/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)

UnitedHealth Group (UNH) has long been one of the biggest names in the health insurance and managed care sector, wearing many hats through its insurance operations and fast-growing healthcare services arm. For years, it was the kind of stock investors could simply buy and let time do the heavy lifting. Then the tide turned. The past couple of years threw more than a few curveballs, with a sharp rise in Medicare Advantage costs and mounting pressure dragging the shares lower. Although the stock has staged an encouraging comeback in 2026, many investors are still waiting to see if this turnaround has real legs.

That’s why July 16 deserves a big circle on the calendar. UnitedHealth is set to report its second-quarter earnings before the market opens, and Wall Street will be watching closely for signs that the recovery is staying on track.

The company heads into the release with the wind at its back. In the first quarter, it topped Wall Street’s expectations, improved its medical care ratio to 83.9%, raised its full-year earnings guidance, and expressed confidence that its efforts to simplify operations and strengthen execution are beginning to pay off.

With optimism building ahead of the earnings release, let’s take a closer look at whether UNH stock still has room to run.

About UnitedHealth Stock

Founded in 1974 and headquartered in Minnesota, UnitedHealth Group is one of the world's largest healthcare companies, with a market capitalization of $386.3 billion. It operates through two complementary businesses: UnitedHealthcare, which provides health insurance coverage to millions, and Optum, which delivers technology-enabled care, pharmacy services, data analytics, and healthcare solutions. Together, they create an integrated healthcare ecosystem that blends insurance with care delivery, helping improve patient outcomes while driving long-term growth across an increasingly digital healthcare landscape.

