/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Memory chips have become costly, owing to the high demand and limited supply of high-bandwidth memory (HBM). As a result, AI infrastructure deployments have also become more costly — that is if companies can get their hands on memory in the first place. Back in October 2025, Nvidia (NVDA) CEO Jensen Huang traveled to South Korea to meet with executives and secure memory supply. When the world first woke up to memory as a bottleneck, Nvidia already had a head start.

Still, while Huang did something similar in June of this year, he hasn’t been able to make the company immune to the memory supply shock. AI server racks are becoming hard to build with limited memory, and the problem is now finally knocking on Nvidia’s door.

GF Securities analyst Jeff Pu believes that the unprecedented memory price surge will impact Nvidia’s server rack deployment. Pu now expects the Vera CPU rack to change to 96GB per SOCAMM, resulting in a total of 768GB per CPU. Per the spec sheet, it is supposed to be twice this amount at 1.5TB, but clearly the bottleneck is so severe that even the godfather of AI isn’t immune. More importantly, the LPDDR5X capacity accounts for 61% of the Vera Rubin 200 rack memory and storage budget. The reduction in capacity therefore makes sense from a financial perspective as well. Going forward, Pu expects memory to account for 20% of the materials cost for AI racks in 2027.

About Nvidia Stock

Nvidia is a semiconductor company that designs graphics processing units (GPUs), AI chips, and networking solutions for data centers, automotive applications, professional visualization, and gaming. Founded in 1993, the company is headquartered in Santa Clara, California, and has a market capitalization of $4.7 trillion.

Over the last 12 months, NVDA stock has increased by 24%, marginally outperforming the S&P 500’s ($SPX) 20% gain during the same period. On its own, the growth seems respectable. Look at the growth of Nvidia’s peers, however, and the gain looks comparatively insignificant. Micron (MU) stock, for instance, has increased 682% in the past year. Meanwhile, NVDA stock has also come under pressure amid growing concerns about U.S. export restrictions on AI chips to China. In the past month, the stock has declined by 4%, which some analysts believe might make for an attractive entry point.

Nvidia’s valuation presents one of the most compelling cases in the current market. The company now trades at a significant discount compared to its historic norms, with the forward price-to-earnings (P/E) ratio of 22.4 times significantly cheaper than its five-year average. The EPS growth trajectory also makes NVDA stock appealing, with analysts expecting 90% growth in fiscal 2027 followed by 34% growth in fiscal 2028. Capital structure is exceptional as well, with Nvidia being net cash positive by more than $40 billion.

One primary concern for investors remains U.S. export restrictions on AI chips to China, which have reduced Nvidia’s total addressable market. However, most analysts believe the market to be undervaluing a company trading at a considerable discount while delivering record revenue performance.

Nvidia Reports Earnings

Nvidia reported first-quarter fiscal 2027 earnings on May 20. The firm achieved record results across every key metric. Revenue of $81.6 billion grew 85% year-over-year (YOY), beating the analyst consensus of $78 billion. Non-GAAP EPS of $1.87 represented even bigger growth of 140% YOY, comfortably beating the $1.77 consensus estimate. The key driver for Nvidia's record revenue was the data-center segment, which accounted for $75.2 billion in revenue, up 92% YOY. Additionally, the company raised its quarterly dividend from $0.01 to $0.25. CEO Jensen Huang credited agentic AI for the extraordinary quarter, stating that “demand has gone parabolic.”

For Q2, Nvidia guided revenue of approximately $91 billion. Gross margin is also expected to be a healthy 75%, signaling strong pricing power. CFO Colette Kress stated that OpEx growth is estimated to climb in the upper 40% range. Due to ongoing export restrictions, the company has not recognized any data-center revenue from China in Q2. Export restrictions have had a severe impact on investors' confidence in Nvidia, as NVDA stock fell following the earnings report despite the exceptional numbers.

What Are Analysts Saying About Nvidia Stock?

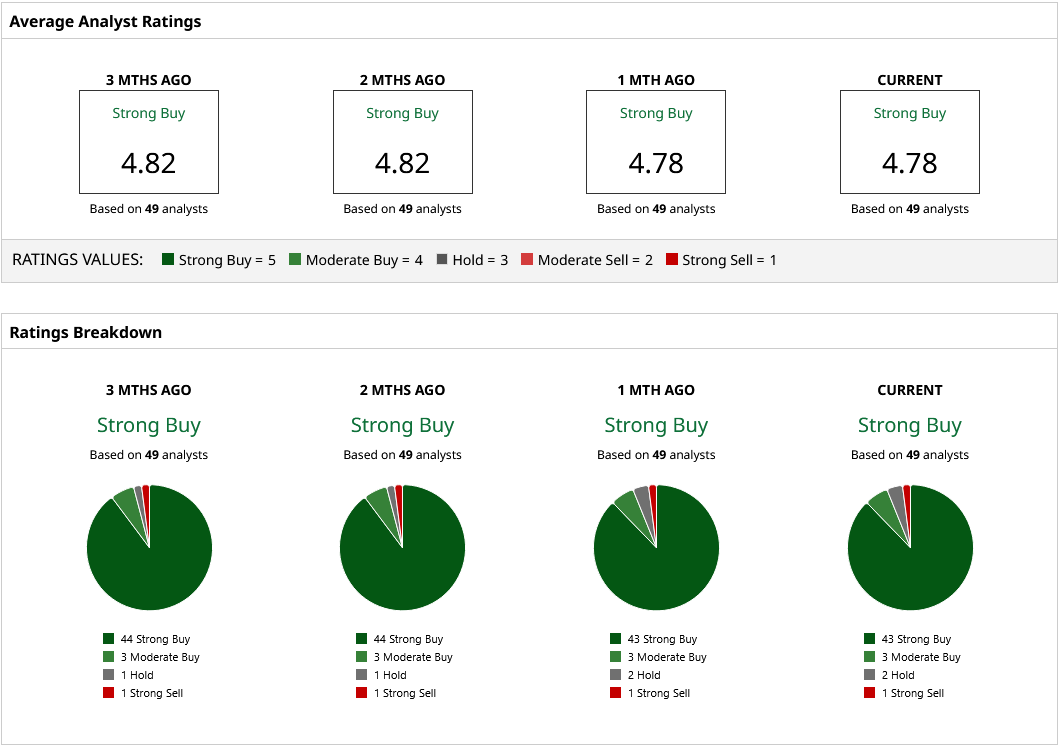

Bernstein analyst Stacy Rasgon has a “Buy” rating for Nvidia with a price target of $315. Continued growth in AI infrastructure demand has driven a bullish view amongst analysts. Bank of America Securities analyst Vivek Arya and Oppenheimer analyst Rick Schafer also have “Buy” ratings for NVDA stock.

Based on 49 Wall Street analysts with coverage, Nvidia stock holds a consensus “Strong Buy” rating. The mean price target of $301.92 indicates potential upside of 53% from current levels. The overall positive analyst outlook is understandable for a company that has recently lost stock value even after delivering record results.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)