Netflix (NFLX) has never been a company to sit still. It has evolved into the world’s leading streaming platform, constantly reinventing itself with original content, live sports, gaming, and a fast-growing advertising business. But even the biggest names can hit a rough patch.

Despite delivering impressive numbers in the first quarter of 2026, the streaming giant has struggled to win over investors this year. A softer full-year outlook, lingering questions about the company’s next growth engine, and the departure of co-founder Reed Hastings have left many wondering where the streaming giant goes from here. Those concerns have kept the stock in the red, even as Wall Street remains broadly optimistic about its long-term prospects.

That’s why July 16 is a date investors would not want to miss. Netflix is scheduled to report its second-quarter earnings results, giving investors a fresh look at the direction in which the company is headed. A strong quarterly report, coupled with upbeat guidance, could be the spark investors have been waiting for, restoring confidence and helping Netflix turn the page after a challenging first half of the year.

With Wall Street remaining broadly bullish ahead of the earnings release, let's take a closer look at Netflix stock.

About Netflix Stock

Netflix has come a long way since its days as a DVD-by-mail rental service. Headquartered in California and now valued at $326.97 billion, it has grown into the world's leading streaming platform by constantly reinventing itself. From artificial intelligence (AI)-powered content recommendations to launching an ad-supported tier in 2022 and cracking down on password sharing in 2023, Netflix has kept evolving with consumer habits.

Also, the company has expanded into live programming, including NFL games and comedy specials. Today, Netflix serves more than 325 million paid subscribers across over 190 countries, offering movies, series, documentaries, games, and award-winning original content.

Netflix’s shares have gone from stealing the spotlight to facing a reality check. The streaming giant has been under pressure in recent weeks after reportedly losing the bidding war for Roku (ROKU) to Fox (FOX), not long after missing out on Warner Bros. Discovery (WBD), which ultimately went to David Ellison’s Paramount (PSKY). Those back-to-back deal disappointments have fueled concerns that Netflix may be losing ground on strategic opportunities just as competition across the media landscape heats up.

However, the market’s frustration runs deeper than missed acquisitions. Investors were hoping Netflix would raise its full-year 2026 revenue outlook after a blockbuster first quarter, but management chose to stand pat. Its operating margin guidance also fell short of analysts’ expectations, raising concerns that the one-time breakup fee from the Warner Bros. deal may be masking rising content amortization costs. Adding another layer of uncertainty is the news of longtime chairman Reed Hastings officially stepping down, marking the end of an era as Netflix works to prove its advertising business can become a meaningful growth engine.

