/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Analysts covering Micron Technology (MU) continue to raise their annual revenue forecasts for Aug. 2027 as well as their price targets. But MU stock is off its peak. That presents an opportunity for value buyers.

For example, 2-week out-of-the-money MU puts now yield over 5.8% for short-sellers. This article will show how that works.

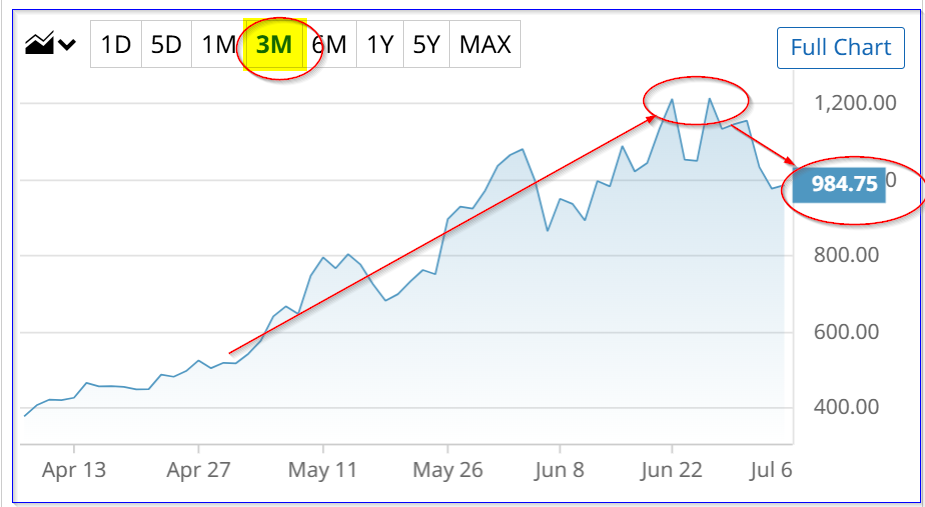

MU stock closed at $984.75 on Monday, July 6, well below its recent peak price of $1,209.19 on June 25. However, it could be worth substantially more based on its free cash flow (FCF) margins and analysts' revenue forecasts.

Higher Analyst Revenue and Price Targets for Micron

I have written several Barchart articles where I showed how I set a price target for MU stock based on these two inputs.

For example, on June 26, I wrote an article ("Micron Skyrockets After Huge Revenue Upgrade - Could MU Be Worth $2,500 Per Share?) where I showed that MU could be worth between $2,251 and $2500 per share over the next few years

That was based on $225.71b FY 27 revenue forecasts and either a 45% FCF margin or a 50% FCF margin. I used a 4% FCF yield metric to derive a fair market value (FMV).

However, since then, analysts have raised their FY 2027 revenue forecasts to $234.24 billion.

As a result, using a lower 45% FCF margin assumption, and a 4% FCF yield metric, Micron could be worth:

$234.24b x 0.45 = $105.4 billion FCF

$105.4b / 0.04 = $2,625 billion fair market value (FMV)

That is still 136% over Micron's market cap today of $1,112 billion, according to Yahoo! Finance. In other words, the price target is 136% over today's price:

$984.75 x 2.36 = $2,304.31 price target (PT)

However, using a 50% FCF margin assumption, it could be worth significantly more:

$234.24b x 0.50 = $117.12b FCF

$117.12b / 04 = $2,938 billion FMV

$2,938b / $1,112b = 2.633x;

984.75 price x 2.633 = $2,592.85 PT

So, now, based on higher revenue price targets, MU is worth between $2304 and $2,593 per share.

Moreover, analysts have substantially raised their price targets. For example, Yahoo! Finance reports that the average of 45 analysts is now $1,486.00. That is up from $828.72, as seen in my June 14 Barchart article. Similarly, Barchart's mean analyst survey price is now $1,416.39, up from $872.77 on June 14.

In addition, AnaChart, which tracks recent analyst write-ups, shows an average PT of $1,234.45 from 28 analysts.

The bottom line is that analysts have now raised their price targets well over the present stock price. You can see why. Their own revenue forecasts are substantially higher. In other words, they expect to see high memory chip prices for at least the next year.