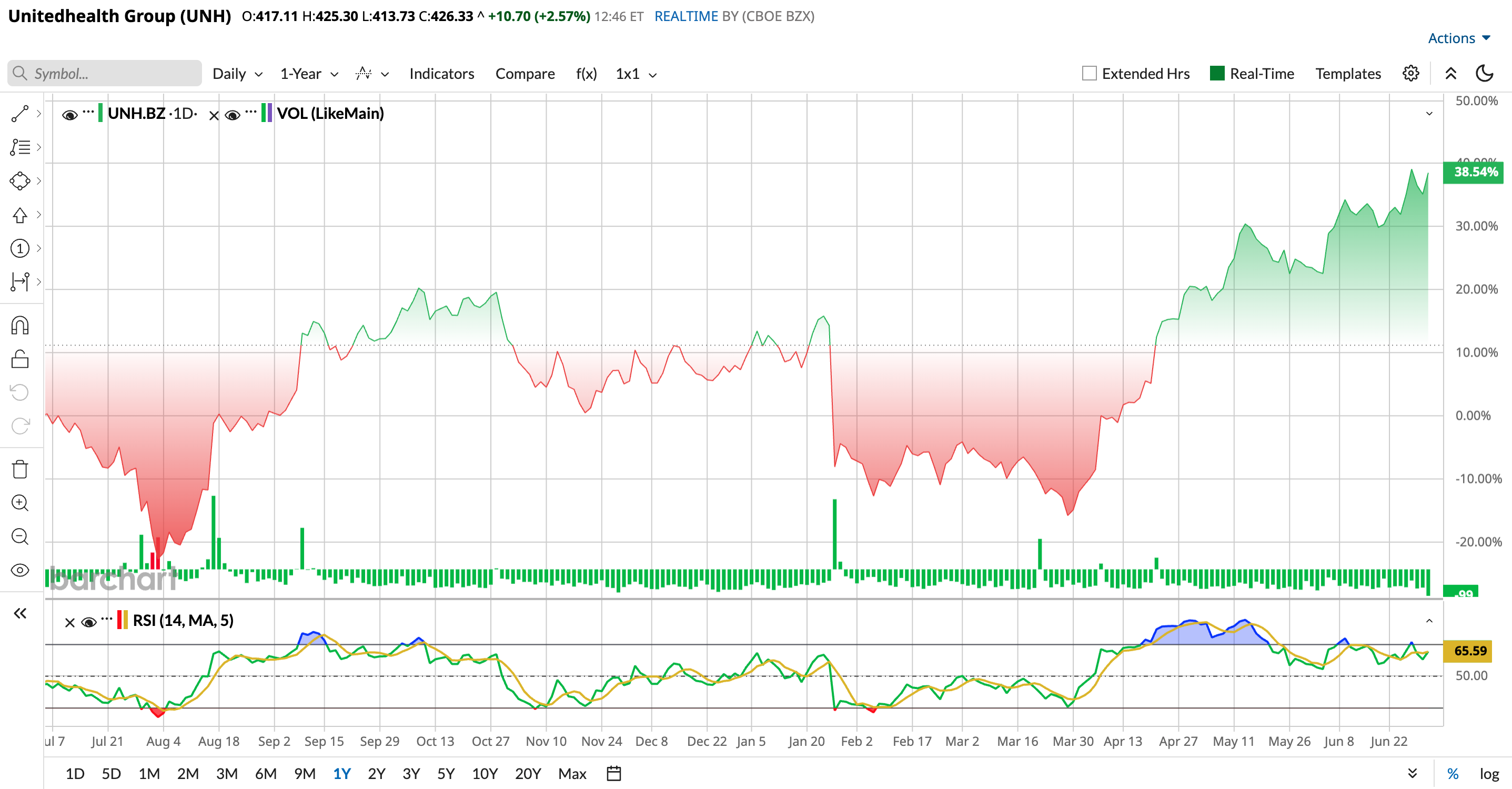

UNH stock has weathered more than its fair share of storms over the past year. After a bruising 2025, the shares tumbled to a five-year low of $234.60 in August 2025 as investor sentiment took a beating and sellers stayed firmly in the driver’s seat. But every storm eventually runs out of rain. Since hitting that bottom, the stock has bounced back nearly 81.6%, steadily rebuilding lost ground.

That recovery has helped push UNH up 38.3% over the past 52 weeks, with an impressive 28.9% gain already in 2026. The momentum has gathered pace recently, as the stock climbed 53.4% in the past three months and another 12.6% over the last month.

Technically, the picture also looks healthier. The 14-day RSI has settled at 64.87 after cooling from overbought levels in mid-May, while relatively muted trading volumes suggest investors are quietly accumulating shares rather than chasing the rally – a classic case of slow and steady winning the race!

Valuation-wise, UNH is not exactly screaming “bargain.” The stock trades at 22.60 times forward non-GAAP price-to-earnings, a premium to both its sector peers and its historical average. If earnings continue to gather steam, today’s multiple could look a lot less demanding over time. Meanwhile, its price-to-sales ratio of 0.85 times remains comfortably below both the sector median and its own five-year average, suggesting the stock is not expensive from every angle.

And if there was any doubt about management’s confidence, its dividend policy tells a different story. Even after the stock’s rough patch earlier this year, UnitedHealth continues to reward shareholders. Earlier this month, the company raised its quarterly dividend by 5%, raising the payout from $2.21 to $2.32 per share. That marks its 16th consecutive year of dividend increases and extends its uninterrupted dividend-paying streak to 24 years. It also brings the annualized payout to $9.28 per share, offering a forward yield of about 2.21%, well above the SPDR S&P 500 ETF's (SPY) 1.01% yield.

A Closer Look at UnitedHealth’s Q1 Results

When UnitedHealth Group reported its first-quarter results on April 21, it gave investors a reason to breathe a little easier. The healthcare giant delivered a solid performance, with revenue climbing 2% year-over-year (YOY) to $111.7 billion, comfortably topping Wall Street’s expectations. Adjusted earnings came in at $7.23 per share, edging higher from a year ago and reinforcing the view that the company is gradually getting back on its feet.

The quarter was not flawless, but the good outweighed the bad. Growth in commercial fee-based memberships and another strong showing from Optum Rx helped power results, even as weakness at Optum Health and a decline in risk-based memberships acted as a drag. On the insurance side, premium revenue rose to $87.6 billion from $86.5 billion a year earlier.

Perhaps the biggest bright spot was medical cost management. UnitedHealth’s adjusted medical care ratio improved to 83.9%, down 90 basis points from last year, signaling that healthcare costs were becoming more manageable. While medical costs inched up to $73.5 billion, favorable reserve development and tighter cost controls helped keep profitability on track.

The balance sheet also moved in the right direction. Cash and short-term investments increased to $31.2 billion, while long-term debt edged lower to $71.4 billion. Meanwhile, operating cash flow surged to $8.9 billion from $5.5 billion a year earlier, giving the company enough financial muscle to return $2 billion to shareholders through dividends during the quarter.

Looking ahead, management struck an optimistic tone despite earlier expecting 2026 revenue to top $439 billion, which would be slightly below 2025 levels due to planned operational right-sizing. The company raised its adjusted EPS outlook to more than $18.25, reflecting improving margins, while earlier projecting net margins of roughly 3.6%, $2.5 billion in share repurchases, $8 billion in dividends, and $3.8 billion in capital expenditure.

