/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

China’s artificial intelligence (AI) race is no longer just about building bigger data centers. It is increasingly about deciding who gets to fill them. As Beijing doubles down on technological self-reliance, Chinese enterprises are shifting more of their AI infrastructure spending toward homegrown chipmakers, reshaping one of the world’s largest semiconductor markets in the process. For companies that once viewed China as a major growth opportunity, the changing landscape is becoming far more challenging.

Fresh data from a Bloomberg survey underscores just how quickly that transition is unfolding. Among 60 executives across China’s software, finance, manufacturing, and retail sectors, respondents said they expect domestic AI chips to account for 46% of their AI hardware budgets over the next 12 months, up sharply from roughly 30% today. Meanwhile, nearly 80% reported that AI infrastructure projects are already running over budget, prompting companies to prioritize readily available local alternatives over imported hardware.

The biggest beneficiaries of that shift are domestic chipmakers such as Huawei, Hygon, and Cambricon, while tech giants including Tencent Holdings (TCEHY), Alibaba (BABA), China Telecom, and China Mobile continue pouring billions into expanding AI data centers across the country. In fact, AI startup Z.ai, formerly known as Zhipu, is reportedly exploring the development of its own custom AI chips as demand for its general language models accelerates.

That trend presents an increasingly difficult backdrop for Santa Clara-based Advanced Micro Devices (AMD). Although Chinese customers continue deploying AMD’s MI308 AI accelerators, Bloomberg’s survey suggests their share could steadily decline as government policies encourage domestic sourcing and legacy AMD chips become harder to obtain. With Chinese companies expected to invest roughly $294 billion in domestic data center projects over the next five years, AMD risks watching a significant slice of that opportunity shift to local competitors.

To that end, here’s what investors should know before making their next move on AMD stock amid these growing headwinds.

About Advanced Micro Devices Stock

Advanced Micro Devices is one of the world’s leading semiconductor companies, designing the chips that power AI data centers, cloud computing, personal computers, gaming consoles, and enterprise applications. The company has a market capitalization of $841.6 billion.

AMD has strengthened its position in recent years through its EPYC server processors and Instinct AI accelerators, which are seeing growing adoption among cloud providers and enterprise customers. With a broad portfolio spanning CPUs, GPUs, networking, and software, AMD is well positioned to benefit from the rising demand for AI infrastructure and high-performance computing.

