/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

Shares of software giant Oracle Corporation (ORCL) have faced a brutal selloff lately, even though the company’s fundamentals remain pretty much intact. Even as the software giant continues to deliver record revenue and explosive cloud growth, investors have been heading for the exits, worried that Oracle’s aggressive artificial intelligence (AI) spending could come back to haunt it. The concern isn’t that demand is fading. It’s that Oracle is spending at a breathtaking pace to keep up with it. Billions of dollars are being poured into expanding its cloud infrastructure, pushing capital expenditures to record highs.

That spending has pushed free cash flow into negative territory and forced the company to rely on debt and equity financing, raising concerns about whether its AI investments will generate strong enough returns. Investors are also keeping a close eye on Oracle’s rapidly growing backlog. While it reflects robust demand, much of the recent surge has been driven by a small number of large AI customers. Those mega deals have fueled impressive growth, but it also means Oracle is increasingly dependent on a small group of deep-pocketed clients to keep the momentum going.

Those fears have certainly taken a toll on the stock, with Oracle shares plunging more than 50% from their 52-week high as concerns over ballooning AI investments and the sustainability of the AI boom overshadowed the company's strong fundamentals. That being said, not everyone thinks the selloff is justified. Piper Sandler recently defended its "Overweight" rating on Oracle, arguing that the market is underestimating the company’s cloud opportunity.

The firm believes Oracle could generate roughly $2.2 billion in Oracle Cloud Infrastructure (OCI) revenue that isn’t yet reflected in consensus estimates. While analyst Billy Fitzsimmons acknowledged investor concerns around capital intensity, AI monetization, customer concentration, and margins, he remains optimistic, citing OCI’s accelerating growth, Oracle’s new CFO, and solid expectations for the applications business in fiscal 2027. So, given Piper Sandler’s optimism despite market concerns, let’s take a closer look at Oracle.

About Oracle Stock

Founded in 1977, Oracle has evolved from a pioneer in database software into one of the world’s largest enterprise technology companies. Headquartered in Austin, Oracle provides cloud infrastructure, enterprise applications, and database software that power businesses across industries, from banks and retailers to healthcare providers and governments. But over the past decade, Oracle has shifted its focus from traditional on-premise software to cloud computing.

Today, the company’s biggest priority is expanding its cloud infrastructure business, particularly Oracle Cloud Infrastructure (OCI), as demand for AI computing accelerates. To support that growth, Oracle has ramped up investments in data centers and AI infrastructure, betting that rising enterprise spending on AI will drive its next phase of growth. While that strategy has boosted cloud revenue, it has also sparked concerns over the scale of the company’s capital spending, making Oracle one of Wall Street’s most closely watched AI stocks.

Oracle’s aggressive push into AI and cloud infrastructure has come at a steep cost. While the company is investing heavily to capitalize on the next wave of enterprise computing, investors have grown increasingly uneasy over surging capital expenditures, mounting cash burn, and the near-term pressure on profitability. As a result, the stock has faced a relentless selloff, despite the company’s long-term growth ambitions.

The market's skepticism is reflected in Oracle’s share price. With a market capitalization of approximately $414.1 billion, the stock has plunged 58.2% from its 52-week high of $345.72, reached last September. Oracle has also significantly underperformed the broader market, falling 39.4% over the past year while the S&P 500 Index ($SPX) has gained 20%. The trend has continued in 2026, with Oracle shares down 26.2%, compared with the broader market’s 10% return over the same period.

A Record Quarter Wasn’t Enough to Calm Oracle Investors

If Oracle’s latest earnings report proved anything, it’s that the company’s business isn’t slowing down. When the software giant reported its fiscal 2026 fourth-quarter results on June 10, it delivered another blowout quarter, comfortably topping Wall Street’s expectations on both revenue and earnings as demand for its cloud and AI offerings continued to accelerate. Total revenue climbed 21% year over year to a record $19.18 billion, edging past analysts’ consensus estimate of $19.08 billion.

Profit growth was just as impressive. GAAP earnings per share (EPS) rose 21% to $1.45, while non-GAAP EPS jumped 24% to a record $2.11, handily beating the Street's estimate of $1.96. The biggest highlight was once again Oracle Cloud Infrastructure (OCI). As companies ramped up spending on AI training and inferencing, Oracle’s total cloud revenue surged 47% to a record $9.9 billion. OCI was the clear growth engine, with revenue skyrocketing 93% year over year to $5.8 billion.

