/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

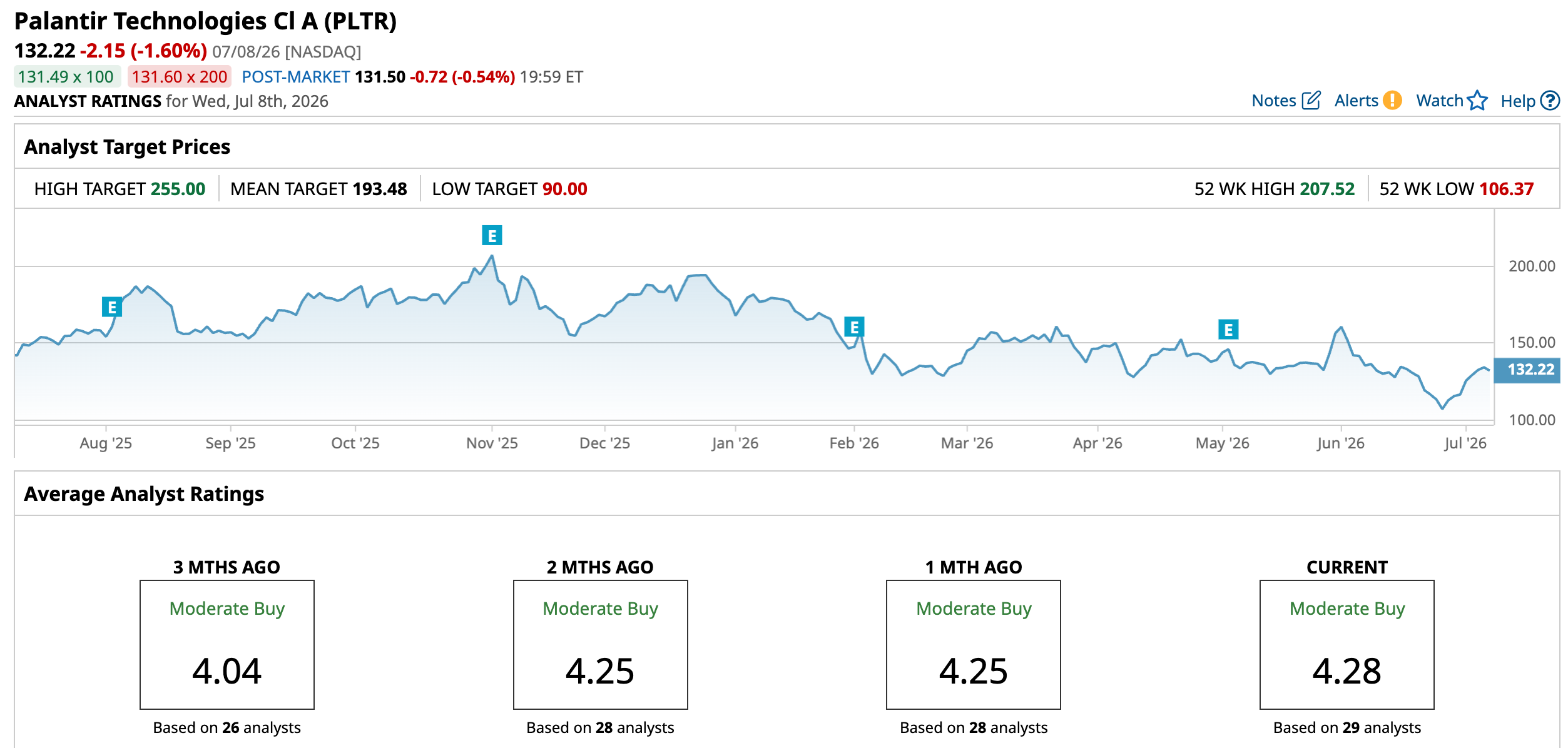

Palantir Technologies (PLTR) stock has been under pressure in 2026. The enterprise AI software company's shares have fallen 25.6% year-to-date (YTD), significantly lagging the broader S&P 500 Index ($SPX). Furthermore, the stock is trading 36.3% below its 52-week high of $207.52.

The steep decline was largely driven by Palantir's premium valuation relative to its peers and growing competition from AI companies.

However, the sell-off has made Palantir’s valuation more reasonable. At the same time, the company's accelerating growth has improved its risk-reward profile, making the shares more attractive than they were earlier in the year.

Palantir's Growth Engine Has Shifted To a Higher Gear

Palantir has been consistently delivering solid financial numbers, with growth accelerating with each quarter. This acceleration is driven by surging demand for its Artificial Intelligence Platform (AIP).

The trend is hard to ignore. Revenue growth accelerated from 39% in the first quarter of 2025 to 48% in the second quarter, 63% in the third quarter, and 70% in the fourth quarter. Rather than slowing after an exceptional 2025, Palantir entered 2026 with even stronger momentum.

In the first quarter of 2026, Palantir generated revenue of $1.63 billion, representing 85% year-over-year (YOY) increase and a 16% sequential growth. While Q1 was the company’s fastest revenue growth quarter, solid demand and an expanding customer base indicate that its top-line growth rate will accelerate further in the quarters ahead.

The U.S. remains Palantir's biggest growth market. Its U.S. revenue jumped 104% YOY and 19% sequentially in Q1 as businesses and government agencies accelerated AI adoption.

Customer growth has been equally impressive. Palantir ended the quarter with 1,007 customers, up 31% from a year earlier, while its U.S. commercial customer count climbed 42% to 615.

