Oil prices have moved well off their recent highs, with crude now trading in the $60-$70 range. That decline has eased concerns about headline inflation by reducing energy-related cost pressures across the economy. As inflation expectations have moderated, the market has become more comfortable pricing in a less restrictive Federal Reserve policy. According to CME Group's FedWatch tool, traders expect only one rate hike this year. In turn, demand for Treasuries has improved, supporting bond prices and helping push yields lower. The question becomes: have Treasury yields had time to react to the rapid decline in energy prices?

Seasonal factors also tend to favor lower Treasury yields during this period. The 10-year yield has a long history of drifting lower between late July and early September as trading volumes decline and many market participants reduce risk ahead of the fall. While this pattern is not guaranteed to repeat every year, it is a tendency that fixed-income traders and hedgers monitor closely. With fewer catalysts during the late summer, Treasury prices often find support unless unexpected economic data or policy developments shift market expectations.

The Treasury market may also receive technical support as the government's fiscal year-end on September 30 approaches. Funding needs and issuance patterns can influence supply-and-demand conditions, particularly as the Treasury continues to rely heavily on Treasury bills to manage short-term liquidity. While coupon issuance remains substantial, the combination of seasonal positioning, moderating inflation expectations, and fiscal year-end funding dynamics could continue to favor lower yields through early September before attention shifts to heavier issuance, economic data, and Federal Reserve policy later in the month.

10-Year Treasury Prices Technical Picture

Source: Barchart

The trend in 10-Treasury prices has been down (higher yields); the market did find support in May and has since made minimal higher highs and higher lows (lower yields). If the May lows hold, 10-Year Treasury prices have a good chance of continuing higher and flipping the 50-day simple moving average (SMA). Being patient and monitoring the daily trend to confirm the bottom is in may be a sensible bet here. There are many factors affecting these prices, and the prudent trader should seek a little more confirmation.

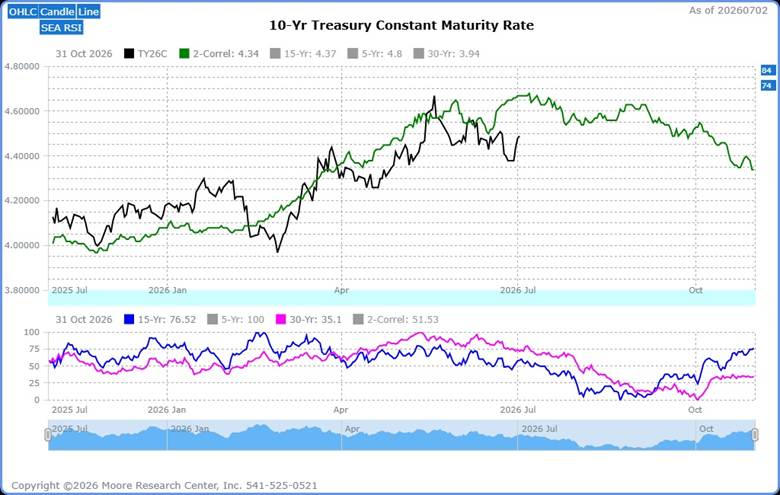

10-Year Yield Correlated Years

Source: Moore Research Center, Inc. (MRCI)

The chart above shows the yield of the 10-Year Treasury; it moves in the opposite direction to the 10-Year Treasury price. The yield (black line) had peaked out in May and has been correcting the recent rally. There are two years, 1984 and 1974, and if the market continues to follow these correlations, the path is toward lower yields. The chart below the yield shows the 15-year (blue) and 30-year (purple) seasonal patterns. Notice that, over 30 years, the seasonal pattern has been for yields to peak and then decline. That seems to be a fairly large sample size of price action. Can there be an anomaly, and will yields go higher this year? Of course, but the pattern is for lower yields.

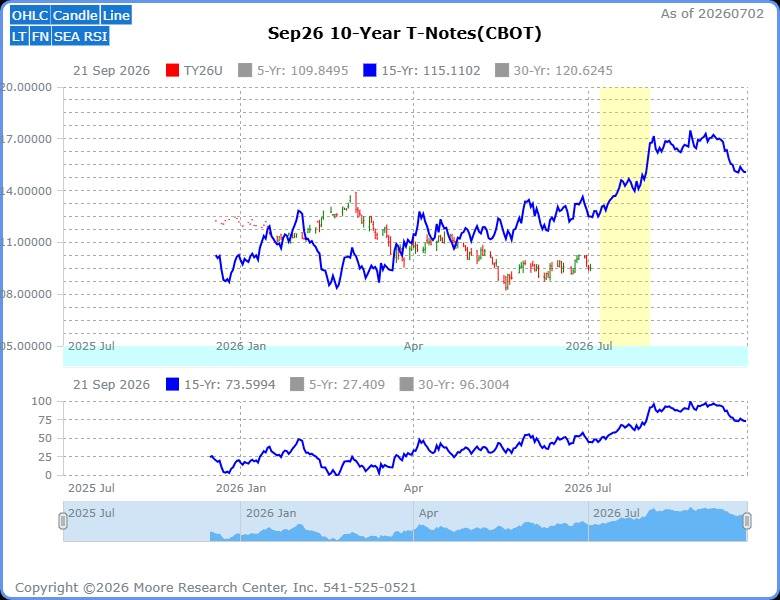

Optimal Seasonal Pattern

Source: MRCI

MRCI's research has found that 10-Year Treasury prices have risen during the summer months. An optimized window need not span the entire duration of a seasonal pattern. It does, however, filter out many setups to find not only the one with the optimal return but also the one with the fewest drawdowns during the trade.

