Wall Street has a habit of jumping to conclusions, especially when a new headline threatens to reshape a fast-growing industry. That was exactly what happened when reports suggested Meta Platforms (META) might rapidly expand its AI data center footprint and its plans to potentially monetize excess computing capacity through a cloud business.

Investors wasted little time selling shares of AI infrastructure providers like Nebius Group N.V. (NBIS), which slipped 17% on July 1 and is still falling, fearing the social media giant could become a formidable competitor rather than a customer. The assumption seemed straightforward. If Meta becomes a cloud provider itself, companies like Nebius could lose out.

However, not everyone is convinced the market got the story right.

A fresh analysis from SemiAnalysis argues that the market may have been too quick to draw conclusions. Instead of replacing AI infrastructure providers, Meta’s relentless appetite for computing power could create even bigger opportunities for them. The research firm believes Meta’s AI ambitions are still expanding rapidly, with data center investments expected to accelerate over the next few years, making partners like Nebius important beneficiaries rather than casualties.

If that view proves correct, the recent decline in Nebius stock may have less to do with weakening fundamentals and more with misplaced investor fears – making the latest pullback one worth a closer look.

About Nebius Stock

Nebius Group is an AI infrastructure company headquartered in Schiphol, the Netherlands, focused on building a full-stack cloud platform for AI applications. The company provides large-scale GPU clusters, AI cloud services, and developer tools that help enterprises train and deploy AI models.

Beyond its core business, Nebius also owns TripleTen, a technology-focused reskilling platform, and Avride, which develops autonomous driving and delivery robotics technologies. Backed by a strategic partnership with Nvidia Corporation (NVDA), Nebius is rapidly expanding its AI cloud infrastructure to serve customers across industries, including healthcare, finance, robotics, and government. Led by founder and CEO Arkady Volozh, the company has also expanded into AI supercomputing and today commands a market capitalization of $49.4 billion.

