Advanced Micro Devices (AMD) is in focus today, after Benchmark analyst Cody Acree backed a “Buy” rating on the semiconductor giant. The bullish note follows a fireside chat with AMD’s CFO Jean Hu, which contributed to “further conviction in the company’s strong fundamental position” for Acree.

Why Benchmark Says AMD Stock is a ‘Buy’ Now

Citing the company’s increasing market share in both the PC and server markets relative to struggling rival Intel (INTC), Acree is upbeat about AMD’s “increasing competitiveness in the AI market.” In particular, the analyst says there’s reason to be optimistic about AMD adding Dell’s (DELL) corporate PC business to its artificial intelligence (AI) portfolio.

”Dell’s ramp alone should drive a material increase in the company’s commercial PC market share,” wrote Acree, who set a price target of $170 for AMD stock. That’s about 49% higher than current prices, and it’s also a generous premium to AMD’s average 12-month price target of $146.49 from analysts.

AMD Stock Moves Off the Lows

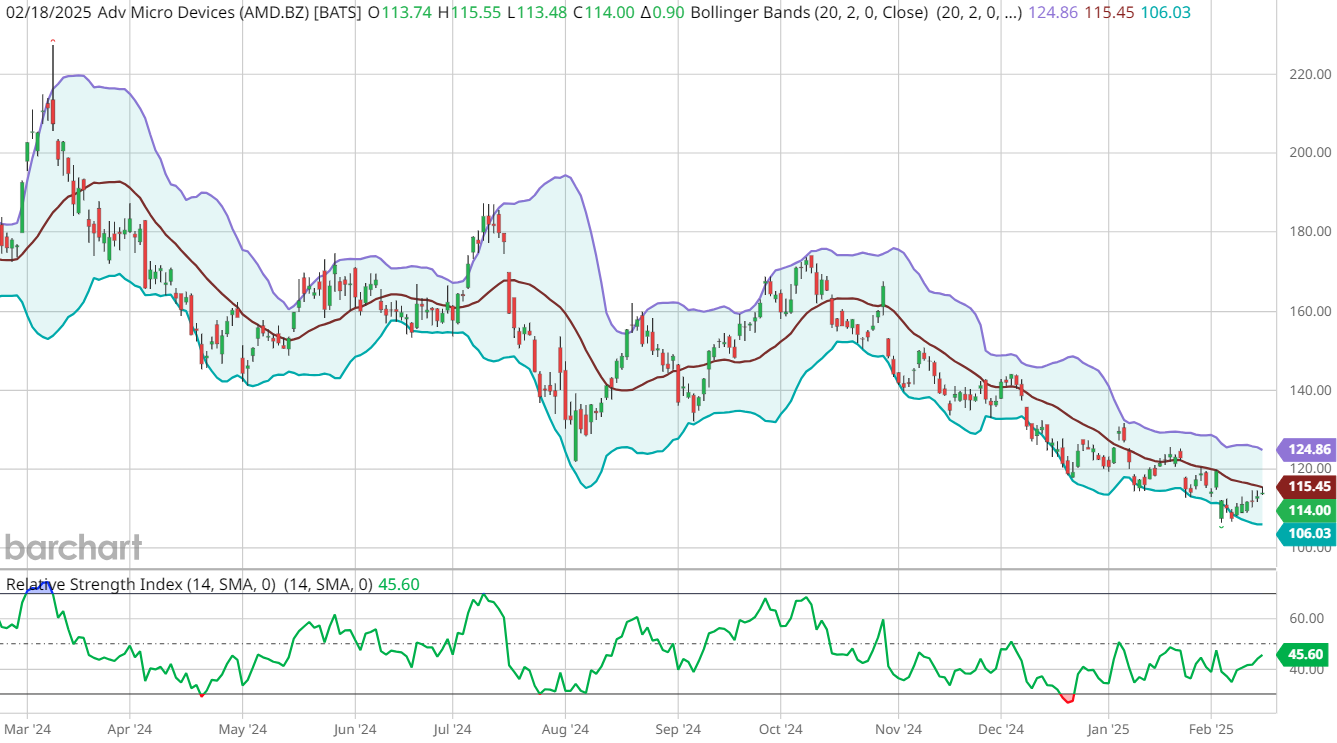

AMD is slightly higher this morning, chipping away at the 13% correction from its Jan. 7 year-to-date high. The shares are bouncing back from a recent break below their lower Bollinger Band, and are now sitting just below their 20-day moving average.

On a longer-term basis, the semiconductor stock has underperformed the broader market significantly over the past year, with a 52-week decline of 34%. However, AMD still boasts a 10-year return of 3,536%.

Trading at a forward price/earnings (P/E) ratio of 23.91, AMD stock presents an attractive valuation compared to its biggest competitors in the artificial intelligence (AI) chip market, like Intel (INTC), Nvidia (NVDA), and Marvell Technology (MRVL).

Should You Invest in AMD Now?

While the shares may be reasonably priced, investors should note that AMD's strategic positioning in the AI chip market offers both outsized upside potential - and serious challenges worth considering.

The company's data center segment demonstrated robust growth in Q4 2024, with a 69% year-over-year increase to $3.9 billion, though this marks a slowdown from the previous quarters' triple-digit growth rates. Management is projecting a 30% year-over-year revenue increase for Q1 2025, primarily driven by the anticipated ramp-up of their new Instinct MI350 GPUs.

AMD's strategic focus is also evidenced by their collaboration with France's CEA for developing next-generation AI computing architectures. Separately, a significant vote of confidence in AMD came from EVP Philip Guido's recent purchase of 4,645 shares, marking the first insider purchase since 2012.

However, some analysts have expressed concerns about weaker-than-expected guidance for the first half of 2025, and AMD continues to face stiff competition from dominant AI chip leader Nvidia. Going forward, the company's ability to execute on its MI350 GPU production plans and gain market share in the fiercely competitive AI chip market will be crucial factors in determining its future success.

This article was generated with the support of AI and reviewed by an editor. On the date of publication, the editor had a position in: NVDA , AMD . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here./Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)