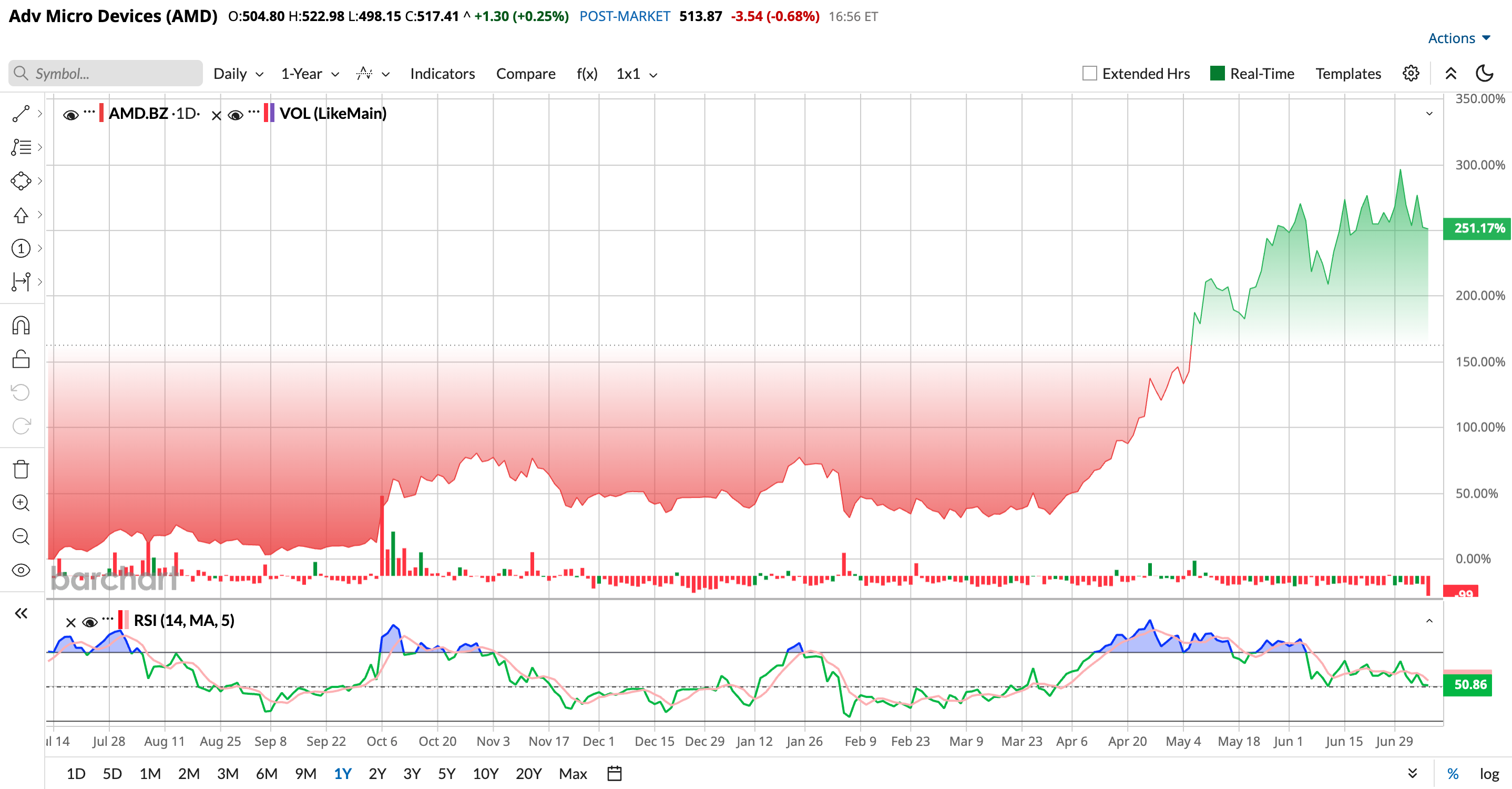

AMD stock has been on a remarkable run over the past year, reflecting Wall Street’s growing belief that the chipmaker will remain one of the biggest beneficiaries of the AI revolution. As demand for AI infrastructure, high-performance computing, and data center chips continues to surge, investors have steadily piled into the stock, sending AMD’s shares up an impressive 275.4% over the past 52 weeks and comfortably ahead of the broader market.

Wall Street also became increasingly optimistic. Toward the end of June, analysts raised their price targets, with Wells Fargo lifting its target to $615 on expectations of strong server CPU demand, while Cantor Fitzgerald boosted its target to $700, describing the current AI semiconductor cycle as a “generational” opportunity. That optimism helped AMD shares climb to a record high of $584.73 on June 30.

The celebration was short-lived, though. In the very next trading session, the stock dropped nearly 7% after reports suggested that Meta Platforms (META) could begin reselling excess AI computing capacity, raising fresh competitive concerns. Even so, the pullback barely dented the broader rally. AMD stock remains up 141.6% in 2026 alone and has soared 123.2% over the past three months.

The momentum received another boost on July 6, when Japanese self-driving startup Turing announced it had begun using AMD’s AI GPUs for roughly 10% of its AI training workloads and had also secured an investment from AMD's venture capital arm. The announcement marked another notable AI customer win, helping the stock jump 6.6% as the broader chip sector regained its footing.

Technically, the chart looks steady. AMD's 14-day RSI, which had entered overbought territory in June, has eased to 51.38, suggesting the stock has taken a healthy breather after its massive rally rather than losing momentum. At the same time, rising green trading volumes indicate that buyers continue to step in, signaling that bullish sentiment remains intact.

AMD’s massive rally has also pushed its valuation to premium levels. The stock currently trades at 69.82 times forward adjusted earnings and 17.01 times sales, well above many semiconductor peers and its historical averages. Even so, investors appear willing to pay that premium, betting AMD's expanding role in AI infrastructure and data centers will justify its rich valuation over time.

A Snapshot of AMD’s Q1 Report

AMD delivered an impressive first-quarter report for fiscal 2026 on May 5. Revenue rose 37.8% year-over-year (YOY) to $10.25 billion, beating Wall Street’s expectations, while non-GAAP EPS increased 42.7% annually to $1.37. Once again, the company’s Data Center segment was the biggest growth driver, reflecting continued investment by cloud providers and enterprises in AI infrastructure.

Data Center revenue climbed 57.2% YOY to a record $5.8 billion, fueled by strong demand for AMD’s EPYC server processors and Instinct AI GPUs. Management noted that AI demand is evolving beyond simply adding more GPUs to data centers. As AI models become more sophisticated, businesses also need high-performance CPUs to manage and coordinate those workloads. AMD believes this trend will create another major growth opportunity for its EPYC processors, particularly as agentic AI and real-world AI inference workloads become more widespread.

Meanwhile, client and gaming segment revenue increased 22.6% annually to $3.6 billion, while Embedded revenue rose 6.1% to $873 million as demand improved across multiple end markets.

