Headquartered in Stamford, Connecticut, Charter Communications, Inc. (CHTR) is one of the largest broadband connectivity and cable operators in the United States, with a market capitalization of approximately $17.5 billion. Under its Spectrum brand, the company provides Internet, Mobile, Video, and Voice services, delivering seamless connectivity solutions to homes, businesses, and local communities across 41 states.

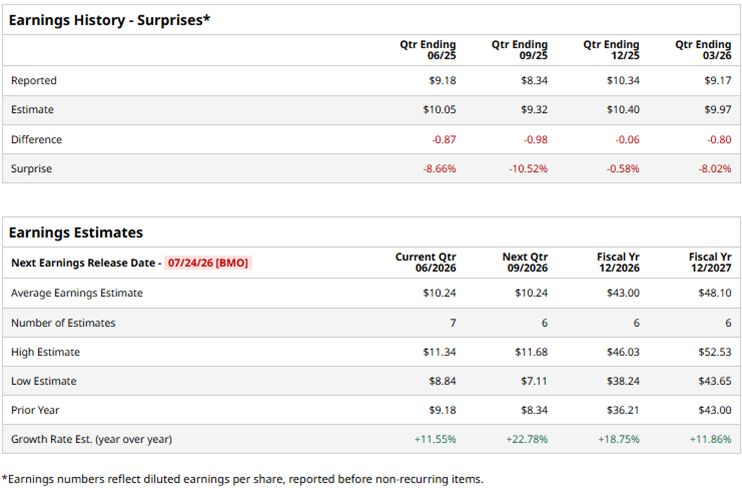

CHTR is scheduled to report its FY2026 Q2 earnings on Friday, July 24, 2026, before the market opens. Ahead of the release, analysts expect the company to report a diluted EPS of $10.24, representing a 11.6% increase from $9.18 in the year-ago quarter. However, Charter Communications has missed Wall Street's EPS estimates in each of the past four quarters.

For fiscal 2026, analysts expect CHTR to report an EPS of $43, up 18.8% from $36.21 in fiscal 2025. Likewise, EPS is projected to increase another 11.9% year over year to $48.10 in fiscal 2027.

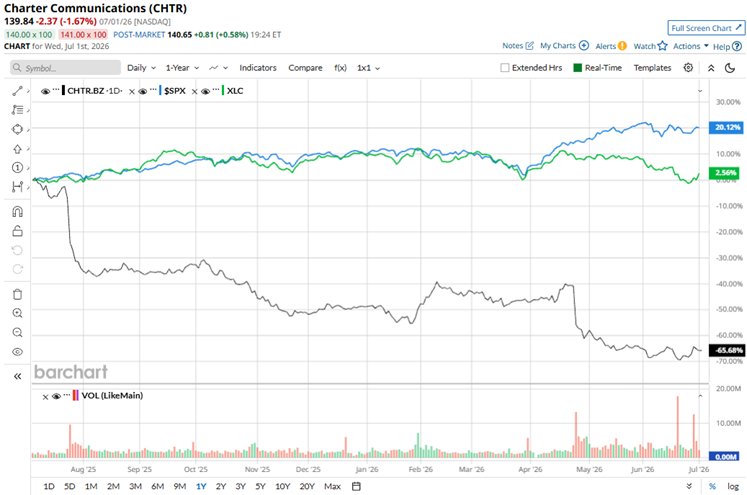

CHTR stock has plunged 66.6% over the past 52 weeks, significantly trailing the S&P 500 Index ($SPX), which returned 20.7%, and the State Street Communication Services Select Sector SPDR ETF (XLC), which gained 1.8% over the same period.

On June 29, Charter Communications shares rallied more than 9% after Bloomberg reported that the company had held discussions with SpaceX about launching a consumer phone service powered by satellite connectivity. The potential partnership is expected to combine Charter's wireless business with SpaceX's Starlink satellite network, helping extend mobile coverage to remote and underserved areas. While no agreement has been announced, investors welcomed the report as a potential growth opportunity that could strengthen Charter's competitive position in the wireless market and diversify its connectivity offerings.

However, analysts remain neutral on CHTR, with the stock carrying a "Hold" consensus rating. Among the 25 analysts covering the stock, seven rate it a "Strong Buy," 13 recommend "Hold," and five suggest a "Strong Sell." The average analyst price target of $242.89 implies a potential upside of 73.7% from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)