/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

Amazon.com (AMZN) has moved one step closer to giving Space Exploration Technologies (SPCX) a real run for its money. The company announced that it now has enough satellites in orbit to roll out the initial service of its Leo internet from space network later this year.

Amazon launched 29 satellites at around 12:30 a.m. EST on Thursday, July 2, aboard a United Launch Alliance Atlas V rocket. The successful mission expanded Amazon's constellation to more than 390 satellites, enough to support continuous service across its initial latitudes.

Even though the company still needs to raise the newly launched satellites to their assigned altitude, it has already completed enough launches to begin initial service this year.

Amazon first introduced the project as Kuiper in 2019 before later renaming it Leo. The satellite network aims to deliver high-speed, low-latency broadband to homes, businesses, and remote locations worldwide. It also stands as Amazon's most direct challenger to SpaceX's Starlink, which has enjoyed a sizable head start since launching in 2020.

Starlink started with nearly 900 satellites in low Earth orbit before expanding its constellation to more than 10,000 satellites, providing service across about 160 countries. Amazon, meanwhile, plans to deploy about 3,200 Leo satellites.

With hundreds of flight-ready satellites already waiting at the Cape and a dedicated vertical integration facility prepared to support Leo Vulcan 1 and future missions, Amazon believes it has a clear path to accelerate launches and expand network coverage following its initial service rollout later this year.

About Amazon Stock

Amazon might have started as an online bookstore, but that page turned long ago. Today, the company has a market cap of roughly $2.6 trillion and operates one of the world's largest retail marketplaces, an enormous logistics network, and a cloud infrastructure business.

The Seattle, Washington-based company also builds devices such as Kindle and Echo, creates digital media content, and delivers cloud computing, artificial intelligence (AI), data storage, and analytics services worldwide through Amazon Web Services (AWS).

On the price performance front, shareholders have enjoyed a rewarding journey. Amazon’s shares climbed 9.85% during the past 52 weeks. They also gained 6.3% year-to-date (YTD). Buyers stepped on the gas during the last three months as the stock advanced another 15.3%.

From a valuation standpoint, Amazon still trades at a premium. The stock is currently trading at 27.91 times forward adjusted earnings and 3.17 times sales. Both figures sit above broader industry averages and reflect investors' confidence in the company's scale, growth prospects, and market leadership.

Amazon Surpasses Q1 Earnings

Amazon came out swinging in Q1 FY2026, delivering another impressive quarter for investors. The stock rose 1.3% on April 29 after the company released its results. Net sales climbed 16.6% year-over-year (YOY) to $181.5 billion, ahead of Wall Street's estimate of $177.3 billion. EPS jumped 74.8% from the year-ago level to $2.78 and topped analysts' forecast of $1.64.

Coming to business segments, North America revenue increased 12.1% YOY to $104.1 billion. International sales rose 18.7% from the previous year to $39.8 billion and increased 11% after excluding foreign exchange impacts. AWS continued to carry plenty of weight as revenue surged 28.4% year over year to $37.6 billion.

Margins also headed in the right direction. Operating income grew 29.6% to $23.9 billion. Net income soared 76.7% from the year-ago level to $30.3 billion. Amazon also strengthened its financial position, with cash and cash equivalents increasing to $101.8 billion from $86.8 billion as of Dec. 31, 2025.

Looking forward, management expects Q2 FY2026 net sales between $194 billion and $199 billion, representing YOY growth of 16% to 19%. They project operating income between $20 billion and $24 billion compared with $19.2 billion in the year-ago quarter.

On the other hand, Wall Street expects Q2 FY2026 EPS to increase 8.3% YOY to $1.82. Analysts also forecast full-year FY2026 EPS of $7.75, representing 8.1% growth from the previous year. Furthermore, they estimate FY2027 EPS to climb another 30.2% to $10.09.

