/The%20Adobe%20logo%20on%20a%20smartphone%20screen%20by%20filins%20via%20Adobe%20Stock.jpeg)

Adobe (ADBE) has been under scrutiny as investors remain split between fears that generative artificial intelligence (AI) could disrupt its creative-software empire and hopes that the company will emerge as one of the biggest beneficiaries of the technology shift. That debate may be starting to tilt in Adobe’s favor.

HSBC recently upgraded Adobe to “Buy” from “Hold” and raised its price target to $308 from $282, arguing that concerns about AI-powered rivals have become overblown and that Adobe’s entrenched workflows, massive user base, and rapidly expanding AI features make the platform far more resilient than many investors assume.

The analysts also highlighted 13.1% year-over-year (YoY) growth in total and current remaining performance obligations (RPO) in Q2, indicating sustained demand. Although Adobe’s AI-first revenue tripled YoY, it still represented only about 2% of Q2 revenue, suggesting AI features are complementing, rather than replacing, customers’ existing usage patterns.

As Adobe embeds AI deeper into Photoshop, Illustrator, Premiere Pro, and its broader Creative Cloud ecosystem, the company could be positioned to monetize AI disruption at scale.

About Adobe Stock

Adobe is a leading software company headquartered in San Jose that develops creative, document management, and digital experience solutions for individuals and enterprises. Its flagship products include Creative Cloud, Document Cloud, Acrobat, Photoshop, Illustrator, Premiere Pro, and the AI-powered Firefly platform, serving millions of creators, businesses, and marketers worldwide. Adobe has increasingly embedded generative AI capabilities across its software ecosystem to enhance productivity and strengthen customer engagement. The company had a market cap of around $86.7 billion.

