/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

Micron Technology (MU) has been one of the market's biggest winners over the past year, and the chipmaker just added another catalyst. The company unveiled a new long-term memory supply agreement with Ford Motor (F), extending its push into the fast-growing automotive market.

The announcement comes shortly after Micron delivered another blockbuster quarterly report, beating Wall Street's expectations on both revenue and earnings. Those results only tell one thing: that AI-driven demand and higher memory prices continue to fuel record profitability.

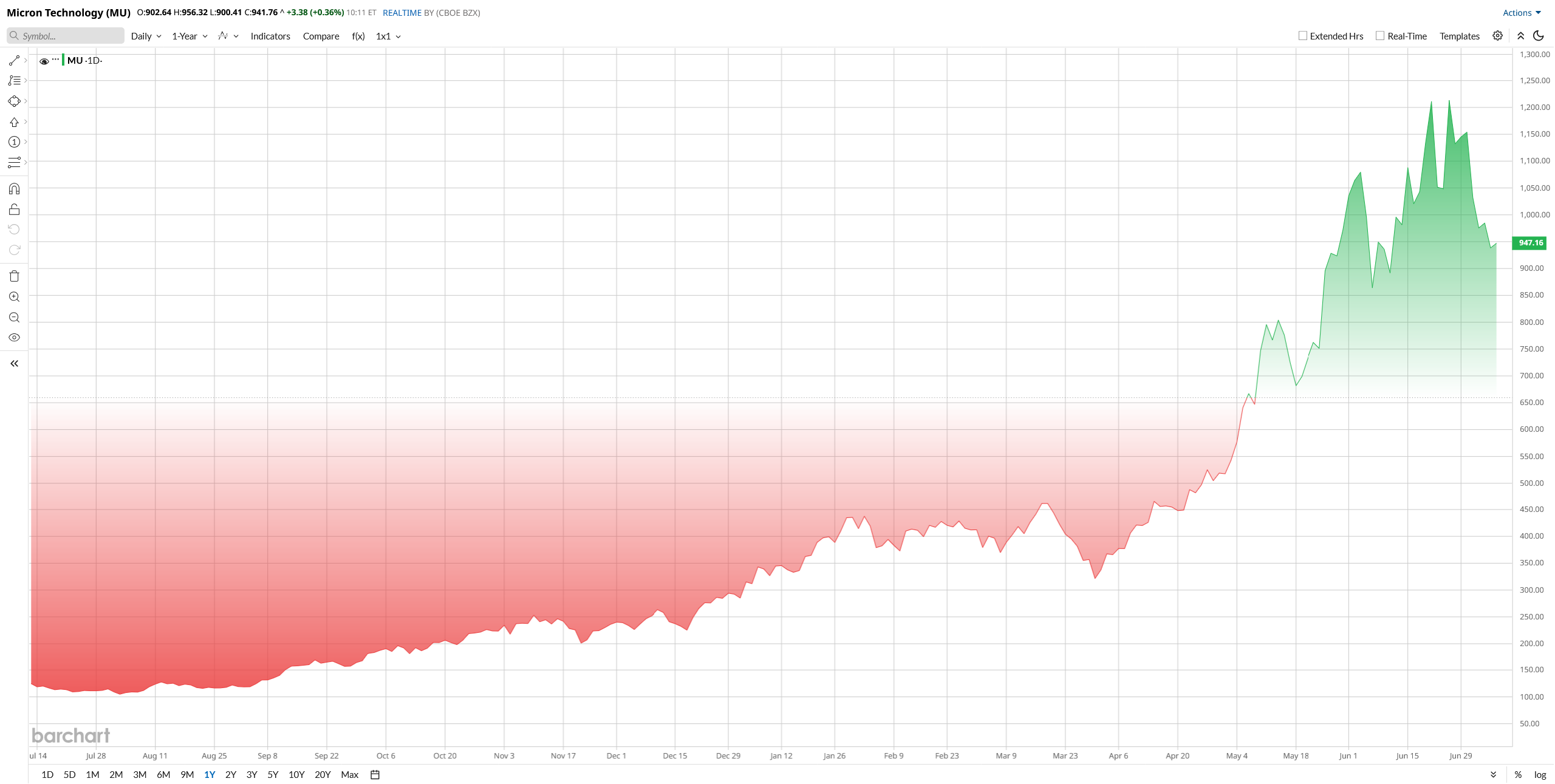

The combination of another strategic customer agreement, booming financial results, and strong AI demand helped support investor sentiment. That's the reason MU stock is soaring and has climbed roughly 660% over the past year, although the stock already trades at a premium valuation that leaves little room for disappointment.

