International Business Machines Corporation (IBM) investors should mark July 22 on their calendars as the technology giant prepares to report its second-quarter 2026 earnings, a closely watched update that could reveal whether its artificial intelligence (AI), hybrid cloud, and software businesses are generating enough momentum to justify the stock’s strong rally.

With enterprise demand for AI accelerating and IBM strengthening its consulting expertise, and next-generation infrastructure at the center of corporate AI adoption, Wall Street will be looking for signs of sustained revenue growth, expanding margins, and stronger free cash flow, while management’s outlook could provide fresh clues about the company’s growth trajectory for the second half of 2026.

About International Business Machines Stock

IBM is a global technology and consulting powerhouse headquartered in Armonk, New York. Founded in 1911 as the Computing-Tabulating-Recording Company and rebranded in 1924, IBM today operates in more than 170 countries and offers a broad portfolio spanning hybrid cloud platforms, AI solutions, infrastructure hardware, software, consulting services, and financing. IBM’s market cap is around $272.12 billion.

IBM shares have delivered a mixed performance in recent months. Although the stock has remained slightly positive over the past 12 months, it is up marginally 0.73% year-to-date (YTD) after pulling back from its record levels earlier this year.

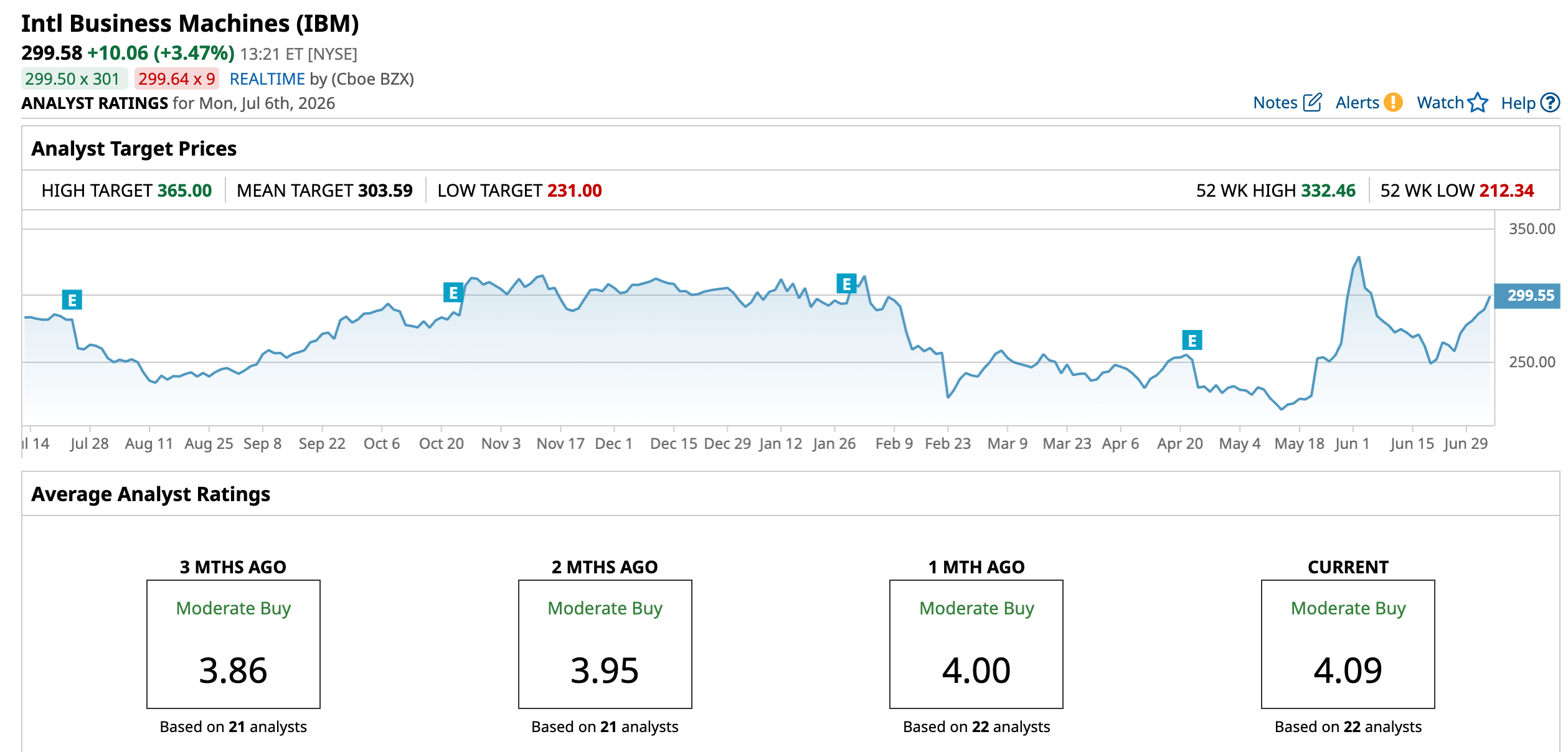

The stock climbed to a 52-week high of $332.46 on June 2, reflecting investor enthusiasm over IBM’s AI, hybrid cloud, and enterprise software growth prospects, before broader market volatility and profit-taking weighed on the shares. Since hitting the high, the stock retreated 9.9%.

Despite that correction, momentum has turned positive again, with IBM rallying 9.85% over the past five trading days as investors grew increasingly optimistic ahead of the company’s July 22 second-quarter earnings report, where management is expected to provide fresh insight into AI-driven demand and the company’s outlook for the remainder of 2026.

The stock is currently trading at a discounted valuation compared to industry peers at 23.35 times forward earnings.

Steady Q1 Results

IBM reported a stable start to fiscal 2026 when it released its first-quarter results on April 22 that exceeded Wall Street’s expectations.

