Dell Technologies DELL is scheduled to report its fourth-quarter fiscal 2025 results on Feb. 27.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Dell expects fourth-quarter revenues in the range of $24-$25 billion, with a midpoint of $24.5 billion, indicating 10% growth. Earnings are expected to be $2.50 per share (+/- 10 cents).

The Zacks Consensus Estimate for revenues is pegged at $24.66 billion, suggesting 10.48% growth from the figure reported in the year-ago quarter.

The consensus mark for quarterly earnings is pegged at $2.53 per share, up a couple of cents over the past 30 days, and suggesting year-over-year growth of 15%.

Dell Technologies Inc. Price and EPS Surprise

Dell Technologies Inc. price-eps-surprise | Dell Technologies Inc. Quote

Dell’s earnings beat the Zacks Consensus Estimate in all of the trailing four quarter, with an earnings surprise of 10.44% on average.

Let’s see how things have shaped up for DELL shares prior to this announcement.

Key Factors to Note for DELL

Sluggish PC shipments in the consumer segment are expected to have hurt DELL’s top-line growth in the fourth quarter of fiscal 2025 amid continued consumer demand challenges and competitive pressures. Weak IT spending over storage is expected to have negatively impacted top-line growth.

Per Gartner’s latest report, DELL saw a 0.1% year-over-year decline in worldwide PC shipments in the fourth quarter of 2024. Dell Technologies’ market share declined 20 basis points (bps) to 15.5%. According to IDC’s data, DELL lost 20 bps market share to 14.4% while shipments remained at 9.9 million units.

Although Dell’s fiscal fourth-quarter results are expected to have benefited from the robust demand for AI-optimized servers, guidance implied a sequential decline.

Dell anticipates 13% year-over-year revenue growth at the midpoint for the combined Infrastructure Solutions Group (ISG) and Client Solutions Group (CSG). ISG revenues are expected to increase in the mid-twenties, while CSG revenues are expected to be up low single digits year over year.

In the fiscal third quarter, ISG revenues jumped 33.8% year over year to $11.37 billion. DELL’s current guidance implies slow growth from AI-related sales in the to-be-reported quarter.

The Zacks Consensus Estimate for DELL’s fourth-quarter fiscal 2025 ISG revenues is currently pegged at $11.713 billion, indicating 25.5% year-over-year growth. The consensus mark for CSG is pegged at $12.074 billion, suggesting 3.1% year-over-year growth.

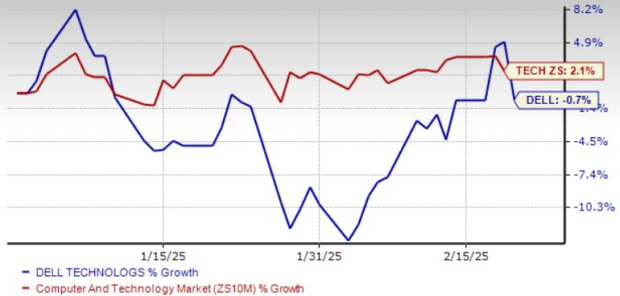

DELL Shares Underperform Sector

Year to date, Dell’s shares have declined 0.7%, underperforming the broader Zacks Computer & Technology sector’s return of 2.1%.

Year-to-Date Performance Chart

DELL stock is overvalued, as the Value Score of C suggests.

Can Strong AI Demand Push the DELL Stock Higher?

Strong demand for AI servers, driven by ongoing digital transformation and heightened interest in generative AI (GenAI) applications, is a key catalyst. In the third quarter of fiscal 2025, Dell Technologies shipped $2.9 billion of AI servers, and the AI server backlog was $4.5 billion, exiting the reported quarter.

AI server pipeline is expanding across Tier-2 CSPs and enterprise customers. Dell expects strong top-line growth for the second half of fiscal 2025, driven by robust AI demand.

The Dell AI Factory, which combines Dell Technologies’ solutions and services optimized for AI workloads and supports an open ecosystem of partners comprising NVIDIA NVDA, Meta Platforms META, Microsoft MSFT and Hugging Face, has been a game changer.

DELL’s end-to-end solutions portfolio supports long-term growth targets. It expects revenues to grow between 3% and 4% and earnings of more than 8%.

Dell expects to return more than 80% of adjusted free cash flow to shareholders and a dividend growth rate of more than 10% during the 2024-2028 timeframe. Since the VMware spin-off, Dell has returned $5.5 billion to shareholders.

What Should Investors Do With DELL Stock?

Dell’s robust portfolio and rich partner base are noteworthy. However, challenges in the PC market are a headwind in the near term. DELL’s fiscal fourth-quarter guidance implies lower AI-related sales. This, along with growing risks related to tariffs, is a concern for investors. A stretched valuation is a headwind.

Technically, DELL shares are trading below the 200-day moving average, indicating a bearish trend.

DELL Shares Trade Below 200-Day SMA

Image Source: Zacks Investment Research

DELL currently has a Zacks Rank #5 (Strong Sell), suggesting that it may be wise to avoid the stock ahead of fourth-quarter fiscal 2025 results.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Dell Technologies Inc. (DELL): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Meta Platforms, Inc. (META): Free Stock Analysis Report

/Technology%20abstract%20by%20TU%20IS%20via%20iStock.jpg)