Even with medical membership expected to decline across several key segments, management believes stronger execution and disciplined cost control will keep the company moving in the right direction.

UnitedHealth is all set to unveil its Q2 earnings report on Thursday, July 16, before the market opens. Analysts predict revenue for the quarter to be around $111 billion and EPS to rise by 18.6% YOY to $4.84. EPS for fiscal 2026 is anticipated to be $18.32, representing an annual growth of 12.1%, and then surge by another 13.5% YOY to $20.80 in fiscal 2027.

What Do Analysts Expect for UnitedHealth Stock?

Wall Street is growing more upbeat on UnitedHealth ahead of its July 16 earnings report. Morgan Stanley recently lifted UNH’s price target to $468 from $453 while reiterating its “Overweight” rating. The bank believes UnitedHealth is well-positioned to kick off the managed care earnings season on a strong note, backed by healthier healthcare utilization trends and improving execution at Optum Health.

It also expects the company to deliver second-quarter earnings per share above the market’s estimates. In fact, Morgan Stanley has named UnitedHealth one of its top picks, suggesting a solid report could set the stage for the rest of the managed care industry.

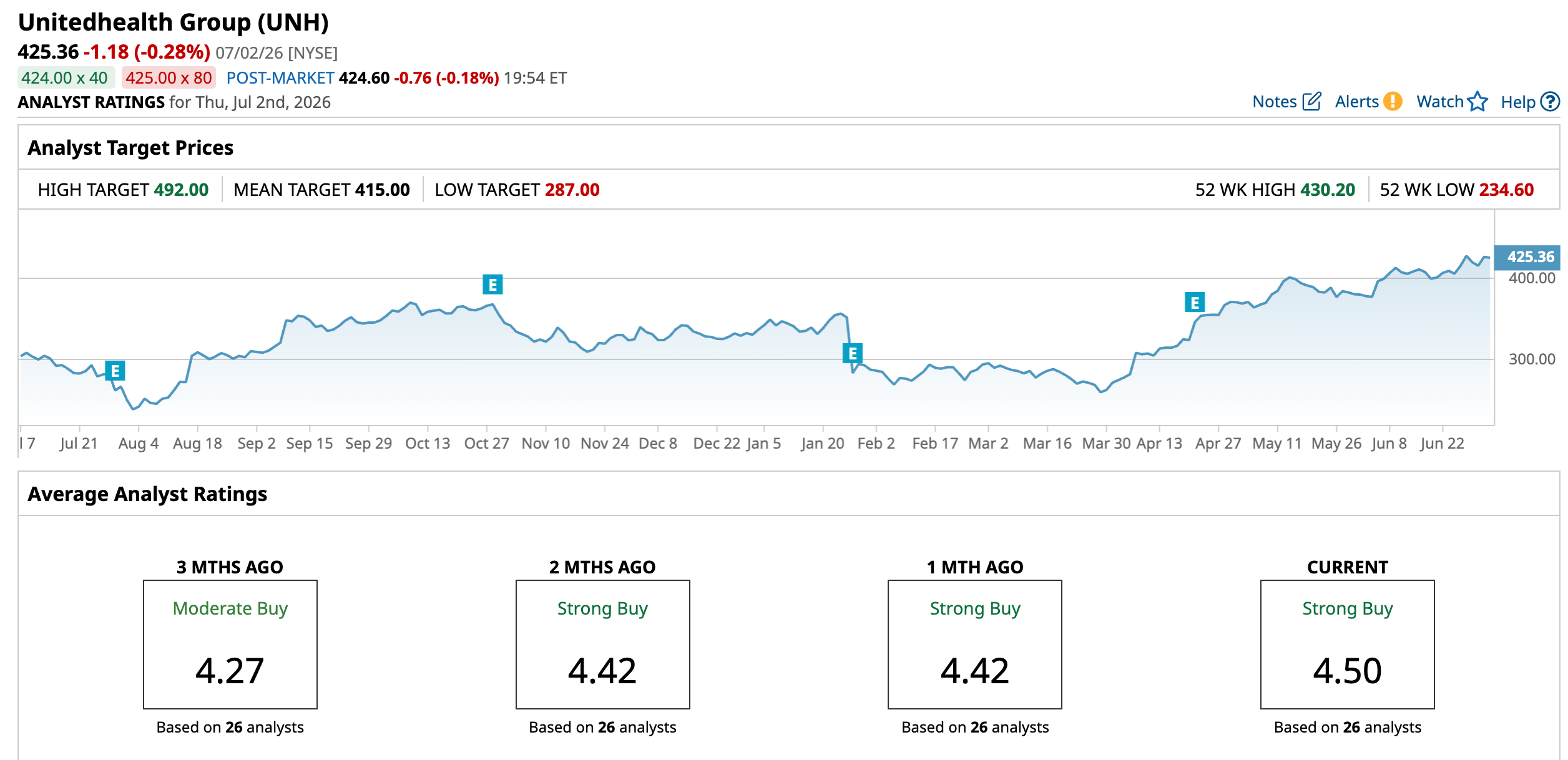

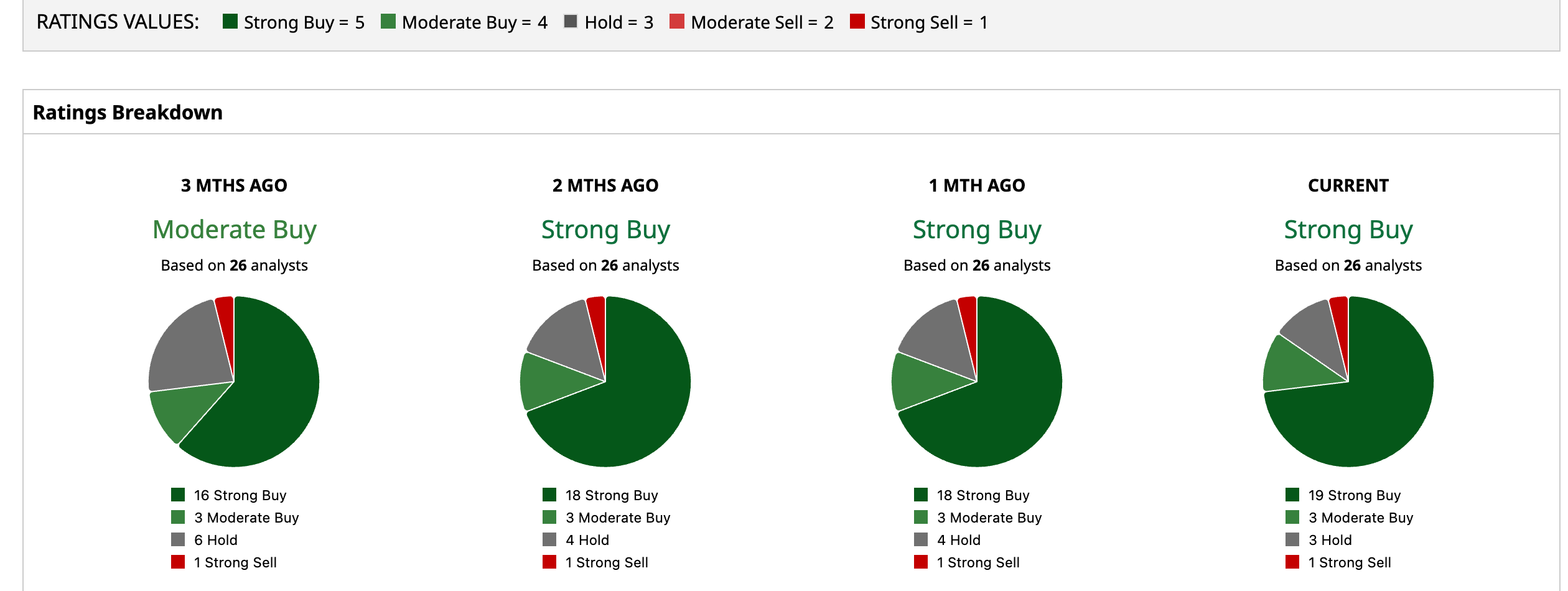

Analysts have clearly grown more confident over the past few months. UNH had a “Moderate Buy” rating three months ago, but it has now been upgraded to a “Strong Buy” rating overall. In fact, 19 of the 26 analysts covering UNH stock currently rate the stock a “Strong Buy.” Three analysts suggest a “Moderate Buy,” three are playing it safe with a “Hold,” and the remaining one analyst has a “Strong Sell” rating.

While the stock has edged past the mean price target of $415, the Street-high target of $492 signals that UNH has upside potential of 15.7% from the last closing price.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)