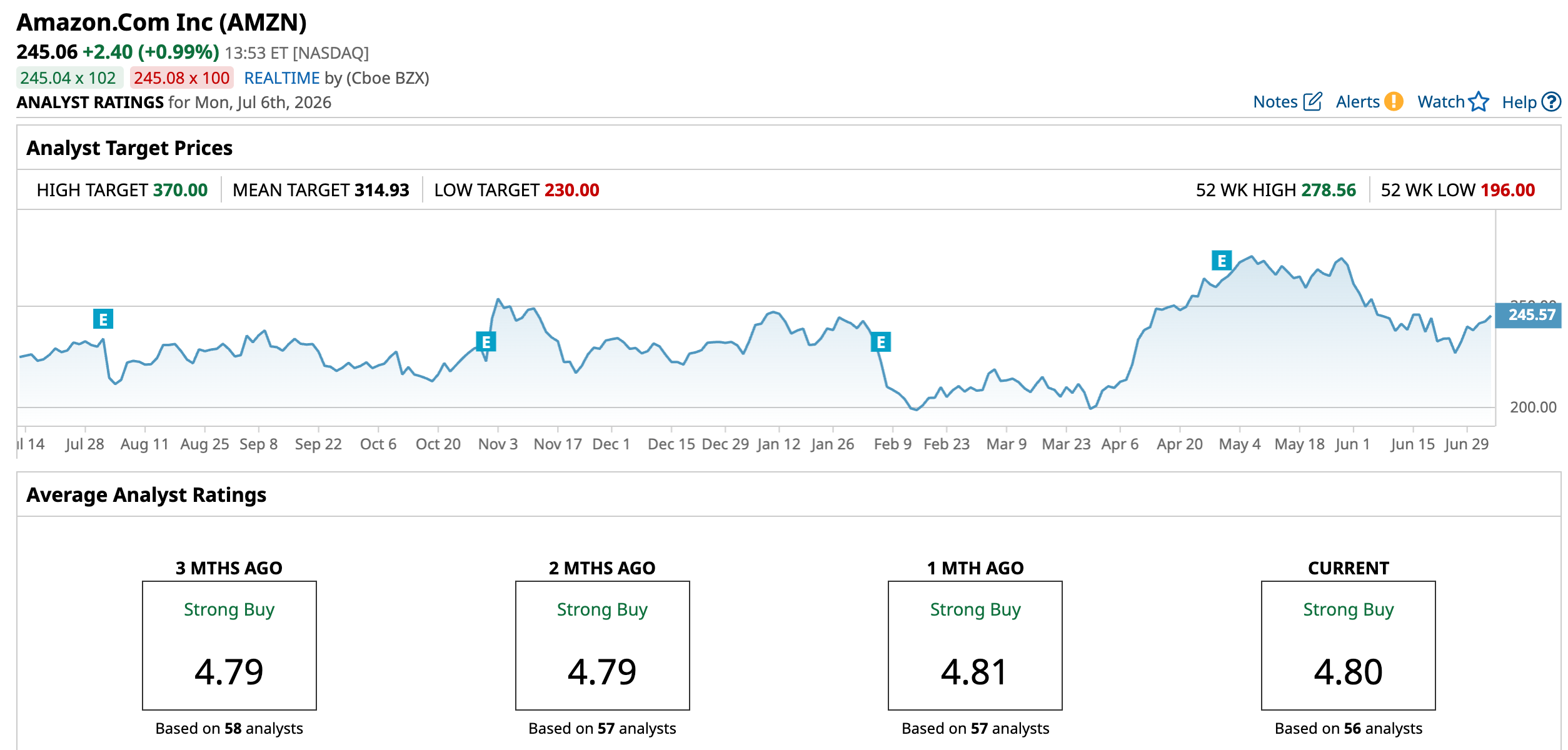

What Do Analysts Expect for Amazon Stock?

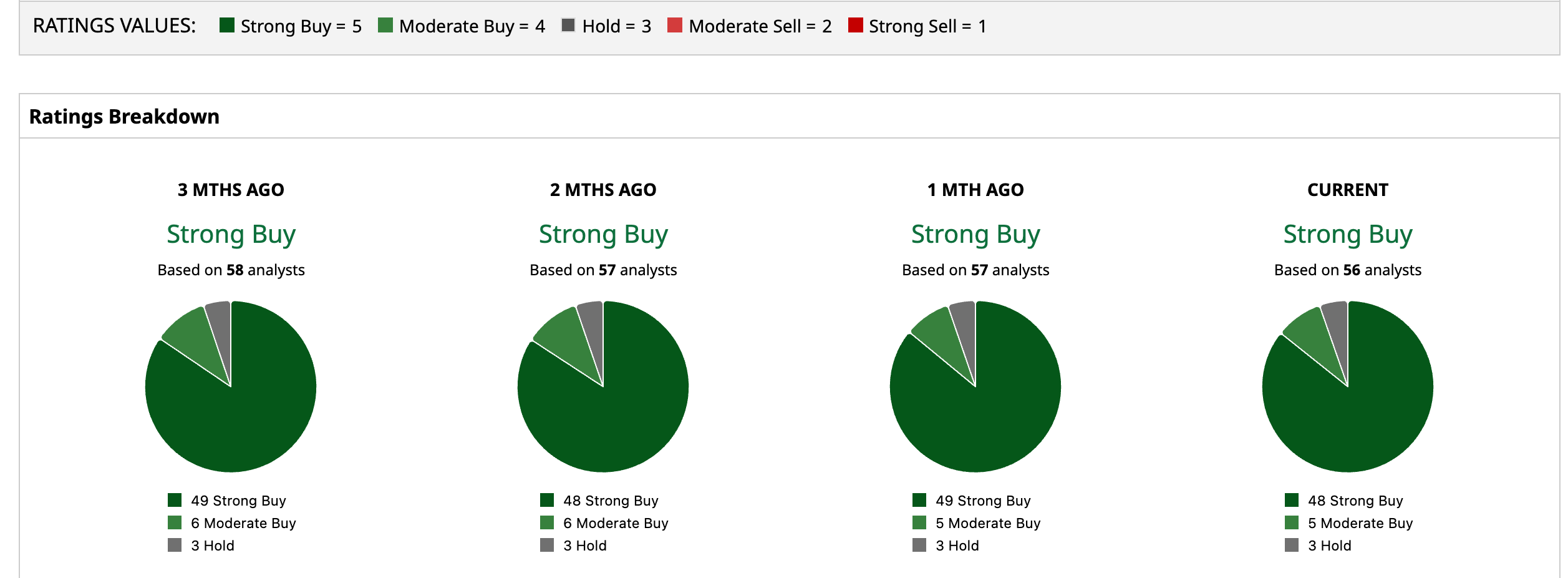

Wall Street is backing Amazon with plenty of conviction. Analysts have currently assigned the stock an overall “Strong Buy” rating. Among 56 analysts covering the company, 48 recommend “Strong Buy,” five suggest “Moderate Buy,” and three maintain “Hold” ratings.

To that end, the average price target of $314.93 signals potential upside of 28.5%. Meanwhile, the Street-High target of $370 implies a 51% gain from current levels if Amazon continues to meet expectations.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)