/O'Reilly%20Automotive%2C%20Inc_%20location%20by-%20jetcityimage%20via%20iStock.jpg)

It was a good day in the markets on Monday, as all the major indexes were in positive territory: the S&P 500 was up 0.72%, the Dow Jones Industrial Average gained 0.29%, the NASDAQ Composite was up 1.12%, and the Russell 2000 gained 0.45% on the day.

On the pitch, the U.S. got thoroughly trounced by a better Belgium squad, 4-1. Their World Cup run was good, but their tournament has come to an end. Belgium moves on to the quarter-finals to face Spain on Friday in Los Angeles. The final two quarter-finalists will be determined today with games in Atlanta and Vancouver.

Yesterday’s bearish price surprises for stocks with high share volumes included automotive parts retailer O’Reilly Automotive (ORLY). Its share volume was 15.34 million, about 63% higher than its 30-day average. Its options volume was unusually high at 18,469, about 6.8 times the 30-day average.

Not sure what all the fuss was about. O’Reilly doesn’t report Q2 2026 earnings until July 29, and there was no new news about the Bloomberg report from last week that O'Reilly might bid $10 billion to buy Genuine Parts' (GPC) automotive business.

As a result of speculation, ORLY stock lost 6.66%, putting it on Barchart’s bearish price surprises list. Down nearly 10% over the past 12 months, its valuation looks to be more reasonable than it’s been in some time.

The question is whether it’s shed enough to entice buyers back into the fray. With that in mind, I consider the pros and cons of buying ORLY stock at $85 and change.

The Pros of Buying ORLY Stock Now

Before O’Reilly’s latest swoon, ORLY hadn’t traded around the $85 level since December 2024. Further, its share price is down 22% over the past nine months, since hitting an all-time high of $108.71 in September 2025.

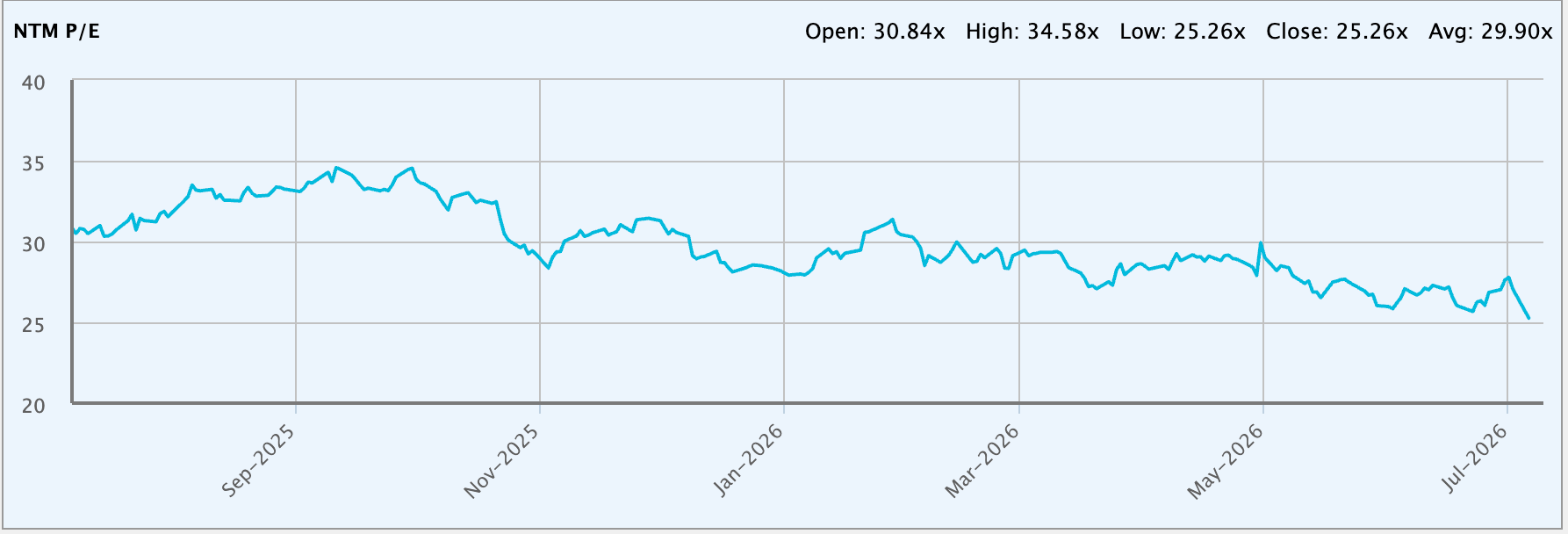

The one-year chart below shows that O’Reilly’s current forward P/E ratio is 25.26x, about 27% less than the September 2025 multiple of 34.58x at its all-time high.

