/AI%20(artificial%20intelligence)/3D%20Graphics%20Concept%20Big%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Sunrun (RUN) remained in focus on July 8 as the company officially entered the edge computing space with a distributed artificial intelligence (AI) data center pilot program.

The initiative places compute nodes directly into customer homes equipped with Sunrun solar and battery networks to handle AI inference workloads.

The announcement arrives at a time when investors desperately need a reason to stick with RUN stock, which is down about 36% year-to-date as of writing.

What the Pilot Program Means for Sunrun Stock

The new pilot program shifts AI workloads from massive data centers into residential properties, utilizing Sunrun’s expansive infrastructure of more than 1.1 million solar and battery storage systems.

By installing localized compute nodes inside customer homes, the clean energy company will sell modular artificial intelligence inference capacity directly to enterprise buyers.

This unique decentralized layout leverages existing home batteries for backup power, enabling data processing to continuously run through local blackouts.

For homeowners, the initiative acts as an economic incentive, offering financial compensation for hosting the nodes.

Meanwhile, Sunrun shares will benefit from a new high-margin revenue stream, given McKinsey estimates AI inference demand to grow at a compound annualized rate of a whopping 35%.

Is It Worth Buying RUN Shares Today?

RUN’s initiative effectively bypasses the lengthy grid interconnection queues and land acquisition bottlenecks that plague traditional data center buildouts.

Plus, it complements the company’s recent 16-gigawatt clean energy partnership with Tesla (TSLA) and Renew Home as well.

If this multi-month pilot hits its milestones, it could transform Sunrun stock from a pure-play solar utility into a notable picks-and-shovels AI infrastructure name.

Investors should also note that RUN is currently trading at a forward price-to-earnings (P/E) ratio of nearly 12x, which represents a meaningful discount not just to its historical multiple, but to its rivals like Enphase Energy (ENPH) as well.

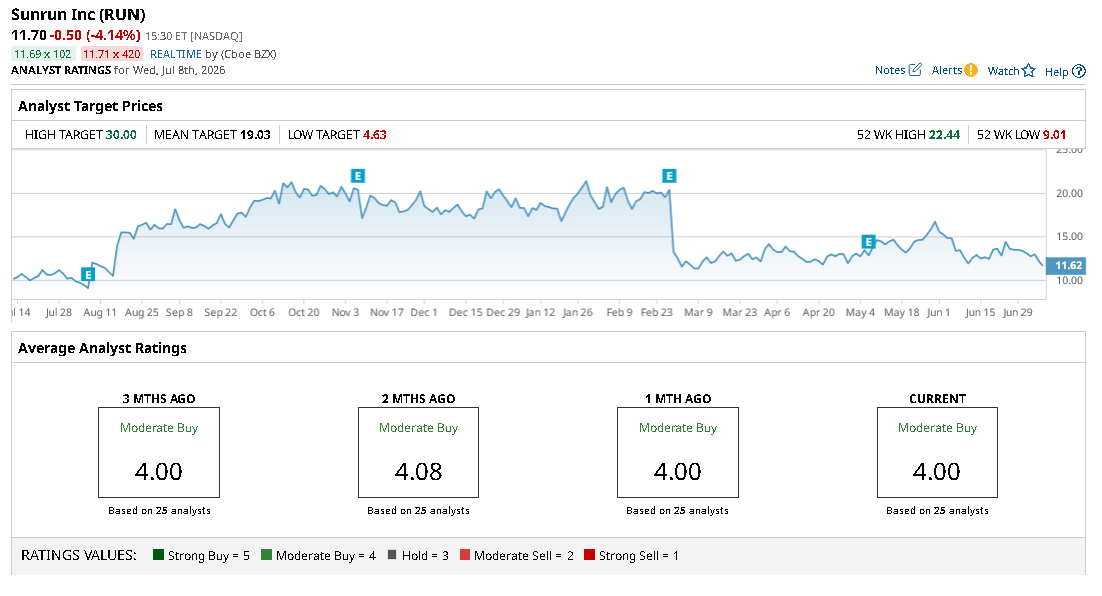

What’s the Consensus Rating on Sunrun?

Crucially, Wall Street analysts remain convinced that RUN shares’ year-to-date decline has gone a bit too far.

According to Barchart, the consensus rating on Sunrun sits at “Moderate Buy” currently, with the mean price target of about $19 indicating nearly 60% upside from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)