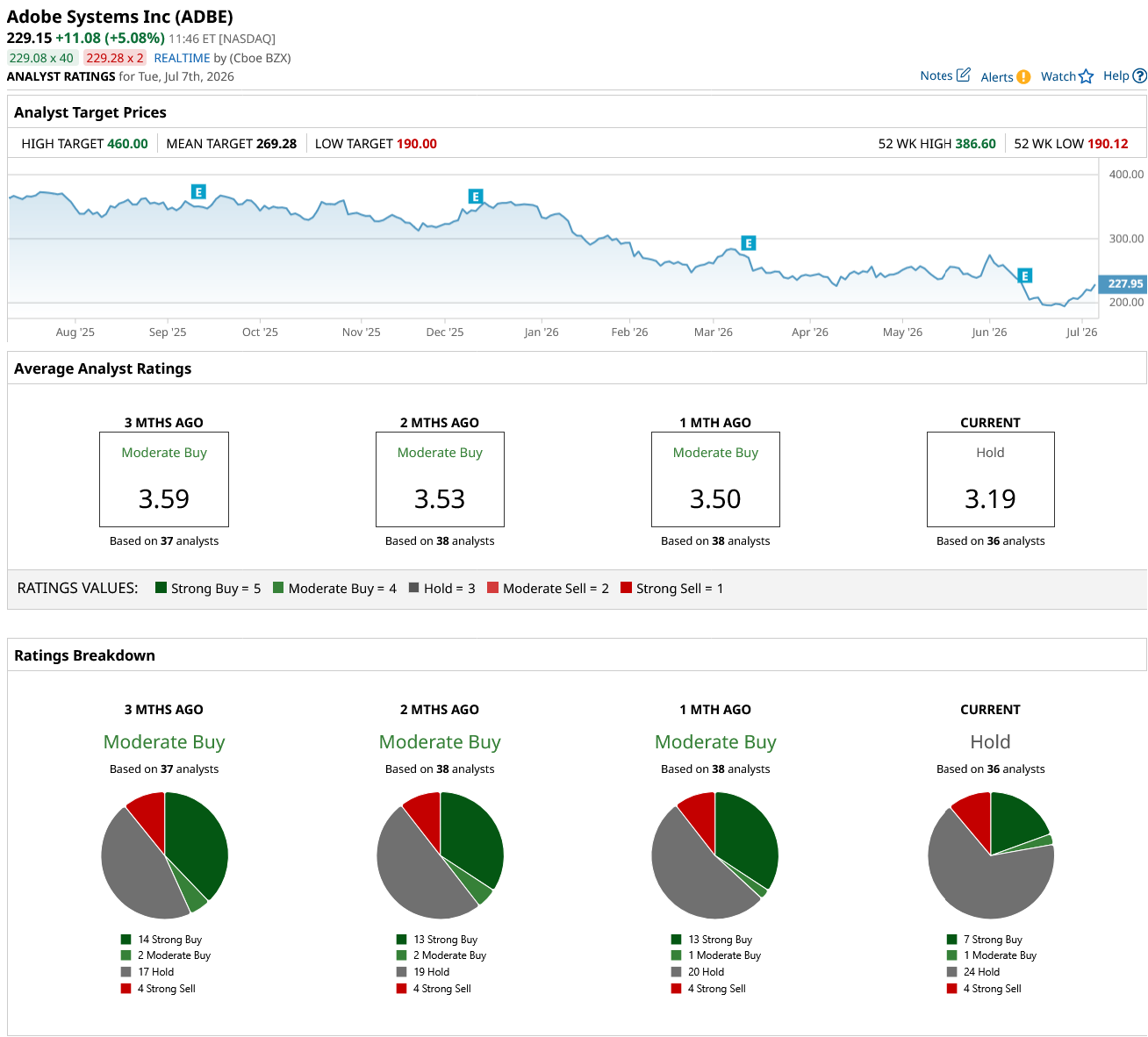

Adobe’s stock has significantly underperformed the broader sector over the past year as investors worried that generative AI could erode demand for its creative software franchise. The shares are down around 41% over the past 52 weeks and have declined about 36% year-to-date (YTD), reflecting concerns over AI competition, executive turnover, and valuation compression.

However, sentiment has begun to improve recently. ADBE stock has gained 8.5% over the past five trading days, including a 4.1% rally on July 2, after HSBC upgraded the stock and argued that the market is overestimating the threat from AI-powered design tools. The firm said Adobe’s strong customer retention, growing AI monetization, and resilient financial performance position it to benefit from AI rather than be disrupted by it.

ADBE stock is seeing another rally today, and it is up about 5% as of this writing.

The stock is currently trading at a discounted valuation compared to industry peers at 11.10 times forward earnings.

Better-than-Expected Q2 Earnings Report

Adobe reported strong fiscal second-quarter 2026 results on June 11, beating Wall Street’s expectations and raising its full-year outlook. Revenue increased 13% YoY to a record $6.6 billion, while non-GAAP EPS rose 17.8% to $5.96.

Total RPO climbed 13.1% YoY, reflecting healthy future demand, while AI-first ARR tripled from a year earlier to over $500 million. Adobe also highlighted continued strength across its subscription business and enterprise customer base, underscoring that AI is driving incremental demand rather than disrupting its core franchise.

Furthermore, Adobe guided for fiscal Q3 2026 revenue of $6.67 billion to $6.72 billion and non-GAAP EPS of $6.05 to $6.10. The company also raised its full-year fiscal 2026 guidance, forecasting revenue of $26.5 billion to $26.6 billion and non-GAAP EPS of $24.35 to $24.45, citing strong adoption of its AI offerings across Creative Cloud, Document Cloud, and Digital Experience. Adobe projected total ending ARR growth of 10.2% YoY for fiscal 2026.

Despite the beat-and-raise quarter, ADBE stock declined following the earnings release as investors focused on the departure of CFO Dan Durn and continued concerns about AI competition. The stock slumped 6.8% on June 12.

Analysts predict EPS to be around $19.80 for fiscal 2026, up 15.1% YoY, before surging by another 13% annually to $22.37 in fiscal 2027.

What Do Analysts Expect for ADBE Stock?

Although HSBC’s contrarian vote of confidence has boosted ADBE stock's price performance recently, most analysts are taking a cautious stance.

Last month, Wolfe Research downgraded ADBE to “Peer Perform” from “Outperform,” citing a more cautious outlook following the company’s fiscal Q2 results. While the firm remains optimistic about Adobe’s long-term Creative Cloud and Marketing Cloud franchises, it believes the quarter altered its investment thesis due to uncertainty surrounding strategic changes amid executive transitions, slowing growth without significant margin expansion, and a lack of meaningful near- to medium-term catalysts.

Also, following Adobe’s fiscal Q2 earnings, Freedom Broker downgraded the stock to “Hold” from “Buy” and slashed its price target to $250 from $510, arguing that recent growth was driven more by acquisitions than organic expansion.

Meanwhile, UBS reiterated its “Neutral” rating but lowered its price target to $225 from $260, citing concerns that the rise of creative AI tools is eroding Adobe’s pricing power, particularly among individual and lower-end customers.

Overall, ADBE stock has a consensus “Hold” rating. Of the 36 analysts covering the stock, seven advise a “Strong Buy,” one suggests a “Moderate Buy,” 24 give it a “Hold” rating, and four recommend a “Strong Sell.”

The average analyst price target of $269.28 indicates an upside of 18%, and the Street-high target price of $460 suggests that the stock could rally as much as 101%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)