Fairfield, Ohio-based Cincinnati Financial Corporation (CINF) provides property casualty insurance products. Valued at over $28.9 billion by market cap, the company markets a variety of insurance products and provides leasing and financing services. The insurance giant is expected to announce its fiscal second-quarter earnings for 2026 soon.

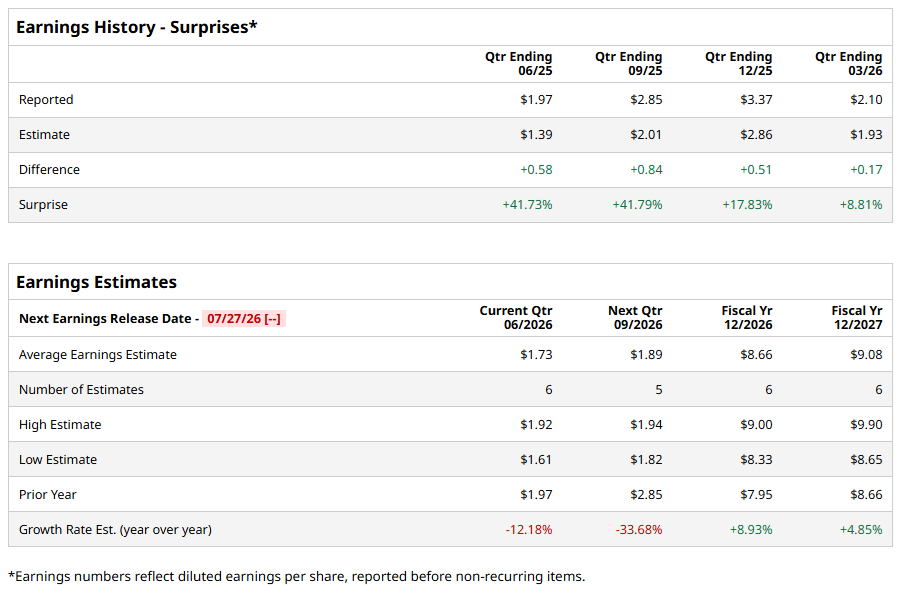

Ahead of the event, analysts expect Cincinnati Financial to report a profit of $1.73 per share on a diluted basis, down 12.2% from an EPS of $1.97 in the year-ago quarter. However, the company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect the company to report EPS of $8.66, up 8.9% from $7.95 in fiscal 2025. Its EPS is expected to rise 4.9% YOY to $9.08 in fiscal 2027.

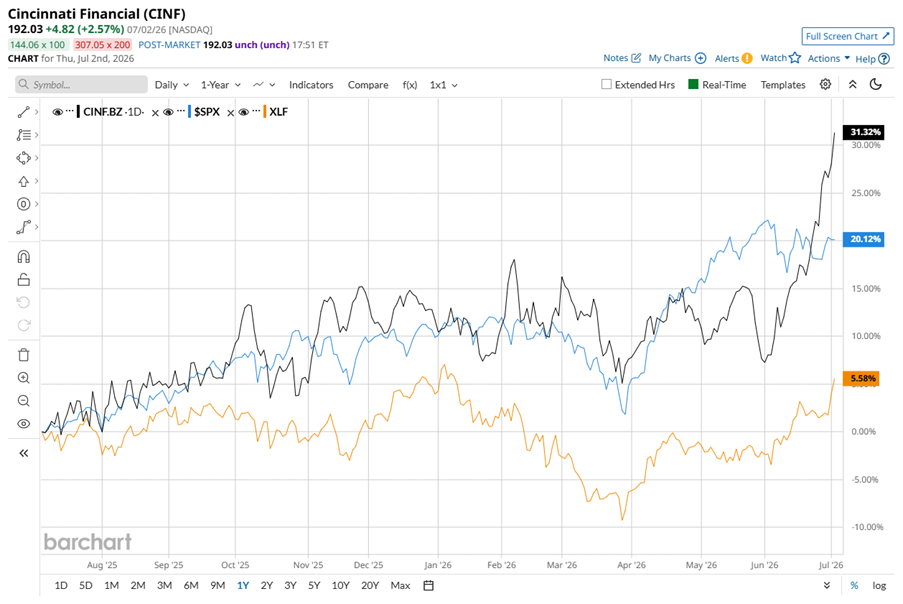

CINF stock has outperformed the S&P 500 Index’s ($SPX) 20.2% gains over the past 52 weeks, with shares up 31.4% during this period. It also outperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 5.7% gains over the same time frame.

CINF’s rally has not been driven by flashy headlines. Instead, investors have been rewarding the insurer for doing what it has done for decades – delivering steady results and consistently returning cash to shareholders. Crowned as a “Dividend King,” the company recently extended its remarkable 65-year streak of annual dividend increases, declaring a $0.94-per-share quarterly dividend in May, payable in July. That works out to an annual dividend yield of about 2%, while its conservative 34.5% payout ratio leaves plenty of room to keep those increases coming.

The company’s mixed Q1 2026 earnings report in April also helped keep the momentum alive. While revenue of $2.9 billion came in below Wall Street’s expectations, adjusted earnings of $2.10 per share topped analyst estimates, giving investors confidence that the business remains on solid footing. That combination of dependable dividends, resilient earnings, and long-term financial discipline helped lift CINF stock to a fresh record high of $192.09 on July 2, allowing it to comfortably outperform the broader market this year.

Analysts’ consensus opinion on CINF stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 10 analysts covering the stock, three advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and six give a “Hold.” CINF currently trades above its average analyst price target of $181.28 and also its most bullish call of $191.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)