/CPU%20Chip.jpg)

When the U.S. government acquired a stake in Intel (INTC), the technology company was struggling as compared to advances in the sector. The last few quarters have been about catching up to make Intel relevant in the world of AI. Backed by the leadership of Lip-Bu Tan, INTC stock has returned 416% in the last 52 weeks.

While the stock looks like it might be taking a breather, INTC is down about 14% in the past week; the uptrend seems to be far from over. Recently, HSBC reiterated its “Buy” rating for INTC stock and raised the price target to $200. HSBC analyst Frank Lee believes that there is “more value stemming from the semiconductor giant's servers and foundry operations.”

Lee has raised the company’s 2026 server CPU shipment growth estimate from 20% to 25% on a year-on-year (YoY) basis. Further, for 2027, the server CPU shipment growth estimate is from 20% to 30%. In addition to this, the narrative for the foundry segment is “improving.” Given the growth potential, the overall outlook seems bullish for Intel.

About Intel Stock

Headquartered in Santa Clara, California, Intel designs, manufactures, markets, and sells CPUs and other semiconductor solutions. The company’s business is divided into three reportable segments: CCG, DCAI, and Intel Foundry.

The CCG delivers platforms and processors that power PCs and edge devices. Further, the DCAI delivers workload-optimized solutions based on Intel’s x86 architecture for data centers. Finally, the Foundry segment develops new leading-edge semiconductor process technologies and advanced packaging technologies.

With an evolving technological landscape, Intel is focused on revitalizing the x86 ecosystem, boosting the external foundry business, and expanding market opportunities by developing purpose-built ASICs and GPUs for customers. The company is focused on addressing the hardware diversity of AI-driven compute workloads.

For FY25, Intel reported revenue of $52.8 billion. For the same period, the company’s operating cash flow was $9.7 billion. As Intel focuses on growth acceleration backed by significant industry tailwinds, INTC stock has surged by 165% in the last six months.

Positive Business Momentum to Sustain

An important point to note is that Intel has delivered earnings surprises in the last few quarters. This is reflective of the sustained improvement in business momentum. Further, analyst estimates point to potential earnings growth of 625% and 53.97% for FY26 and FY27, respectively. With these projections, it’s likely that the sentiment for INTC stock will remain positive.

Among growth drivers, Intel Foundry can be a potential game-changer. In June 2026, Seok-Hee Lee was appointed as executive vice president of Intel Foundry. This appointment is likely to support accelerated development and manufacturing. With strong demand for advanced packaging, the division has significant headroom for growth. As of Q1 FY26, the company’s 14A and 18A progress was “ahead of expectations.”

From a credit perspective, Intel reported cash and short-term investments of $32.8 billion as of March 2026. Further, considering Q1 FY26 operating cash flows of $1.1 billion, the annualized cash flow potential is in the range of $4.5 to $5 billion. Therefore, there is ample flexibility for investment in innovation and manufacturing expansion.

In terms of EBITDA margin and cash flow potential, Intel Foundry can be the biggest catalyst. To put things into perspective, the division reported Q1 FY26 revenue and operating loss of $5.4 billion and $2.4 billion, respectively. With advanced packaging likely to command robust margins, the division is likely to boost cash flows as production volume is ramped up.

What Do Analysts Say About INTC Stock?

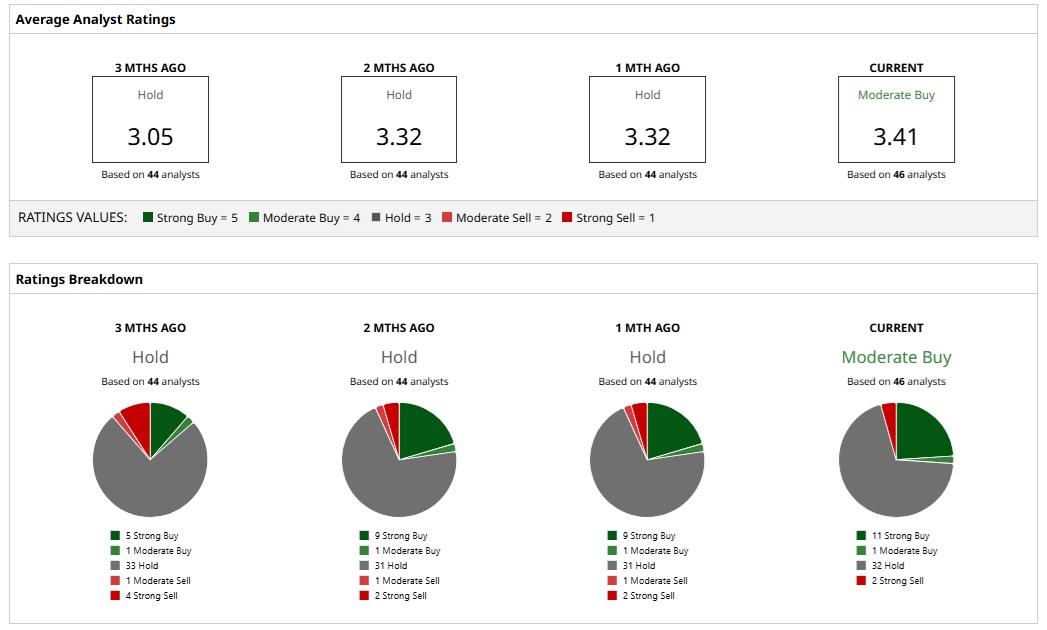

Based on 46 analysts with coverage, INTC stock has a consensus “Moderate Buy” rating. While 11 analysts have a “Strong Buy” rating for the stock, one has a “Moderate Buy,” 32 have a “Hold,” and two analysts have a “Strong Sell” rating.

The mean price target of $102.87 represents a downside potential of 8% from current levels. However, the most bullish price target of $200 suggests that INTC stock could climb as much as 79% from here.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)