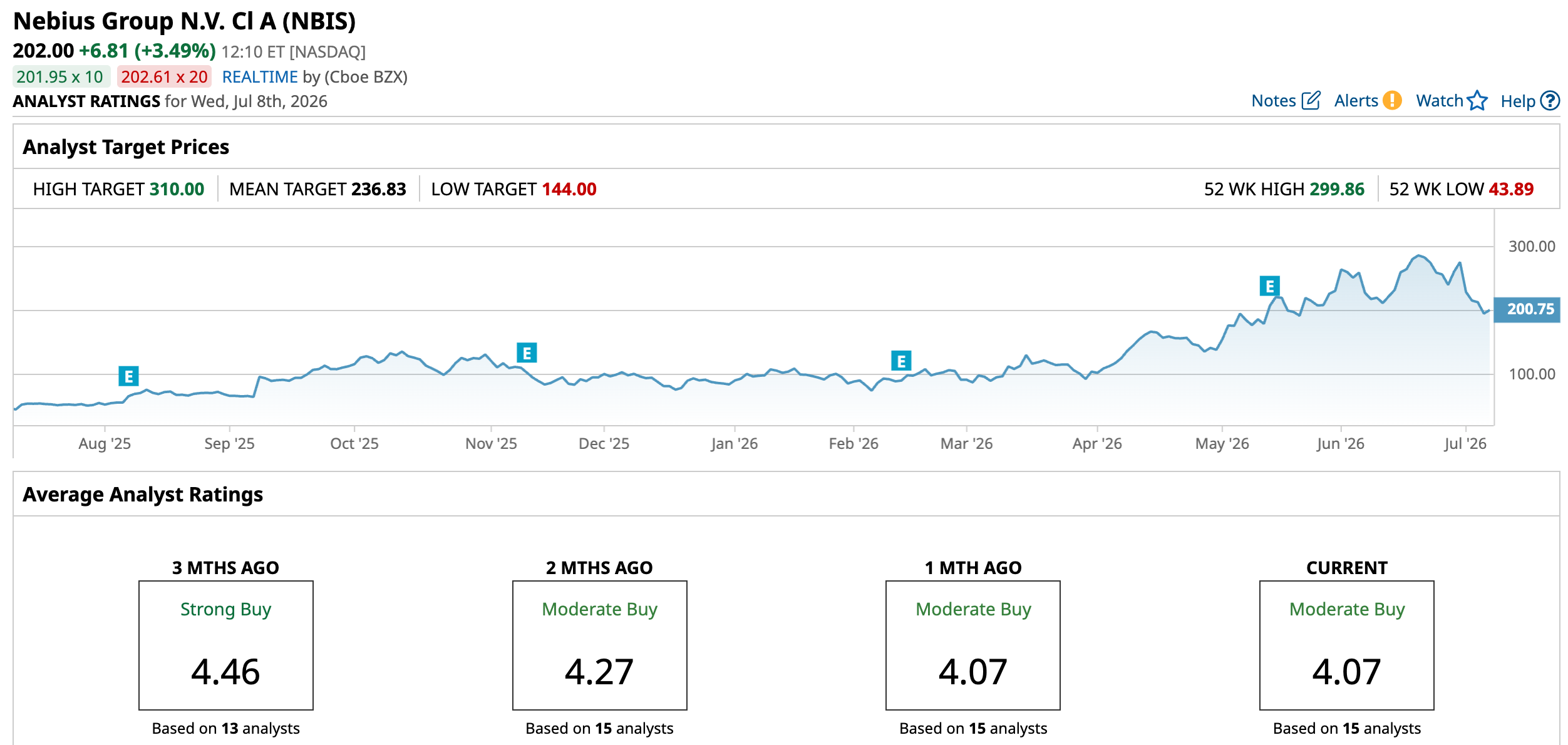

Nebius has rewarded patient investors over the past year, with the stock proving that fortune often favors the bold. Over the past 52 weeks, NBIS shares have soared 346%, driven by relentless demand for AI infrastructure. The momentum carried into 2026, with the stock climbing 151% year-to-date (YTD), while gaining 68% in just over the past three months. Much of that optimism was fueled by the company’s blockbuster first-quarter results in May and its inclusion in the Nasdaq-100 Index on June 22, a milestone that further boosted investor interest.

However, no rally moves in a straight line. After touching an all-time high of $299.86 on June 22, the stock ran into a wall as broader concerns over artificial intelligence (AI) valuations and the sustainability of the sector sparked a wave of profit-taking. Plus, Meta's recent cloud business news added fuel to the fire. Since that peak, NBIS has retreated 30.5%, reminding investors that even the strongest momentum stocks occasionally take a breather.

Technically, the chart suggests caution in the near term. Recent trading sessions have been accompanied by red volume bars, indicating selling pressure. The 14-day Relative Strength Index (RSI) has eased to 43.51, reflecting weakening momentum without yet entering oversold territory.

Meanwhile, the MACD oscillator has turned mildly bearish, with the MACD line slipping below the signal line and the histogram printing red bars. While the long-term uptrend remains intact, the stock may need time to catch its breath before attempting its next move.

Valuation-wise, NBIS stock is priced at 14.72 times forward sales, representing a premium to the sector average of 3.34 times.

A Snapshot of Nebius’ Q1 Earnings Report

Nebius impressed investors with its first-quarter 2026 results, sending the stock up 22.4% over the two trading sessions following earnings. Revenue surged 684% year-over-year (YOY) to $399 million, while its core AI business – excluding Avride and TripleTen – grew 841% to $390 million, driven by rapid capacity expansion, high infrastructure utilization, and strong pricing across its AI cloud platform.

The company continued to invest aggressively for future growth, and that came at a cost. Adjusted net loss widened 20% YOY to $100.3 million, reflecting higher spending on data center expansion, AI platform development, strategic acquisitions, and engineering talent. Even so, adjusted EBITDA swung to a $129.5 million profit, with margin expanding to 32%. Within the Nebius AI business, adjusted EBITDA margin improved sharply to 45%, up from 24% in the fourth quarter of 2025, pointing to improving operating leverage as the business scales.