Shorting 2-Week OTM Puts for High Yields

I discussed shorting 2-week expiry puts in my June 14 Barchart article. That play worked out well, with investors making a 2-week 7% yield for 5% out-of-the-money (OTM) puts. This play can now be repeated.

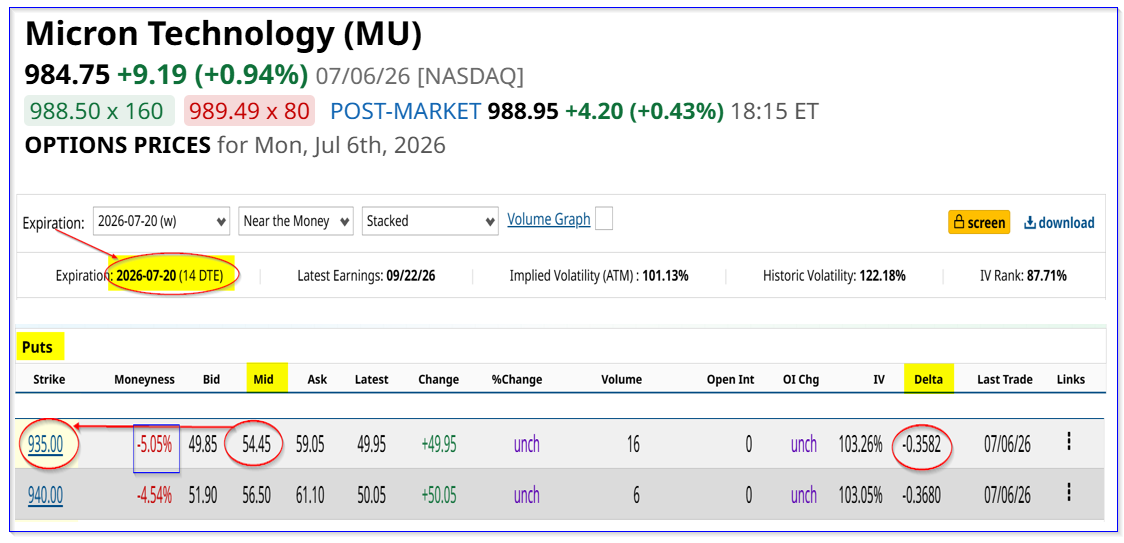

For example, look at the July 20 expiry period. It shows that the $935.00 strike price, which is over 5% lower than today's price, has a midpoint premium of $54.45. That provides an investor (who can post the collateral) a 2-week yield of over 5.82%:

$54.45/$935.00 = 0.058235 = 5.8235% 2-week yield

However, to earn this income, an investor must first post $93,500 in cash or buying power with their brokerage firm. That allows the account to have collateral to buy 100 shares at $935.00, in case MU stock drops to that point on or before July 20.

In return, the account will immediately receive $5,445. So, the net potential cost is only:

$93,500 = $5,445 = $88,055 breakeven point

In other words, if MU falls to $935.00 and the account is assigned to buy 100 shares using the $93.5k in collateral, the investor's net per-share breakeven cost will only be $880.55 per share.

That is a great buy-in cost, over $104 lower than today's price ($984.75), or -10.58% lower.

Downside Risks

However, there are downside risks. For one, the delta ratio is high. At -0.3582, it implies there is almost a 36% chance, based on prior volatility in MU stock, that it could drop 5% in the next 2 weeks.

Moreover, if MU falls below the $880.55 breakeven point, the investor could end up with at least a temporary unrealized capital loss position (i.e., holding MU shares at a higher cost than the stock price).

Nevertheless, given the company's higher price targets and revenue forecasts, that might not last long.

One more potential upside point is that if Micron decides to do a stock split, lowering the stock price, it will be much easier to short out-of-the-money (OTM) puts. That could lower these high short-put yields.

The bottom line is that MU stock looks too cheap. Shorting puts looks like an attractive way to set a lower potential buy-in and make high yields. In this case, the 2-week yield is over 5.8%.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)