion.

Its Non-GAAP EPS jumped 50% to $3.88, above expectations, while the company also reported a 34.8% Non-GAAP operating margin, reflecting continued expense discipline and operating leverage. Meanwhile, the company saw Agentforce and Data 360 annual recurring revenue (ARR) coming in at $3.4 billion, up over 200% YOY, while Public Sector Industry Cloud ARR was over $2 billion, up 23% YOY in Q1.

Furthermore, Salesforce guided for second-quarter fiscal 2027 revenue of $11.27 billion to $11.35 billion, representing 10% to 11% YOY growth, with Non-GAAP EPS of $3.25 to $3.27. Management also raised its full-year fiscal 2027 revenue outlook to $45.9 billion to $46.2 billion, implying approximately 11% YOY growth, while maintaining its Non-GAAP operating margin guidance of 34.3%.

Analysts predict EPS to rise 6.1% YOY to $10.29 in fiscal 2027, and surge by 7.6% annually to $11.07 in fiscal 2028.

What Do Analysts Expect for Salesforce Stock?

Analyst sentiment on Salesforce turned mixed on July 9 when KeyBanc Capital Markets downgraded CRM to "Sector Weight" from "Overweight."

The downgrade came just over a week after Guggenheim upgraded Salesforce to "Buy" from "Neutral" on July 1, assigning a $228 price target. Guggenheim argued that the stock's steep sell-off had become excessive.

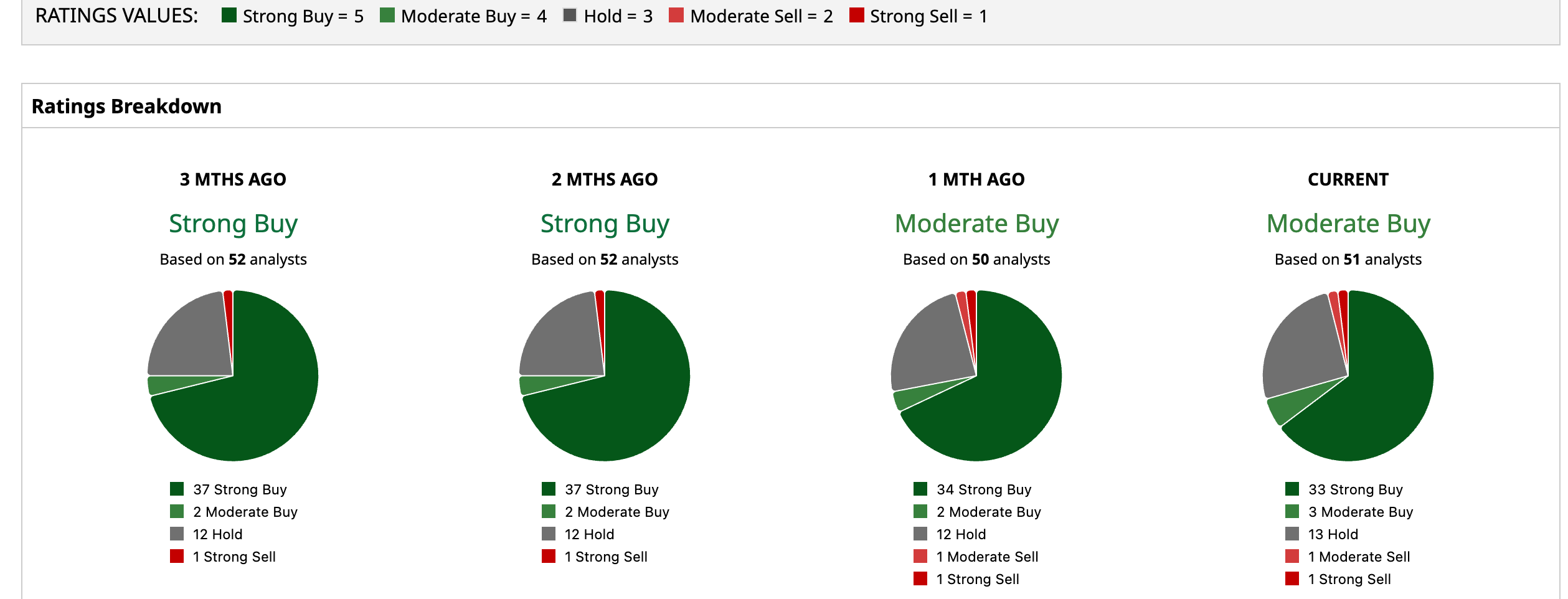

Wall Street is cautiously bullish on CRM. Overall, CRM has a consensus “Moderate Buy” rating. Of the 51 analysts covering the stock, 33 advise a “Strong Buy,” three suggest a “Moderate Buy,” and 13 analysts are on the sidelines, giving it a “Hold” rating, one recommends it a “Moderate Sell,” and one rate it as a “Strong Sell.”

The average analyst price target for CRM is $253.92, indicating a potential upside of 55.9%. The Street-high target price of $475 suggests that the stock could rally as much as 191.6%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)