That explosive expansion more than offset a modest 2% decline in legacy on-premise software license revenue, underscoring Oracle’s successful transformation into a cloud-first company. The company’s future revenue pipeline also reached unprecedented levels. Oracle’s remaining performance obligation (RPO), a measure of contracted revenue yet to be recognized, ballooned to $638 billion as of May 31, marking a remarkable 363% increase from a year earlier.

However, the figure comes with an important caveat. A significant portion of that backlog is tied to a single customer, ChatGPT maker OpenAI, which is itself burning through substantial amounts of cash. While those large AI contracts have fueled Oracle’s rapid growth, they have also heightened concerns about customer concentration. But why did the stock tumble more than 8% on June 11 despite such stellar results?

The answer lies not in Oracle’s operating performance, but in the enormous price tag attached to its AI ambitions. Alongside its earnings, the company said it expects to raise $40 billion through debt and equity financing in fiscal 2027, including the previously announced $20 billion share sale. That comes after Oracle already raised $43 billion in debt and $5 billion in equity during fiscal 2026, amplifying investor concerns over whether AI demand will ultimately generate enough returns to justify such aggressive spending.

The pressure is already evident in Oracle’s cash flows. Free cash flow for fiscal 2026 was deep in the negative territory at $23.7 billion as the company continued pouring billions into expanding its cloud infrastructure to support surging AI workloads. Even so, management remains firmly optimistic. Oracle reaffirmed its fiscal 2027 revenue target of $90 billion and raised its non-GAAP EPS guidance to $8.05, implying 18% earnings growth.

How Do Analysts View Oracle Stock?

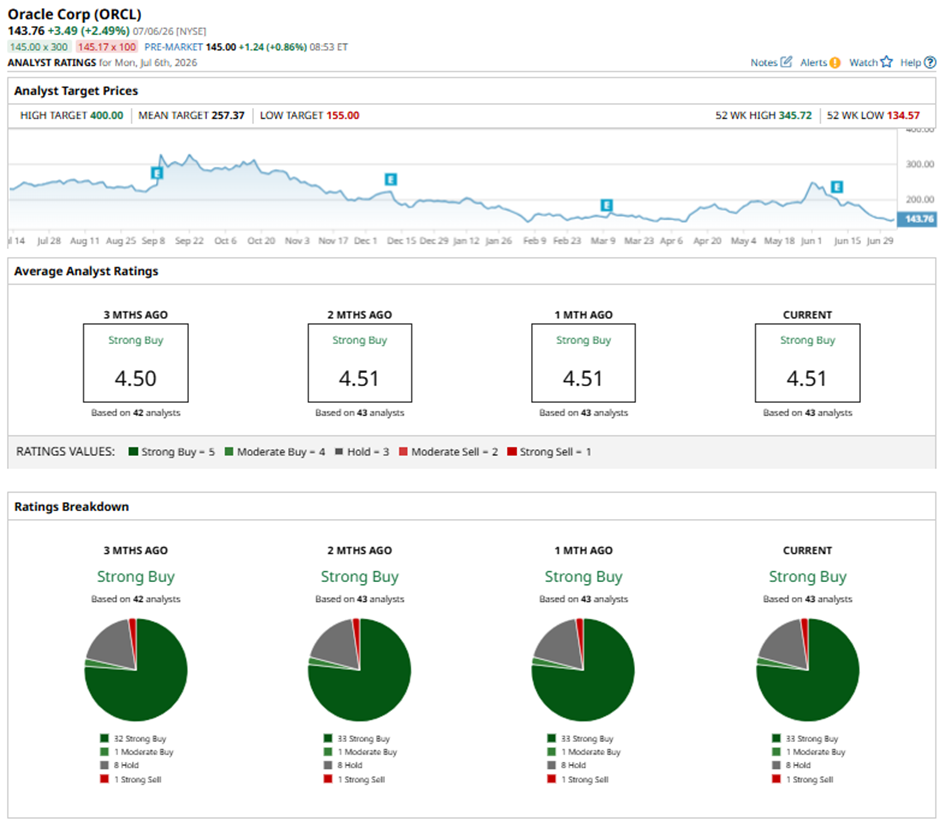

While investors have grown cautious, Wall Street’s confidence in the company remains largely intact. The stock carries a consensus “Strong Buy” rating, with 33 of 43 analysts recommending “Strong Buy,” one assigning “Moderate Buy,” eight maintaining “Hold,” and just one issuing a “Strong Sell.” Analysts also see substantial upside ahead, with the average price target of $257.37 implying a 79% gain from current levels. And the Street-high target of $400 suggests the stock could rally as much as 178.2% from here.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)