Additionally, Nebius ended the quarter with a much stronger financial position. It raised approximately $4.3 billion through convertible senior notes, secured a $2 billion equity investment from Nvidia, and finished the quarter with $9.3 billion in cash and cash equivalents. Operating cash flow surged to $2.26 billion, largely driven by upfront customer payments, giving the company ample resources to continue expanding its AI infrastructure.

Nebius further strengthened its growth outlook by announcing a five-year, $27 billion agreement with Meta, including a $12 billion dedicated compute commitment and $15 billion in optional capacity. Management said the deal provides financing flexibility while allowing capacity to be allocated between Meta and higher-margin AI cloud customers.

And, the company expanded its partnership with Nvidia, earning Nvidia Exemplar Cloud status for GB300 training workloads and improving access to future GPU platforms, including Vera Rubin. Meanwhile, AI demand remains robust, with pipeline generation rising 3.5x sequentially, while multiple customers continue competing for every GPU deployed.

Nebius’ momentum extends well beyond adding more computing capacity. The company is seeing growing adoption across industries, with customers in fintech, healthcare, robotics, manufacturing, pharmaceuticals, and life sciences using its AI cloud and inference platforms to power large-scale AI applications. Management highlighted strong demand for inference workloads, which it believes will be one of the fastest-growing segments of the AI cloud market.

To keep pace with demand, Nebius continues to expand its infrastructure aggressively. During Q1, it increased contracted power capacity to more than 3.5 gigawatts (GW) and raised its 2026 target to at least 4 GW. It also unveiled a new Pennsylvania AI factory capable of supporting up to 1.2 GW of power capacity.

Meanwhile, Nebius is evolving into a full-stack AI platform. Its Token Factory inference platform is gaining enterprise traction, while acquisitions of Eigen AI, Clarifai, and Tavily have strengthened its inference, agentic AI, and software orchestration capabilities.

Looking ahead, Nebius expects 2026 annualized run rate revenue of $7 billion to $9 billion, group revenue of $3 billion to $3.4 billion, and an adjusted EBITDA margin of around 40%, although margins could fluctuate as new capacity comes online. The company also raised its 2026 capex guidance to $20 billion to $25 billion from $16 billion to $20 billion to support anticipated 2027 demand, citing strong customer commitments rather than cost inflation.

However, the aggressive expansion carries execution risks. Nebius must secure GPU supply, complete data center projects on schedule, and navigate intense competition. Any slowdown in AI spending, deployment delays, or pricing pressure could weigh on utilization, cash flows, and profitability.

Analysts monitoring the company anticipate fiscal 2026 loss per share to widen by 7.9% YOY to -$1.91, before narrowing down by 83.3% annually to -$0.32 in fiscal 2027.

Why SemiAnalysis Remains Bullish on Nebius

SemiAnalysis believes the market has misread Meta’s latest AI infrastructure strategy, arguing that the company’s expanding compute needs are likely to create more opportunities for AI cloud providers like Nebius rather than diminish them.

The research firm notes that Meta has already contracted more than 5 GW of data center capacity across cloud and colocation providers in just the first half of 2026 alone. Even more importantly, it argues that this buildout is far from complete, projecting that Meta’s 2027 capex will be “shockingly high” as the company continues to scale its AI ambitions.

That outlook directly challenges the recent selloff in Nebius’ shares, which was triggered by fears that Meta’s plans to monetize excess AI compute through a cloud business would cannibalize neocloud providers. SemiAnalysis dismisses that concern, arguing Meta’s external compute procurement will continue to accelerate. Since early 2024, Meta has signed nearly 10 GW of datacenter deals, with the bulk of new capacity sourced from third-party providers rather than self-built infrastructure.

