/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Mark Zuckerberg has spent the better part of two years telling investors that Meta Platforms (META) would rather own too much computing capacity than too little. Now that bet looks like it is turning into an actual business plan.

Meta is quietly building out a cloud computing division that would sell spare AI computing power and access to its own models to outside companies, according to a Bloomberg report.

If it moves forward, the plan would put Meta in direct competition with Amazon (AMZN) Web Services, Microsoft (MSFT) Azure, and Alphabet's (GOOG) (GOOGL) Google Cloud, three companies that have spent decades and hundreds of billions of dollars building the infrastructure Meta is eyeing in 2026.

Meta's Cloud Ambitions Take Shape

According to Bloomberg, Meta is weighing two different approaches:

- One would let outside developers pay to use AI models hosted on Meta's own servers, including its new Muse Spark models, similar to how Amazon's Bedrock service works today.

- The other option would sell access to raw computing capacity itself, the same model used by smaller specialized firms such as CoreWeave (CRWV).

- The effort reportedly falls under an internal program called Meta Compute, led by infrastructure chief Santosh Janardhan, Meta Superintelligence Labs leader Daniel Gross, and Meta President Dina Powell McCormick.

META stock gained almost 9% on the report but still trades 23% below all-time highs.

Why Meta Is Sitting on Spare Capacity

Meta has been on a spending spree to build data centers, buy chips, and lock in power deals, all in service of what Zuckerberg calls personal superintelligence.

During the company's first-quarter earnings call, Meta raised its full-year capital expenditure forecast to $125 billion to $145 billion, up from a prior range of $115 billion to $135 billion. Meta told analysts the increase was driven mostly by higher component costs, particularly memory pricing, and additional data center work to support capacity in future years.

The social media giant also disclosed that new cloud contracts and infrastructure purchase agreements added $107 billion to its contractual commitments in the quarter alone. Zuckerberg has hinted for months that selling excess compute was on the table.

On the earnings call, he said companies regularly approach Meta, either asking to buy computing power at a premium or to set up an API service similar to what OpenAI and Anthropic already offer.

He said Meta has held off because it believes it can put that capacity to use internally, but that the option remains open if the company ever determines it built more than it needs. Elon Musk's SpaceX (SPCX) has already started renting out computing power from its Memphis data center to Anthropic and Google, a strategy Bloomberg Intelligence estimates could generate more than $50 billion in revenue for xAI by 2028.

Meta appears to be angling for a similar payoff, treating its build-now, monetize-later approach to compute as both an insurance policy and a revenue opportunity.

Meta Takes on AWS, Azure, and Google Cloud

For years, Meta has been one of the biggest customers of the very companies it may soon compete with, striking major computing deals with CoreWeave (CRWV), Google, and Oracle (ORCL) to keep pace with its AI ambitions.

A shift toward selling capacity would mark a fundamental change in how Meta approaches its infrastructure and positions itself against the established cloud giants. Amazon, Microsoft, and Google built their cloud businesses over roughly two decades, layering on enterprise sales teams, developer tools, and global data center networks that now generate tens of billions of dollars in revenue every quarter.

Meta lacks that track record in enterprise cloud sales, though its scale and its own frontier models give it a starting point that few other challengers can match. Meta's massive AI spending has worried shareholders for much of the past year, given how far off the return on that investment has felt.

A cloud business built on selling spare capacity would give Meta another way to turn that spending into revenue rather than just an ongoing cost. Whether it becomes a serious rival to AWS and Azure or simply a side business that offsets some infrastructure costs will likely become clearer as Meta shares more details over the coming quarters.

Is META Stock Undervalued Right Now?

Analysts tracking META stock forecast revenue to increase from $201 billion in 2025 to $473 billion in 2030. In this period, adjusted earnings are projected to expand from $29.68 per share to $57.22 per share. If META is priced at 20x forward earnings, below its 10-year average of $23.6x, it could return around 90% within the next four years.

