Exton, Pennsylvania-based West Pharmaceutical Services, Inc. (WST) designs, manufactures, and sells containment and delivery systems for injectable drugs and healthcare products. Valued at $25.4 billion by market cap, the company’s technologies include the design and manufacture of packaging components, research and development of drug delivery systems, and contract laboratory services and other services. The leading manufacturer of containment and delivery systems is expected to announce its fiscal second-quarter earnings for 2026 in the near term.

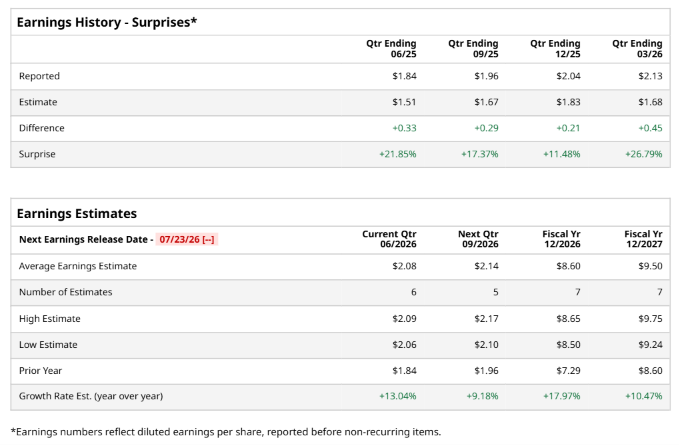

Ahead of the event, analysts expect WST to report a profit of $2.08 per share on a diluted basis, up 13% from $1.84 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect WST to report EPS of $8.60, up 18% from $7.29 in fiscal 2025. Its EPS is expected to rise 10.5% year-over-year to $9.50 in fiscal 2027.

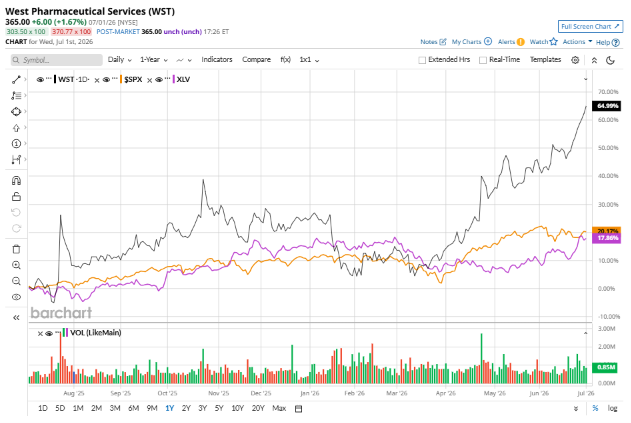

WST stock has outperformed the S&P 500 Index’s ($SPX) 20.7% gains over the past 52 weeks, with shares up 64.1% during this period. Similarly, it outperformed the State Street Health Care Select Sector SPDR ETF’s (XLV) 16.7% returns over the same time frame.

WST beat on surging HVP component demand and manufacturing improvements, with biologics up 26% and GLP-1/non-GLP-1 products gaining traction. CEO Eric Green pointed to strong execution and European output gains, while Annex 1-driven upgrades are shifting mix toward higher-margin products. Management lifted its outlook on HVP momentum and biologics penetration, with CFO Robert McMahon seeing continued margin expansion, though macro conditions warrant prudent forecasting.

Analysts’ consensus opinion on WST stock is bullish, with a “Strong Buy” rating overall. Out of 16 analysts covering the stock, 14 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and one gives a “Hold.” While WST currently trades above its mean price target of $360.87, the Street-high price target of $400 suggests an upside potential of 9.6%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)