AMD ended the quarter with a solid balance sheet, holding $12.35 billion in cash, cash equivalents, and short-term investments against total debt of $3.2 billion. Operating cash flow reached $2.96 billion, while free cash flow improved to $2.57 billion from $2.08 billion in the previous quarter. The company also returned $1.1 billion to shareholders through share repurchases during the quarter.

Looking ahead, AMD expects the momentum to continue into the second quarter. Management guided for revenue of about $11.2 billion, plus or minus $300 million. At the midpoint, that represents roughly 46% annual growth. The company expects the Data Center business to remain the primary growth engine, while continued strength in the Client and Gaming segment and double-digit growth in Embedded are also expected to support another solid quarter.

Meanwhile, analysts tracking AMD expect Q2 EPS to be $1.35, up 400% YOY. Looking further ahead, profit is anticipated to jump nearly 88.1% to $6.15 per share in fiscal 2026 and surge another 76.1% in fiscal 2027 to $10.83 per share.

What Do Analysts Expect for AMD Stock?

Wall Street has become increasingly optimistic about AMD’s prospects, with several analysts raising their price targets in recent weeks. For instance, on June 29, C. J. Muse of Cantor Fitzgerald lifted his target price from $500 to a Street-high $700 while reiterating an “Overweight” rating. Muse also named AMD his top computing-sector pick, placing it ahead of Nvidia Corporation (NVDA) and Broadcom (AVGO). He believes the chipmaker is currently showing the strongest momentum among semiconductor companies, supported by its expanding AI opportunity.

The bullish sentiment extends well beyond Cantor Fitzgerald. Timothy Arcuri of UBS recently set a $670 price target, while Aaron Rakers of Wells Fargo raised his target to $615. Interestingly, Wells Fargo’s optimism stems largely from AMD’s fast-growing server CPU business, suggesting that demand for both AI accelerators and server processors is powering the company’s next phase of growth.

