Chip manufacturing giant Taiwan Semiconductor Manufacturing Company Limited (TSM), or TSMC, is set to report its second-quarter results on July 16 before the market opens. The company has become vital for major technology companies, as AI buildouts take center stage.

Ahead of the results, the company has reportedly asked its customers to prepare for price increases. According to a report by Culpium, this is expected to affect the majority of its wafer revenue (nearly three-quarters). The exact magnitude of the price increases is not known. However, this could fall within the 5%-10% range.

Earlier, it was reported that only the 3nm process would face this. However, the hikes could extend beyond 3nm and 2nm to include older but still advanced processes such as 5nm and 7nm. The inclusion of 7nm is notable because it is heavily used across processors, accelerators, networking silicon, and other high-performance chips. The timing of the increases is also notable, as it shows the immense negotiating leverage it enjoys amid high demand for its chips among AI accelerator vendors.

This also culminates at a time when TSMC has become central in a tech competition between the U.S. and China.

About Taiwan Semiconductor Stock

Taiwan Semiconductor is a leading chip foundry that makes semiconductors for customers across the technology industry. It focuses on advanced manufacturing, producing chips that power smartphones, data centers, and other electronics, while also investing heavily in process technology and global production capacity. The company is headquartered in Hsinchu, Taiwan and has a gigantic market capitalization of $2.25 trillion.

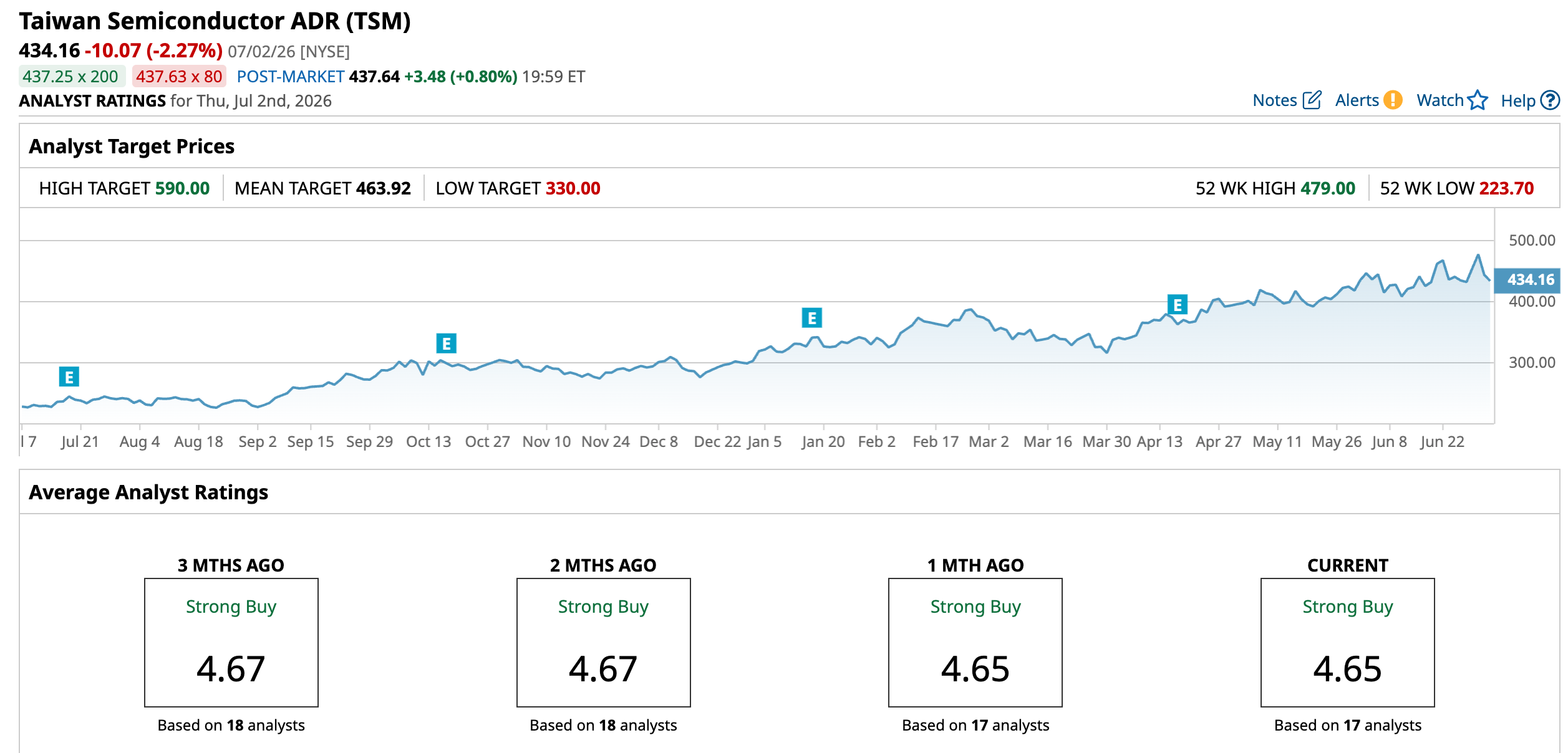

Over the past year, TSMC’s stock has gained 85.86%, while it is up 42.87% year-to-date (YTD). TSMC’s stock has risen over the past year because investors have continued to price in strong demand for advanced chips, especially from AI and high-performance computing customers. The broader semiconductor cycle has also helped, as TSMC sits at the center of the AI supply chain and benefits when major chip designers need leading-edge production. The stock had reached a 52-week high of $479 on June 30.