The next optimal window (yellow box) for the 10-Year Treasury market was identified as July 07 to August 02. Remember that optimized windows are not exact entry and exit dates; they are optimized windows, which means the entry or exit price could be a few days before or after the optimal dates. For this year's seasonal buy, MRCI has found that the September 10-Year Treasury futures have closed higher on August 02 than on July 07 in 13 of the past 15 years, for an 87% occurrence.

As a crucial reminder, while seasonal patterns can provide valuable insights, they should not be the basis for trading decisions. Traders must consider technical and fundamental indicators, risk management strategies, and market conditions to make informed, balanced trading decisions.

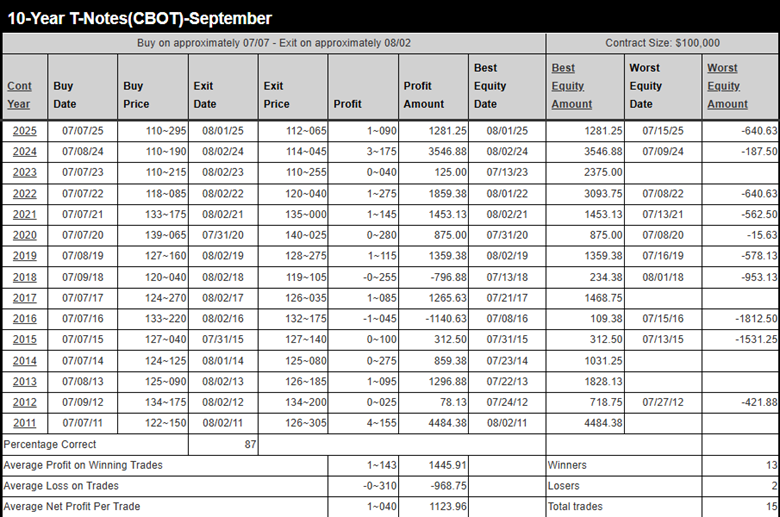

Source: MRCI

The results of the past 15 years of hypothetical price-action trading show that 5 years had no daily closing drawdowns. During this period, the average net profit per contract traded was $1,123.96.

Tradable Assets for Interest Rate Plays

For those looking to trade these dynamics, several instruments offer exposure to Treasury price movements:

- 10-Year Treasury Futures (ZN): Traded on the CME Group Exchange, these contracts allow traders to speculate on or hedge against changes in 10-year Treasury yields. They're highly liquid and sensitive to shifts in Fed policy.

- Micro-Yield Treasury Futures (TO): Also offered by CME Group, these smaller contracts provide a cost-effective way for retail traders to gain exposure to yield movements with lower capital requirements.

- TLT ETF: The iShares 20+ Year Treasury Bond ETF (TLT) tracks long-dated Treasuries, allowing investors to bet on rising bond prices without directly trading futures. It's accessible through most brokerage accounts. Due to the high correlation between the 10-, 20-, and 30-year Treasuries, the TLT can serve as a proxy for equity trades for traders.

- Options on TLT or Futures: Options provide leveraged exposure to Treasury price movements, allowing traders to speculate on volatility or hedge existing positions.

These instruments suit a range of risk profiles, from conservative hedging to speculative bets. Studying interest rate trends can enhance portfolio diversification, complementing equities or commodities. Challenge yourself to explore rates as an asset class—understanding their interplay with macroeconomic and geopolitical factors can unlock new opportunities.

In Closing…

The current market presents an opportunity worth watching. Falling energy prices, easing inflation expectations, seasonal tendencies, and supportive Treasury market dynamics are all pointing toward the possibility of lower yields into early September. While no seasonal pattern or historical correlation guarantees the same outcome this year, recognizing when multiple factors begin to align can help traders identify higher-probability setups before they become obvious to the broader market. As always, confirmation from price action, technicals, and evolving fundamentals should remain part of the decision-making process.

For many traders, interest rates remain one of the most overlooked asset classes despite their influence on nearly every financial market. Whether you're primarily active in equities, commodities, or currencies, adding Treasury products to your trading toolbox can provide valuable diversification and opportunities that often develop independently of other markets. The more you understand how yields respond to inflation, Federal Reserve expectations, and seasonal flows, the better positioned you'll be to capitalize on opportunities wherever they emerge.

On the date of publication, Don Dawson did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)