/EV%20in%20showroom%202%20by%20Robert%20Way%20via%20%20Shutterstock.jpg)

While the market's excitement around the launch of the American Depository Receipt, or ADR, for memory chip major SK Hynix is palpable, developments around another ADR already trading certainly deserve attention. Chinese EV maker, XPeng (XPEV), revealed that it will be expanding its popular MONA sub-brand with its first SUV: the MONA L03. To be released in China today, its global launch will be later this month.

Shares of XPeng ended 3% higher on the news, coming as a welcome break after a tough 2026 so far.

About XPeng

Founded just about a decade ago in 2014, XPeng is one of China's leading smart EV manufacturers. Unlike many traditional automakers, XPeng positions itself as an AI mobility technology company, emphasizing autonomous driving software, in-house AI chips, intelligent cockpits, robotics, and even flying cars. With major offices in Beijing, Shanghai, Shenzhen, Silicon Valley, Munich, and San Diego, XPeng has steadily expanded its global footprint and now sells vehicles across Europe, Southeast Asia, Australia, the Middle East, and Latin America.

Valued at a market cap of about $12.9 billion, XPEV stock is down 35% on a year-to-date (YTD) basis.

So, can the new MONA LO3 be the catalyst for a rebound for XPEV stock? Pertinently, what's the scenario looking like for investors looking to be in it for the long haul? Let's find out.

Q1 Results Disappoint, No Cause For Alarm (Yet)

A key reason why shares of XPeng are down 40% from its IPO in August 2020 is its unprofitable nature. The company has yet to report profits, and that has not sat well with most investors. However, amid all that the company is doing (more on that later), its finances have still not gotten out of hand.

In Q1 2026, XPeng's headline figures of revenue and earnings disappointed. Revenues of RMB 13.03 billion were down 17.6% from the previous year. Seasonality, lower vehicle deliveries, and product transition were cited as the reasons. However, the management's aim of delivering four new models this year will result in a “robust sales growth trajectory.”

Losses widened to RMB 1.87 per share from RMB 0.70 per share, making this the eighth quarter out of the past nine where the company has reported losses. Although this was the only one where losses widened.

For Q2 2026, XPeng expects revenues to be between RMB 19.60 and RMB 20.80 billion, with deliveries of vehicles projected to be between 100,000 and 106,000, denoting year growth ranges of 7.25% to 13.82% and -3.08% to +2.73%, respectively.

Deliveries for the quarter stood at 62,682, a drop of 33.3% on a year-over-year (YoY) basis. This was in the middle of the analyst estimates of deliveries of 61,000 to 66,000 vehicles. However, as a silver lining, gross profits rose to RMB 2.7 billion from RMB 2.5 billion in the year-ago period. Consequently, gross margins extended to 20.6% from 15.6% in the year-ago period.

In terms of valuation, the XPEV ADR is trading at reasonable levels. While forward EV/S and P/S of 1.15 and 0.91 are below the sector medians, the forward P/CF of 13.08 is in the range of the sector median of 10.27.

(Can) Fire on All Cylinders

Setting aside the near-term seasonality concerns and zooming out, one will find XPeng dabbling on multiple fronts: from flying cars to chips to humanoid robots.

Having said that, let's first dive into its core business of EVs. Q1 2026 may have been slow, but the company has expectedly bounced back in Q2 2026. Having delivered 103,295 units, XPeng's growth on a YoY basis was 16%. This was impressive as the wider EV market in China declined by 14% in the first five months of 2025, and the global market grew at a low to mid single-digit rate in the same period.

However, the company still holds just a 3% market share in the Chinese passenger EV market, much behind the market leader BYD (BYDDY).

Notably, to close the gap, XPeng has introduced two recent models targeted at distinct customer groups. The MONA LO3 represents a compact coupe-style sport utility vehicle and serves as the second offering in the MONA lineup after the successful M03 liftback. Positioned toward younger, technology-oriented consumers, it carries an expected starting price of around RMB 150,000, placing it in one of the fastest-growing segments of the Chinese new energy vehicle (NEV) market. The vehicle boasts an aerodynamic design with a 0.228 drag coefficient, a 183-kilowatt motor, and integration of XPeng's latest VLA 2.0 vision-based advanced driver assistance system.

At the same time, the company unveiled an updated version of the G6, positioned as a direct rival to the Tesla (TSLA) Model Y. The 2026 edition features an enhanced XPILOT system powered by the Nvidia (NVDA) Orin X processor with 254 tera operations per second, delivering improved autonomous driving and sensing performance. It incorporates an 800-volt electrical platform that supports very rapid charging times of 10 to 80% in as little as 12 to 20 minutes. The All-Wheel Drive performance variant delivers 358 kilowatts of power and can accelerate from zero to 100 kilometers per hour in 4.13 seconds. This model also plays a central role in XPeng's expansion plans beyond China, with tailored versions prepared for markets including Australia and Europe.

Broadly, XPeng is pursuing a dual approach in its current strategy. It is targeting the mass market with more affordable MONA series vehicles to boost volume sales while focusing on premium offerings such as the G6, P7 Plus, and G9 to capture higher-end and international demand.

Additionally, XPeng has stepped up its efforts in autonomous mobility solutions. In May 2026, the firm announced the start of mass production for its first robotaxi developed entirely with in-house technology. Pilot operations are scheduled for the second half of 2026, with ambitions to achieve fully driverless commercial service by early 2027.

XPeng Is Not All About EVs, Is It?