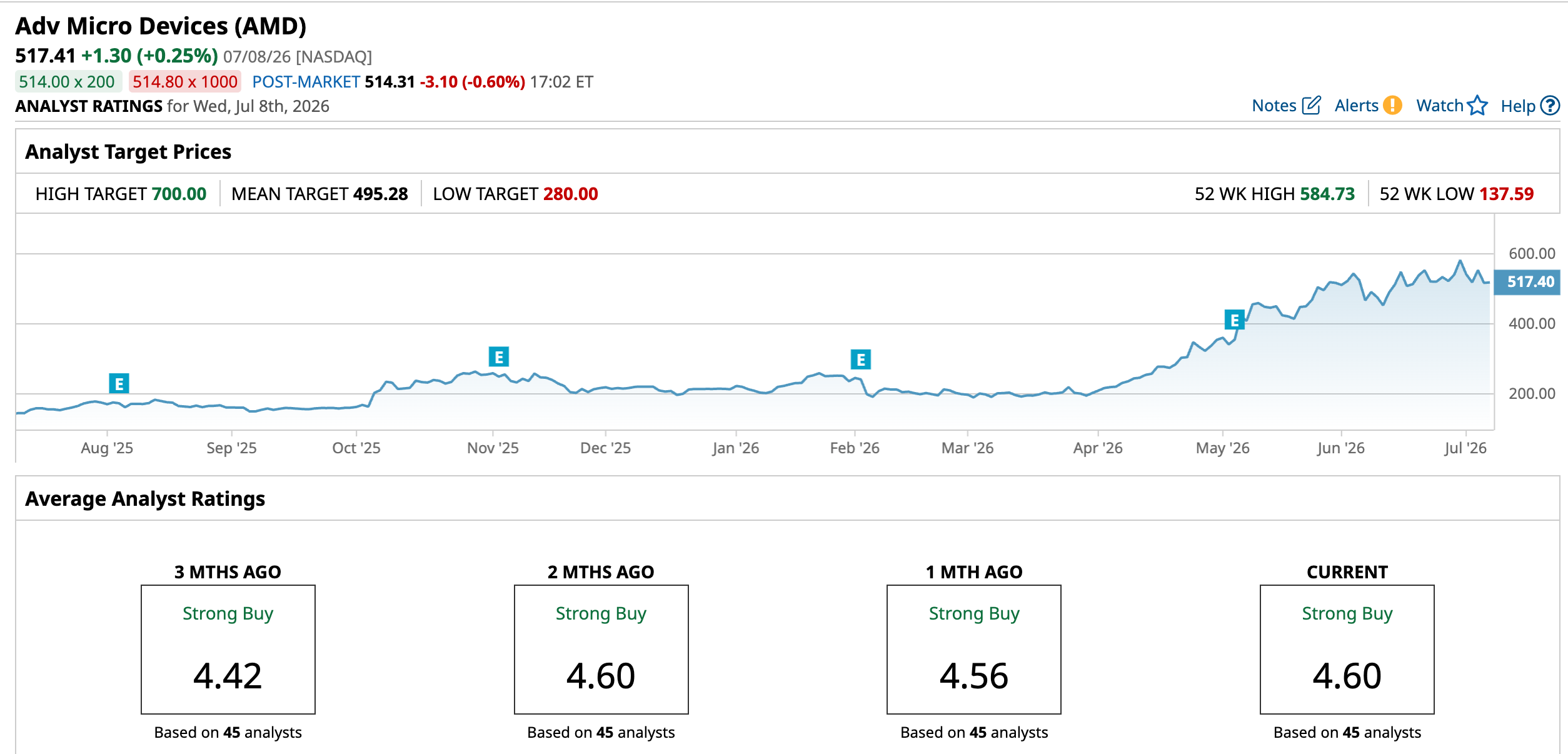

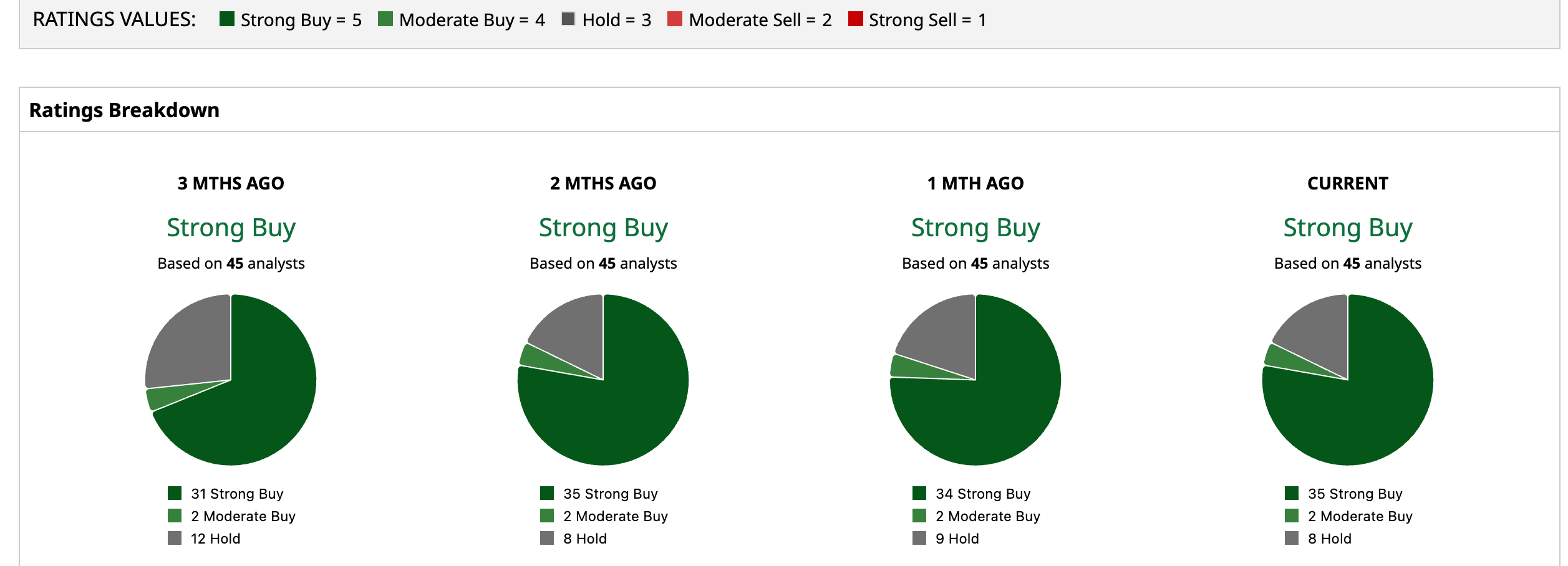

The stock carries a “Strong Buy” consensus overall. Among the 45 analysts tracking the stock, 35 issue a “Strong Buy,” two give a “Moderate Buy,” and eight advise a “Hold.”

AMD’s remarkable rally has already carried the stock above Wall Street’s average price target of $495.28. However, the Street-high target of $700 suggests the shares could still climb another 35.3% from current levels.

Final Thoughts on AMD Stock

China’s pivot toward homegrown AI chips is worth watching, but it’s probably not a reason to lose sleep over AMD stock just yet. For starters, Chinese companies are expected to invest about $294 billion in domestic data centers over the next five years. That’s a big number, until we compare it with the more than $700 billion U.S. hyperscalers are expected to spend in 2026 alone.

AMD also commands only about 4% of China’s AI accelerator market, meaning its exposure is relatively limited. While losing share in China is not ideal, AMD’s long-term growth story remains very much intact as AI infrastructure spending continues to boom across the rest of the world.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)