Ford Expands Micron’s Automotive Opportunity

The new agreement makes Ford the latest automaker to secure long-term memory supply from Micron. Under the deal, the company will provide automotive-grade DRAM and NAND memory products designed for Ford's next-generation electric and intelligent vehicles.

The agreement is significant because automotive memory demand continues to grow as vehicles become more software-defined and AI-enabled. Long-term contracts also give Micron better visibility into future demand while reducing its exposure to the industry's traditionally volatile spot pricing.

Ford joins a growing list of strategic customers. Micron has now signed 16 Strategic Customer Agreements this year, highlighting management's effort to lock in demand across automotive, cloud computing, and AI markets.

Micron Crushes Q3 Earnings Estimate

The Ford announcement follows one of the strongest quarters in Micron's history. During fiscal third-quarter 2026, the company generated $41.46 billion in revenue, easily topping analyst estimates and surging from $9.3 billion a year earlier. Adjusted earnings reached $25.11 per share, also ahead of Wall Street expectations, while gross margins expanded sharply as pricing remained favorable across both DRAM and NAND products.

Management expects the momentum to continue. Micron forecast approximately $50 billion in fourth-quarter revenue along with another quarter of record earnings, suggesting that AI infrastructure spending and constrained memory supply remain powerful growth drivers heading into early 2027.

The Company Isn’t Relying Only on AI Servers

AI data centers are still the largest growth engine in Micron; management is growing in multiple end markets.

The company also recently inked another long-term automotive memory deal with General Motors (GM), and previously, the company announced a joint venture with AI startup Anthropic that aims to reach first-to-market with memory technology designed specifically for AI memory workloads training and inference.

The investment in manufacturing capacity is also high at Micron. The firm recently spent approximately $2 billion to rehabilitate its Manassas, Virginia, plant, which boosted local DRAM manufacturing and its U.S. manufacturing presence.

These investments aim to ensure provision for future demand and to ensure revenue stability by contracting with customers for longer periods than with the memory business model.

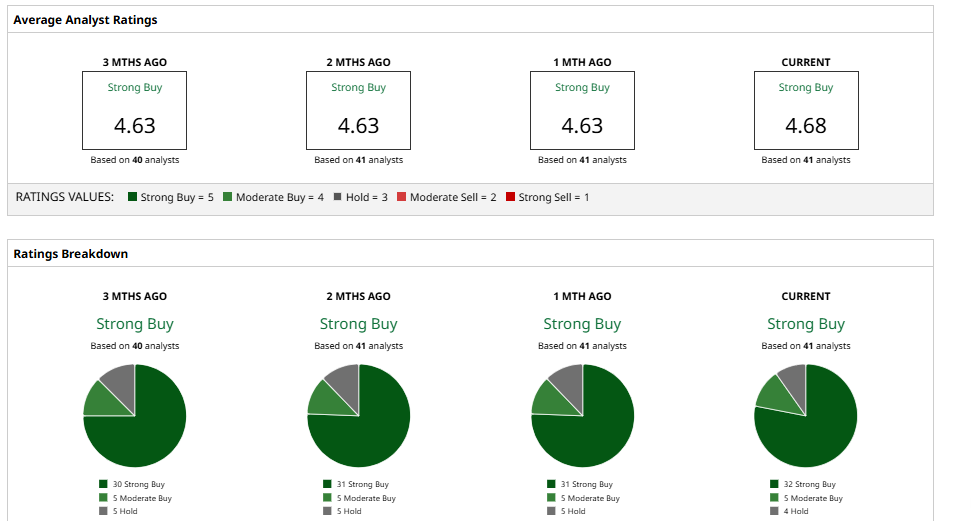

What Analysts Think About MU Stock

Wall Street is definitely upbeat about MU stock despite the abnormally high valuation.

Several banks have initiated their uptick in price targets since Micron's last earnings call and growing customer selection of strategic agreements. Leading analysts at Bank of America, UBS, and J.P. Morgan feel the announced energy contracts are reducing the business's cyclicality from previous memory energy cycles, whereas ongoing investment in AI will have a positive impact on its earnings.

The wider analyst consensus is “Strong Buy,” and the average price target sits at $1,421.94, suggesting an appetizing 50% upside premium from where it stands currently.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)