Here is where the Turing AI chip represents a massive step forward for XPeng as the company aggressively transitions from relying on third-party hardware to fully internal custom silicon. This proprietary chip features a highly advanced 40-core processor and easily supports up to 30 billion parameters for large AI models. It also includes two independent neural network processing units and a unique domain-specific architecture optimized purely for physical AI applications.

What truly separates this chip from the generic (albeit more flexible) alternatives offered by established companies like Nvidia is its sheer processing density and specialized focus on embodied intelligence. A single Turing chip delivers tremendous computing power, and XPeng bundles three of them in their Next P7 sedan to achieve a staggering 2250 TOPS. This incredible processing capacity is roughly nine times higher than current industry standards.

Moving on to the humanoid robot known as Iron, its standout feature is that it operates on the same technological foundation as the automotive passenger fleet. The robot is powered by multiple Turing artificial intelligence chips and utilizes a highly specialized large model, which was specifically engineered for autonomous robotic actions. This sophisticated software allows the machine to achieve independent deep thinking and incredibly fluid physical motion. Furthermore, XPeng engineered all the critical mechanical components entirely internally, including the main operating systems, the robotic joints, and the highly advanced dexterous hands. This strategy completely contrasts with how most competitors build robots by simply piecing together generic parts from various external suppliers.

To actively drive growth, the company plans to integrate Iron directly into its commercial business operations. The initial rollout will see these intelligent machines deployed across XPeng retail showrooms, where they will function as interactive shopping guides and direct sales assistants.

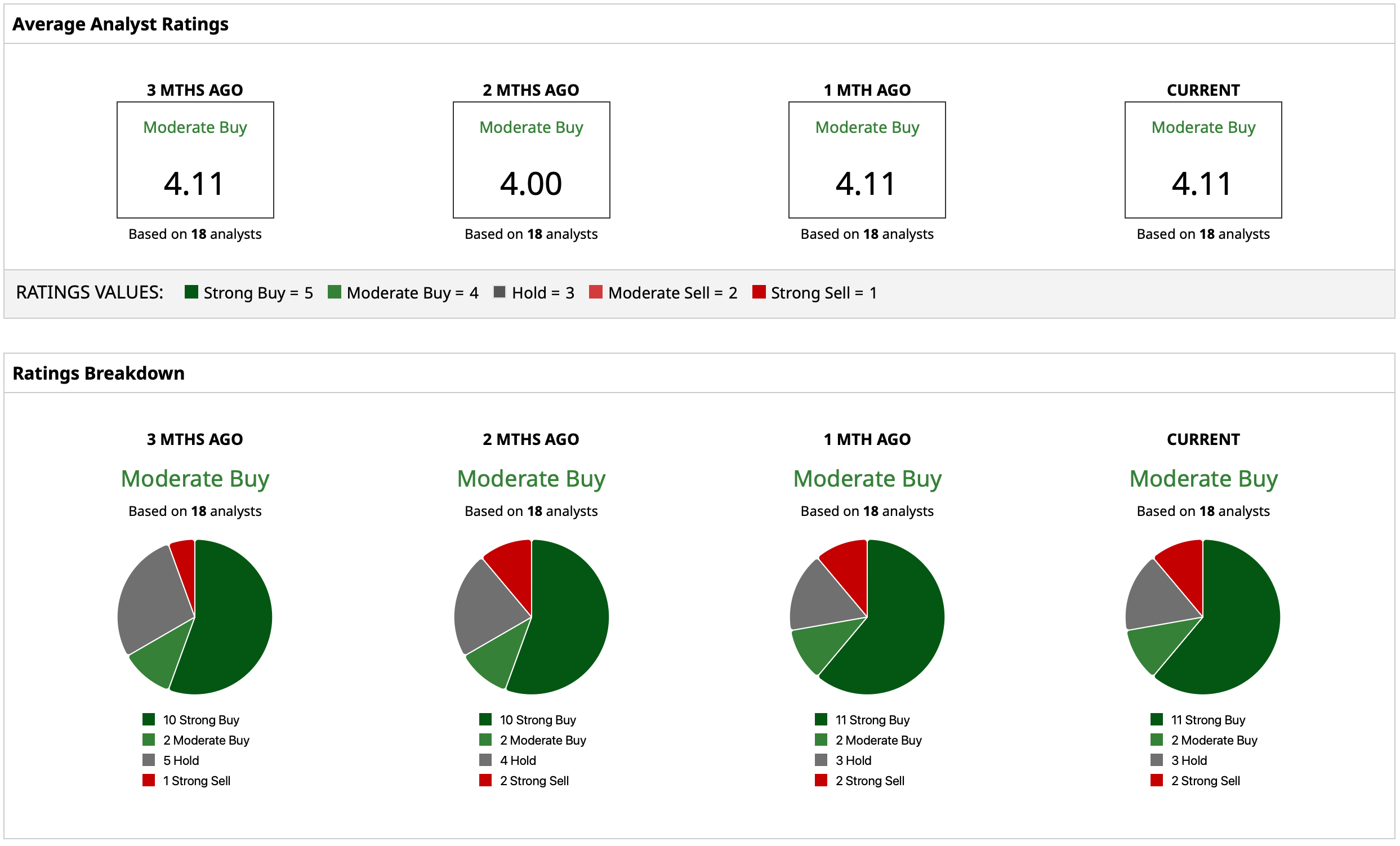

Analyst Opinion of XPEV Stock

Thus, analysts have deemed XPEV stock a “Moderate Buy” with a mean target price of $22.75. This denotes an upside potential of about 71% from current levels. Out of 18 analysts covering the stock, 11 have a “Strong Buy” rating, two have a “Moderate Buy” rating, three have a “Hold” rating, and two have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)