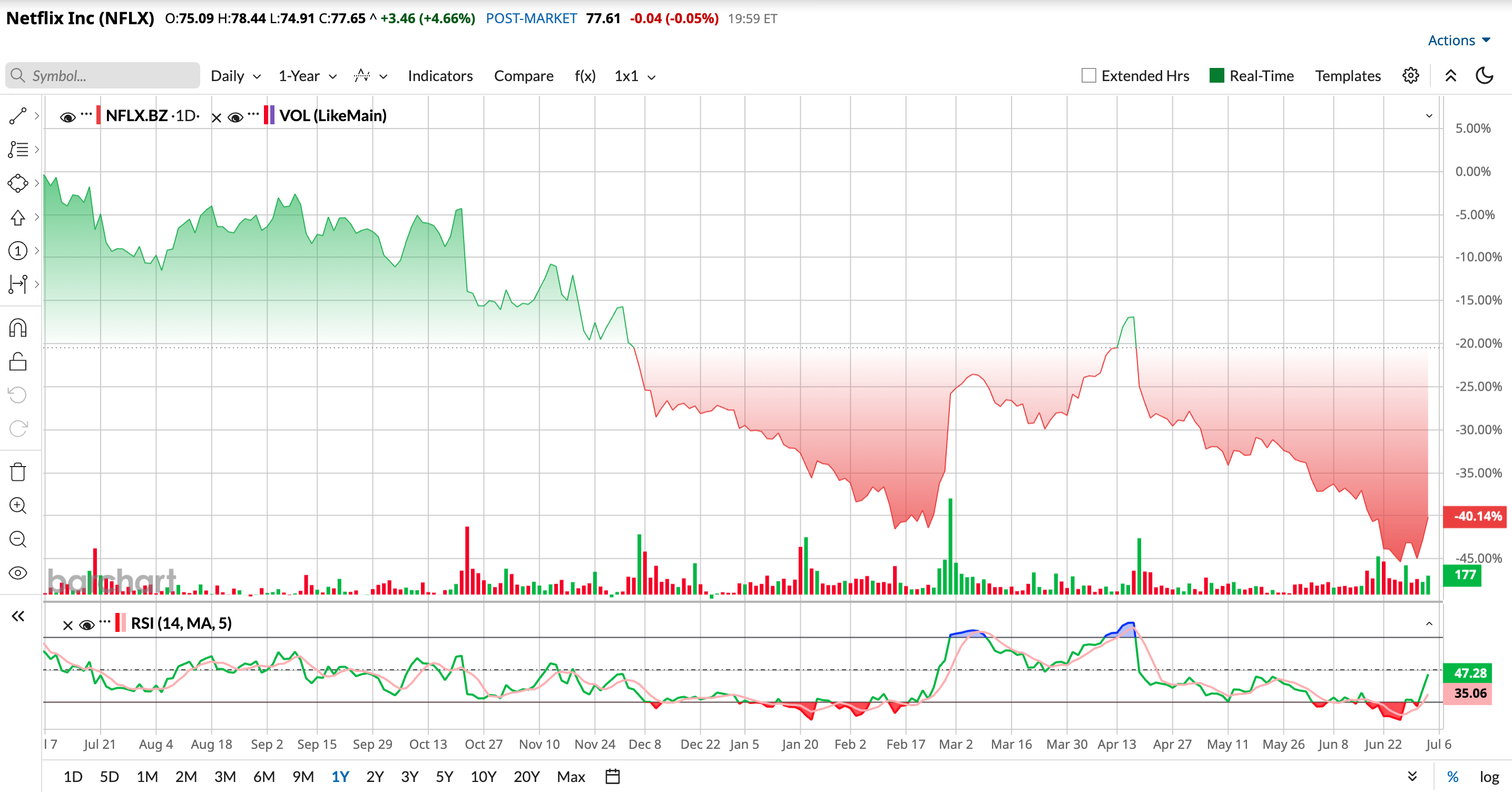

Unsurprisingly, the stock has struggled to find its footing. Over the past 52 weeks, Netflix shares have tumbled 39.6%, retreating from its 52-week high of $134.12 to trade a little above $70. The weakness has accelerated in recent months, with the stock falling 21.3% over the past three months and another 6.8% in the last month alone.

The technical picture also reflects the cooling sentiment. After flashing overbought conditions with a 14-day RSI above 70 in April, the indicator has now slipped to 47.28, suggesting momentum has swung sharply in the opposite direction. For now, investors appear content to stay on the sidelines, waiting for Netflix to offer a clearer picture of where the business is headed. The company now has to prove that its next chapter can be every bit as compelling as the one that made it a streaming giant.

NFLX stock does not come cheap. The stock trades at 21.65 times forward non-GAAP earnings and 6.36 times forward sales, both above sector averages. Still, investors are paying for its long-term growth story. With advertising, live content, gaming, and AI driving expansion, today’s premium looks more reasonable, especially since both multiples remain below historical averages.

A Snapshot of Netflix’s Q1 Numbers

When the streaming giant reported its first-quarter results on April 16, it delivered numbers that comfortably topped Wall Street’s expectations. Revenue climbed 16.2% year-over-year (YOY) to $12.25 billion, while EPS nearly doubled to $1.23 from $0.66 a year earlier. A major contributor to the strong profit growth was higher operating income, helped in part by a one-time $2.8 billion termination fee tied to its agreement with Warner Bros. Discovery.

The company’s advertising business was also impressive. More than 60% of new subscribers in ad-supported markets opted for Netflix’s lower-priced ad tier, while its advertiser base jumped 70% YOY to over 4,000 clients. With that momentum, management now expects its advertising business to generate nearly $3 billion in revenue this year.

Plus, cash generation was solid. Operating cash flow almost doubled to $5.3 billion from $2.8 billion a year ago, driving non-GAAP free cash flow to $5.1 billion. Meanwhile, Netflix is leaning further into AI to improve the user experience. During the quarter, it acquired InterPositive to give creators access to more generative AI tools, while also revamping its mobile app with a new vertical video feature slated to roll out by month-end.

Yet, despite all those wins, investors were not entirely convinced. Netflix’s shares slid 9.72% after the earnings release as Wall Street looked beyond the headline numbers and focused on next steps.

Management estimates full-year 2026 revenue between $50.7 billion and $51.7 billion, implying annual growth of 12% to 14%, supported by steady subscriber additions, selective price increases, and an ad business expected to nearly double in size. They also reaffirmed their full-year operating margin target of roughly 31.5%.