Total revenue increased 9% year-over-year (YOY) to $15.92 billion. On a non-GAAP basis, operating EPS came in at $1.91, representing a 19% YOY increase and ahead of analysts’ expectations. Gross profit climbed to almost $9 billion from $8 billion, reflecting continued margin expansion.

IBM’s Software segment remained its primary growth engine, with revenue rising 11% YOY to $7.1 billion. Within Software, Hybrid Cloud (Red Hat) revenue grew 13%, Automation increased 10%, Data surged 19%, and Transaction Processing advanced 6%. Consulting revenue grew 4% to $5.3 billion, while Infrastructure revenue jumped 15% to $3.3 billion, supported by a 51% surge in IBM Z revenue as demand for the company’s latest mainframe platform remained strong. Financing revenue also increased 15% to $0.2 billion.

Also, cash generation improved. Net cash from operating activities increased to $5.2 billion from $4.4 billion in the prior-year quarter, while free cash flow rose to $2.2 billion, up $0.3 billion YOY. IBM returned $1.6 billion to shareholders through dividends during the quarter.

Furthermore, management reaffirmed its full-year 2026 outlook. IBM continues to expect more than 5% constant-currency revenue growth for the year. The company also maintained its forecast for free cash flow to increase by about $1 billion YOY in 2026, underscoring management’s confidence that demand for AI, hybrid cloud, and enterprise infrastructure solutions will continue to support growth throughout the remainder of the year.

Analysts predict EPS to be around $12.40 for fiscal 2026, up 7% YOY, before surging by another 8.3% annually to $13.43 in fiscal 2027. Plus, the consensus estimate of $3.02 for the second quarter indicates an increase of 7.9% from the prior-year quarter.

What Do Analysts Expect for IBM Stock?

Most recently, RBC Capital reaffirmed its “Outperform” rating on IBM with a $300 price target after the company joined the OpenAI Daybreak Cyber Partner Program. The firm views the partnership positively, as it strengthens IBM’s cybersecurity portfolio by integrating OpenAI’s advanced AI capabilities into enterprise security workflows.

Additionally, Barclays initiated coverage on IBM with an “Overweight” rating and a $350 price target, citing the company’s strong software-led business model and long-term growth potential.

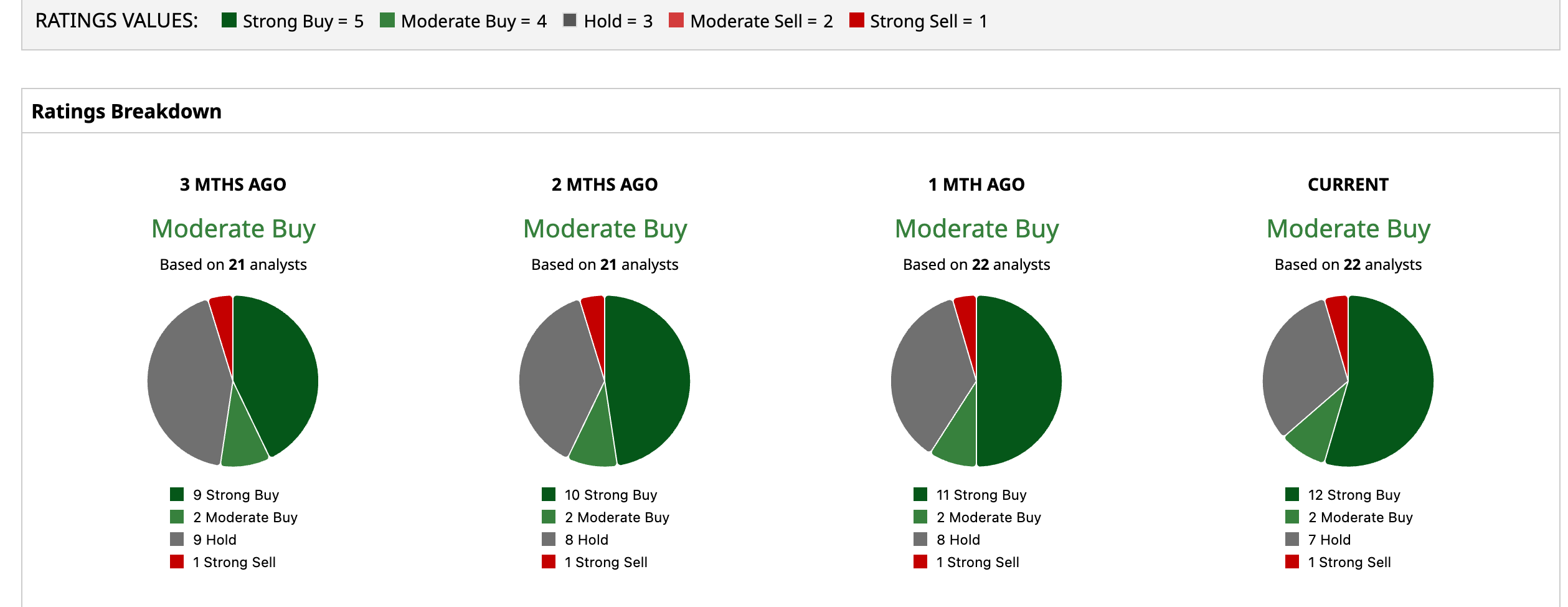

Wall Street is fairly bullish on IBM. Overall, IBM has a consensus “Moderate Buy” rating. Of the 22 analysts covering the stock, 12 advise a “Strong Buy,” two suggest a “Moderate Buy,” seven analysts are on the sidelines, giving it a “Hold” rating and one “Strong Sell.”

The average analyst price target of $303.59 indicates an upside of 1.34%, and the Street-high target price of $365 suggests that the stock could rally as much as 21.8%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.