Source: S&P Global Market Intelligence

The two-year chart shows that, except for July 2024, its current multiple remains reasonable relative to the high and low over the past 24 months.

Source: S&P Global Market Intelligence

One financial metric that I use to consider a stock’s valuation is the free cash flow (FCF) yield. In the 12 months ended March 31, O’Reilly’s FCF yield is 2.4% based on an enterprise value of $78.22 billion and $1.87 billion in FCF. As of Sept. 30, 2025, at the all-time high, ORLY had an enterprise value of $99.53 billion, FCF of $1.57 billion, and an FCF yield of 1.6%.

Normally, I’d toss a stock with a 2.4% yield aside -- I consider FCF yields between 4% and 8% to be fair value (you’re not overpaying), above 8% to be undervalued, and below 4% to be overvalued -- but it’s important to look at its FCF yield from a historical perspective before doing so.

O’Reilly generated $2.76 billion in free cash flow in 2021, the highest in its history. That’s a 20.7% margin. That’s double what it is today.

The big difference is the company’s capital expenditures, which have increased by 154% since 2021. There are several reasons for this.

First, it’s opening many new stores. In 2025, it opened 207 new stores across 37 states, Puerto Rico, and Mexico. In 2026, it expects to open 230 at the midpoint of its guidance. It finished Q1 2026 with 6,644 stores, including 6,495 in the U.S., 121 in Mexico, and 28 in Canada.

All of these new stores cost money to open. Since the end of 2021 (13 quarters), it has added 860 net new stores. That’s an average of 66 per quarter. The company typically spends around $3 million to open a new store built from the ground up. That’s about $200 million a quarter.

Secondly, it’s building out its distribution center network to keep the stores inventoried. The most recent to open was in December 2025 in Stafford County, Virginia. The 550,000-square-foot DC will supply customers in the Mid-Atlantic region. It now has 32 large DCs across all three countries where it operates, with two more on the way in Texas and an expansion of a DC in Florida. It’s all part of going where the customers are.

Lastly, related to all the store and DC openings, are rising construction costs. A new store four years ago cost less than one today. To counter inflation, it has acquired many former Rite Aid drug store leases and is converting them into retail locations, often faster and cheaper than a new build.

Ultimately, the expansion should lead to a higher market share. In 2025, its same-store sales increased by 4.7%, up 180 basis points from 2024. In 2026, it’s projecting 4.0% same-store sales growth.

At the very least, ORLY now provides a growth-at-a-reasonable-price (GARP) trade.