Still, the road ahead is not expected to be perfectly smooth. Netflix is gearing up to release its Q2 report on Thursday, July 16. For Q2, management forecasts revenue of $12.57 billion, representing around 13% YOY growth, while warning that content spending will remain front-loaded. The company expects Q2 to see the year’s biggest jump in content amortization, pushing operating margin down to about 32.6% from 34.1% a year ago before improving later in 2026. Adding another storyline to watch, co-founder Reed Hastings stepped down as chairman in June, leaving investors to keep a close eye on the company's next chapter.

Meanwhile, analysts tracking the company expect Q2 revenue to be around $12.6 billion, while EPS is projected to be $0.79, representing a growth of about 9.7% YOY. Looking ahead, EPS is forecasted to grow by 42.3% YOY to $3.60 in fiscal 2026, with the bottom line for fiscal 2027 projected to reach $3.85 per share, up nearly 7% annually. Overall, the outlook reflects steady growth, but short-term margin and sentiment pressures are shaping investor focus.

What Do Analysts Expect for Netflix Stock?

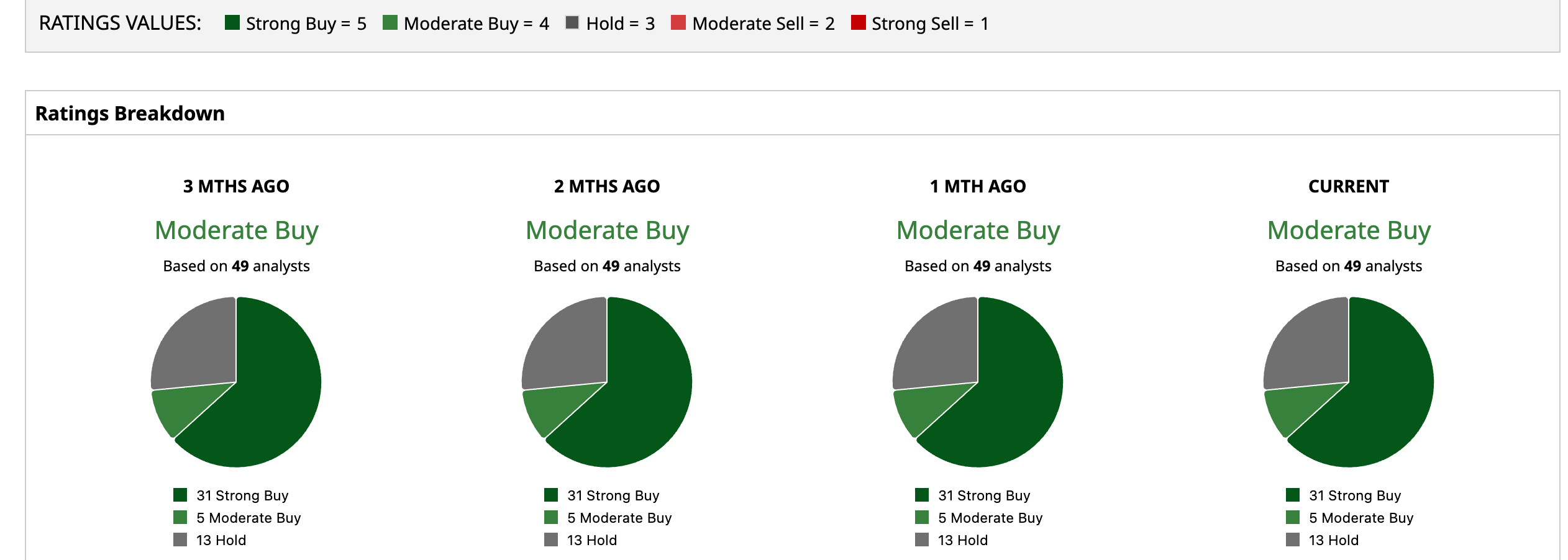

Overall, Wall Street is moderately bullish on NFLX, giving a consensus “Moderate Buy” rating. Of the 49 analysts rating the stock, a majority of 31 analysts have recommended a “Strong Buy,” five suggest a “Moderate Buy,” and the remaining 13 analysts have a “Hold” rating.

Meanwhile, the stock has a mean price target of $113.55, which suggests rebound potential of 46.2% from current price levels. Meanwhile, the Street-high target of $135 implies the streaming giant’s stock could rise as much as 73.9%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)