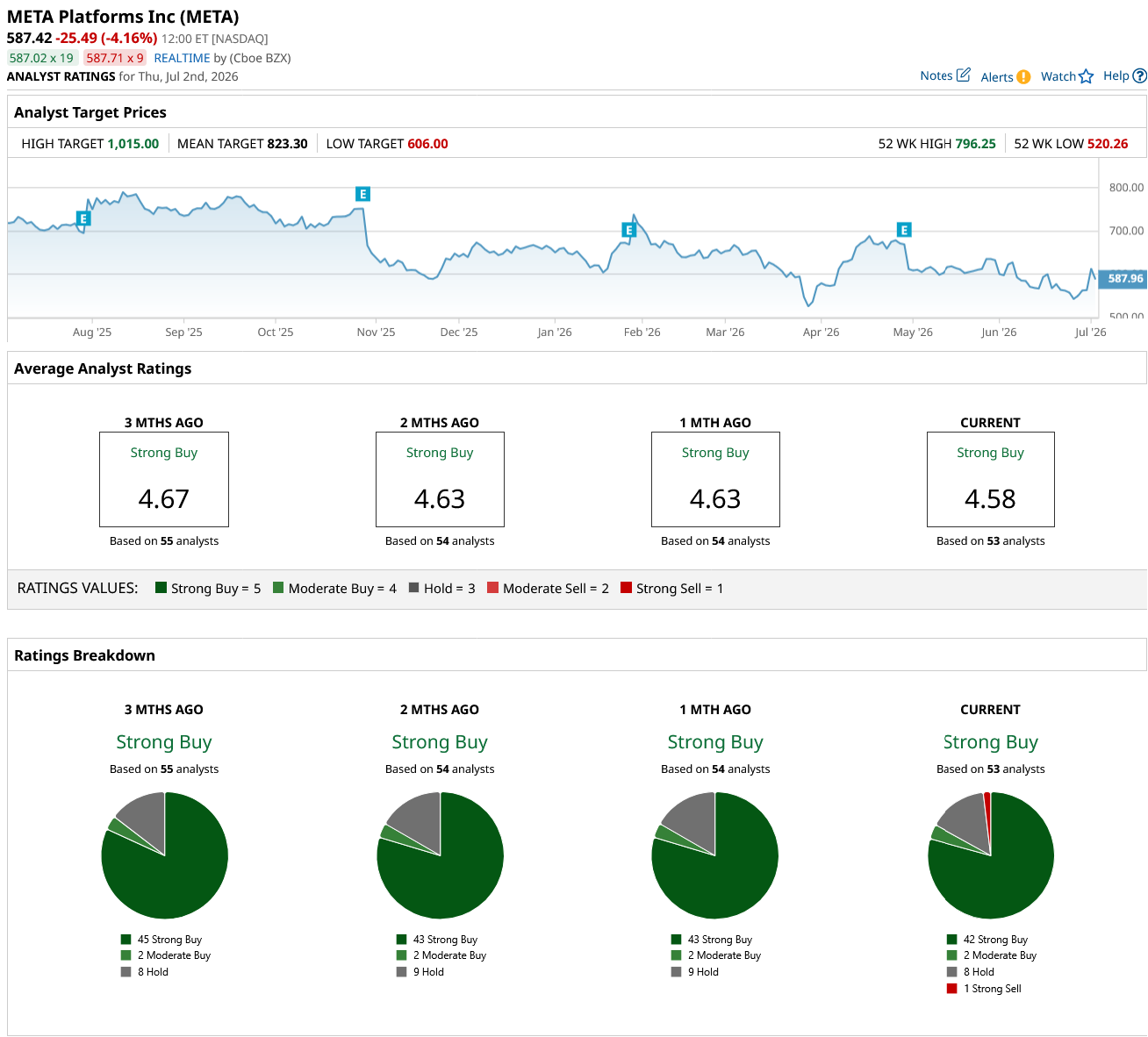

Out of the 53 analysts covering META stock, 42 recommend “Strong Buy,” two recommend “Moderate Buy,” eight recommend “Hold,” and one recommends “Strong Sell.” The average META price target is $823.30, above the current price of about $587.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)