The Reasons Why Investors Should Wait

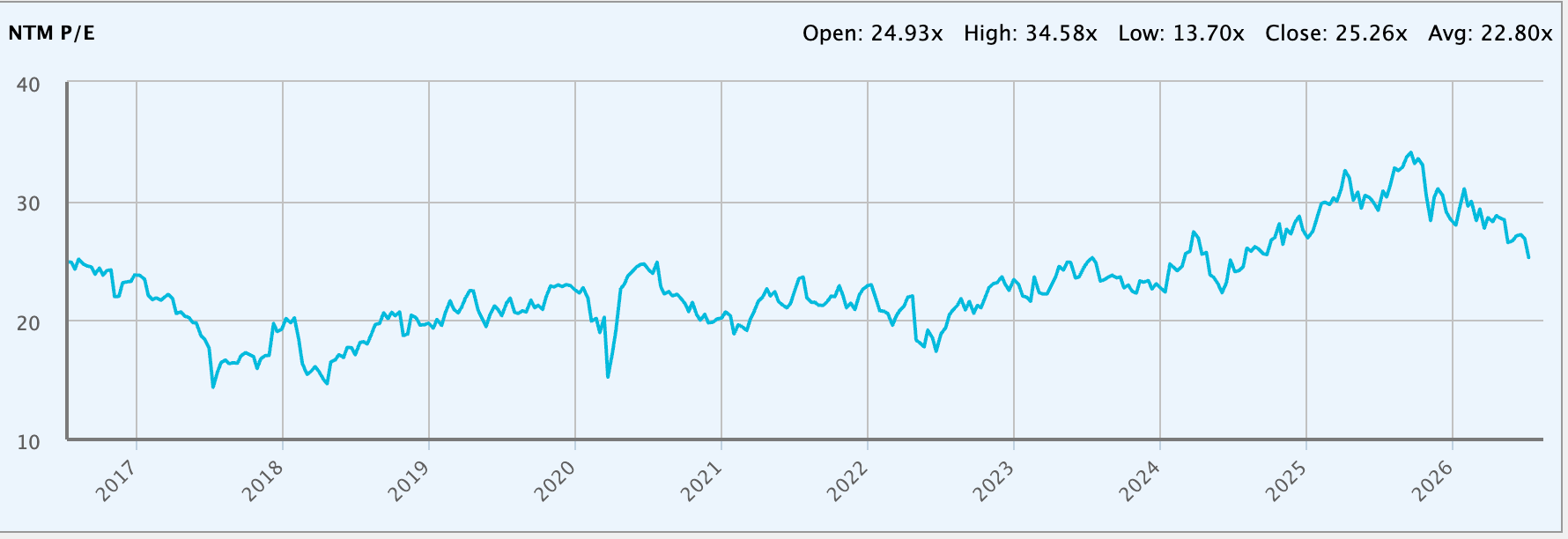

Looking at ORLY’s 10-year chart of forward P/E below, you can see that between 2016 and 2023, the multiple ranged from 15x to 25x its forward earnings per share estimate. From 2024 through today, the multiple has expanded to a range of 22x to 35x earnings.

Source: S&P Global Market Intelligence

As it’s fallen to 25.26x over the past nine months, investors are left to wonder whether it isn’t reverting to the mean, permanently resetting to the multiples seen between 2016 and 2023.

Two things come to mind that could be headwinds to ORLY’s forward P/E multiple: 1) Lower margins, and 2) Higher adoption of electric vehicles (EVs).

In terms of gross margins, there has been a little slippage over the past decade -- it hit a 10-year high of 53.1% in 2019, 150 basis points higher than in the trailing 12 months ended March 31 -- but nothing to be too concerned about given top-line revenue has grown by nearly 80% over this time. Furthermore, its EBIT (earnings before interest, taxes, depreciation and amortization) margin is hanging tough at 19.6% as of March 31, 70 basis points higher than in 2019, and not much lower than the 10-year high of 22.0% in 2021.

The biggest unknown is the acceleration of EV adoption over the next decade. BloombergNEF forecasts that EV adoption (fully electric and plug-in hybrid) in the U.S. by 2030 will be just 17%, down from the 2030 projection of 47.4% two years ago.

That’s actually good news for O’Reilly because EVs require far fewer repairs as they don’t have as many serviceable parts as internal-combustion-powered vehicles. That’s not to say that O’Reilly won’t capture a large share of the EV aftermarket as adoption rates increase, just that the revenue per DIY customer will likely be much lower.

I think it’s safe to say that O’Reilly has a decade or more to figure out how to make the most of a world undergoing an EV transition.

The Bottom Line on O’Reilly Stock

Although a good past performance doesn’t guarantee future returns, the fact that ORLY stock has an annualized total return of 16.84% over the past five years, 366 basis points higher than the SPDR S&P 500 ETF Trust (SPY) -- although it’s a little closer (91 basis points) over 10 years -- speaks volumes about its quality.

I’ve always liked businesses like O’Reilly because they service two markets -- Professional (50% of revenue) and DIY (50%) -- that aren’t going away despite technological innovation. So, the current expansion phase is unlikely to end anytime soon.

Analysts expect it to grow earnings per share by 44% from $3.26 in 2026 to $4.70 in 2030. That’s reasonable growth at a reasonable price.

With a median 12-month target price of $110, you’re getting in at a good time, but you’ll want to put aside some dry powder should Barchart’s 100% Strong Sell technical opinion turn out to be accurate. As for the $10 billion acquisition, it will add to debt, so that's something to consider if looking to buy ORLY.

Either way, I like ORLY for buy-and-hold investors.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)