Despite the rise, TSMC’s stock is trading at a relatively cheap valuation. On a forward-adjusted basis, its price-to-earnings ratio of 28.94 times is lower than the industry average of 33.21 times.

Taiwan Semiconductor’s Q1 Results

Supported by a strong demand for our leading-edge process technologies, TSMC reported strong results in the first quarter. The company’s revenue increased by 35.1% year-over-year (YOY) to NT$1.13 trillion ($35.60 billion). Its income from operations grew by 61.9% YOY to NT$658.97 billion ($20.68 billion). TSMC’s EPS grew 58.3% from the year-ago period to NT$22.08.

For the second quarter, TSMC expects revenue between $39 billion and $40.20 billion, with a gross margin of 65.5% - 67.5%. Wall Street analysts are optimistic about TSMC’s future earnings. They expect the company’s EPS to climb by 52.63% YOY to $3.77 for the second quarter. For fiscal 2026, EPS is projected to surge 44.1% to $15.35, followed by a 27% growth to $19.50 in fiscal 2027.

What Analysts Think About Taiwan Semiconductor’s Stock

Analysts at Barclays maintained TSMC’s rating at “Overweight” while raising the price target from $470 to $625. Analyst Simon Coles believes that the market is actively seeking advanced logic wafer supply, which supports the view of continued strong growth at the company. Moreover, the strong demand for advanced logic wafer supply following a recent Asia supply chain trip was also cited.

In April, analysts at DA Davidson maintained a “Buy” rating and a $450 price target, which reflects confidence in the company’s position and performance as the leading chip manufacturer. Needham raised its price target on TSMC from $410 to $480, while maintaining a “Buy” rating, citing the company’s first-quarter results. Analysts also said AI demand remains strong, and premium smartphone sales are expected to hold up despite pressure on memory prices. Taiwan Semi is managing customer demand alongside heavy capital spending amid a severe chip supply shortage.

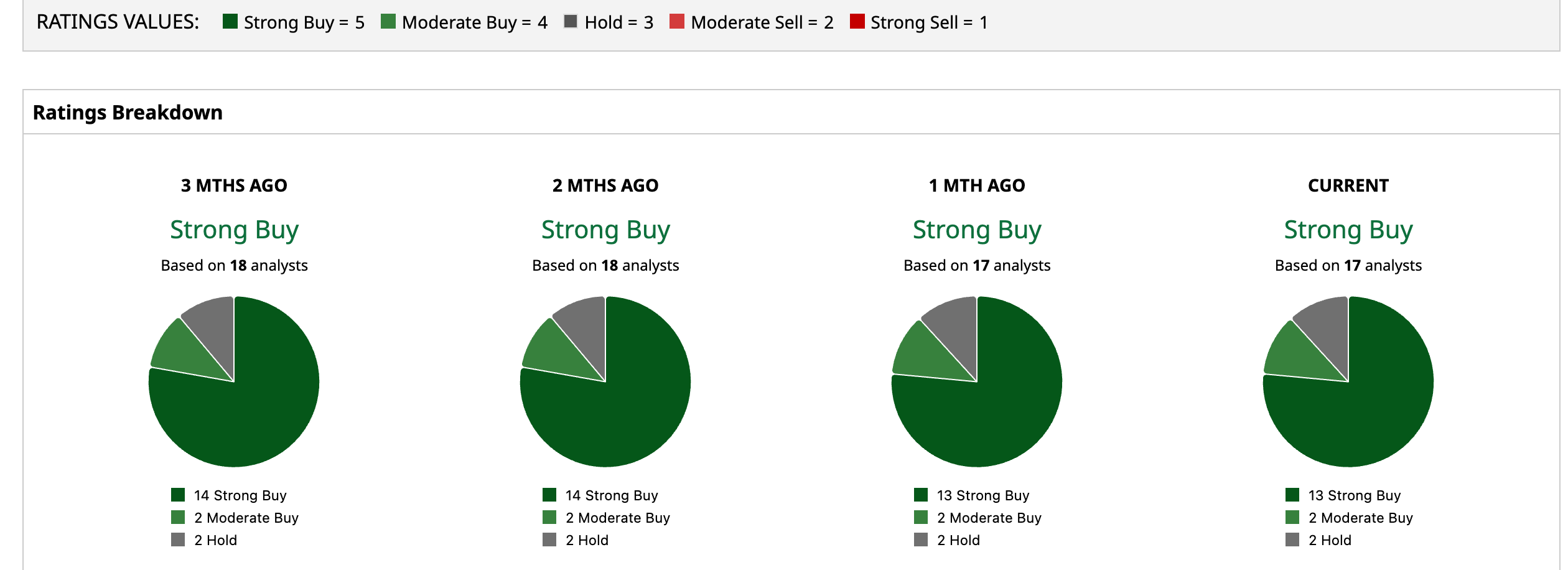

Taiwan Semiconductor has been in the spotlight on Wall Street, with analysts awarding it a consensus “Strong Buy” rating. Of the 17 analysts rating the stock, a majority of 13 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while two analysts are playing it safe with a “Hold” rating. The consensus price target of $463.92 represents a 6.86% upside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)