Revenue from Palantir's top 20 customers increased 55% YOY, with each generating an average of $108 million over the past 12 months. This shows the company is not only attracting new customers but also deepening relationships with existing ones.

Commercial demand has become a major growth engine alongside the company's traditional government business. U.S. commercial revenue surged 133% to $595 million, reflecting strong enterprise demand for AI solutions that improve productivity and decision-making.

Meanwhile, the government segment remains exceptionally strong. U.S. government revenue rose 84% to $687 million, supported by contract renewals, larger deployments, and new program wins.

With both commercial and government businesses growing rapidly, customer base increasing rapidly, and existing customers increasing their spending, Palantir’s growth rate is likely to accelerate in the quarters ahead.

Palantir's Core Growth Metrics Continue to Strengthen

The headline revenue growth wasn't the only encouraging takeaway from Palantir's latest results. Several underlying operating metrics suggest the company's momentum could extend well into the coming quarters.

Most notably, Palantir's net dollar retention rate climbed to 150%, indicating that existing customers are significantly increasing their spending. Further, its total contract value (TCV) bookings surged 135% YOY. Since bookings represent future contracted revenue, this sharp increase provides investors with greater visibility into future sales and indicates that Palantir's revenue pipeline continues to expand rapidly.

Management's Guidance Strengthens Investment Case

Palantir now expects approximately $7.66 billion in revenue for 2026, up from its previous forecast of $7.19 billion. At the midpoint, the new outlook implies annual revenue growth of roughly 71%, indicating that the demand remains exceptionally strong.

Also, the company raised its outlook for its U.S. commercial business, which is now expected to generate more than $3.22 billion in revenue this year, implying at least 120% YOY growth. With enterprise AI adoption still in its early innings, this segment could become Palantir's largest long-term growth driver.

Profitability is improving alongside revenue growth. Palantir now expects adjusted operating income of $4.44 billion to $4.45 billion, while adjusted free cash flow is projected to reach $4.2 billion to $4.4 billion. The combination of accelerating revenue, expanding margins, and a rapidly growing backlog suggests the company's outlook remains solid.

The Bottom Line

The recent correction in Palantir stock has reduced some valuation risk, while the company's fundamentals have strengthened. Its accelerating revenue growth, rising customer spending, expanding backlog, and improving profitability justify its current valuation, making it a compelling investment option.

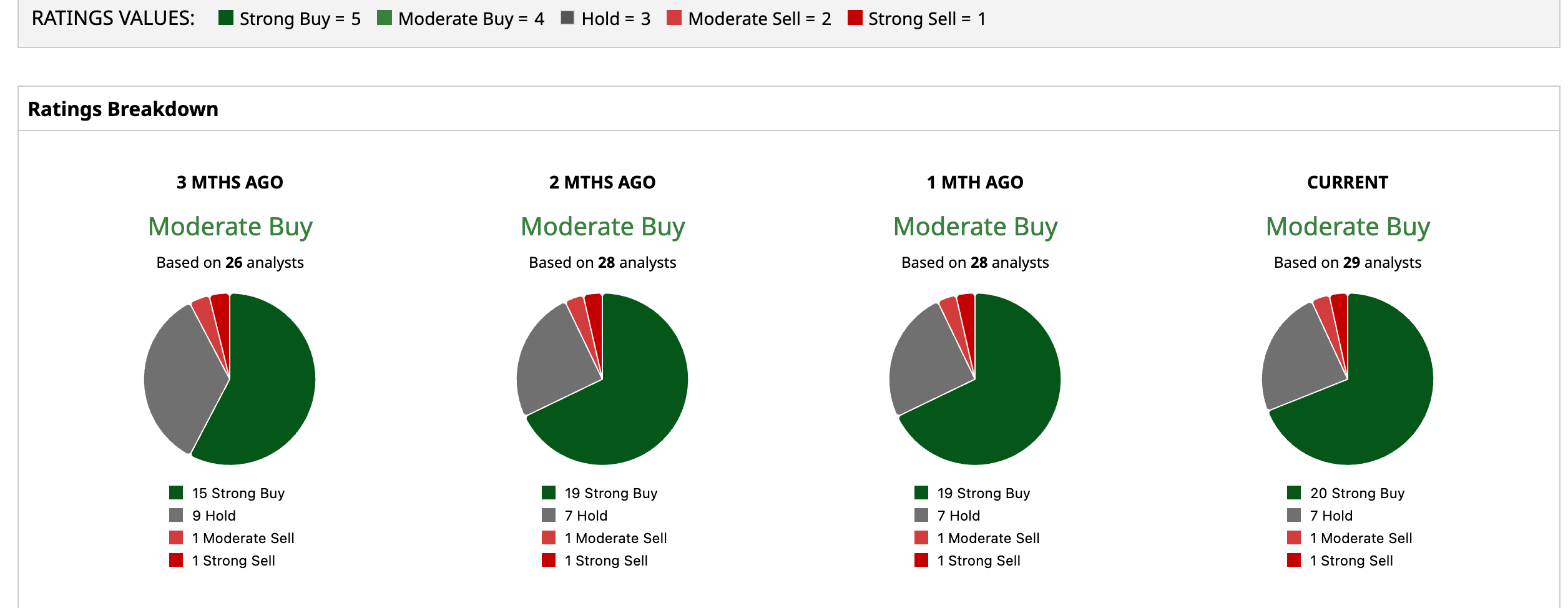

Analysts have a “Moderate Buy” consensus rating for Palantir stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)