The brokerage firm expects that trend to continue as Meta invests in initiatives such as Meta Superintelligence Labs, a planned 10x expansion of its AI-powered advertising recommendation systems, and potentially a roughly $10 billion compute partnership with Anthropic, if ongoing discussions materialize.

Consequently, SemiAnalysis believes companies like Nebius could remain key beneficiaries of Meta’s growing AI infrastructure spending and see meaningful growth in their remaining performance obligations (RPO) over time. The recent sell-off in Nebius’ shares reflects short-term fears rather than a deterioration in the company’s long-term growth outlook.

What Do Analysts Expect for Nebius Stock?

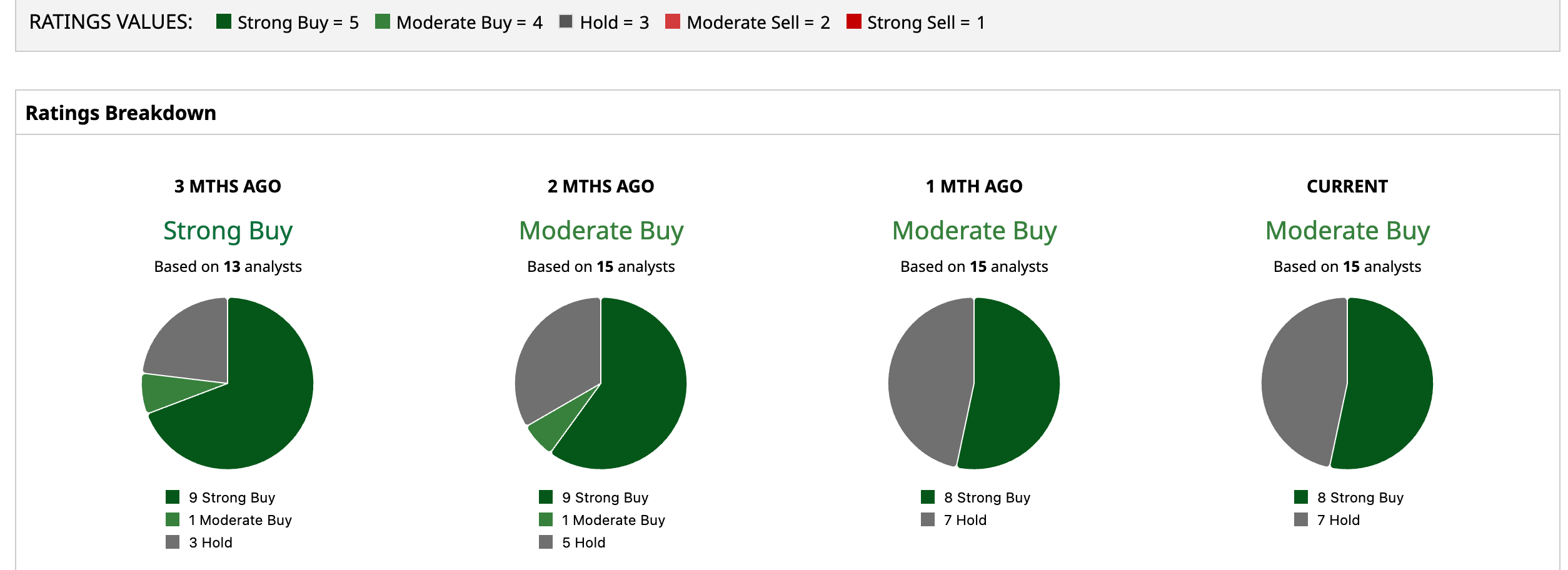

Wall Street’s stance on Nebius has become more measured. While the stock still carries a consensus “Moderate Buy” rating, that’s a step down from the “Strong Buy” consensus it enjoyed three months ago. Among the 15 analysts in coverage, eight suggest a “Strong Buy,” and seven analysts recommend a “Hold.”

NBIS has a mean price target of $236.83, which implies that the stock has an upside potential of 17.2% from the current price levels. The Street-high target of $310 suggests that NBIS could rise as much as 53.5%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)