Late Monday, the US president finally got around to making the much-ballyhooed announcement of 25% tariffs on all steel and aluminum imports to the Unite States.

Both the US dollar index and US stock index futures had already priced in the latest round of the endless game during Monday's session.

However, gold extended this week's early rally to as much as $80 before taking a breather.

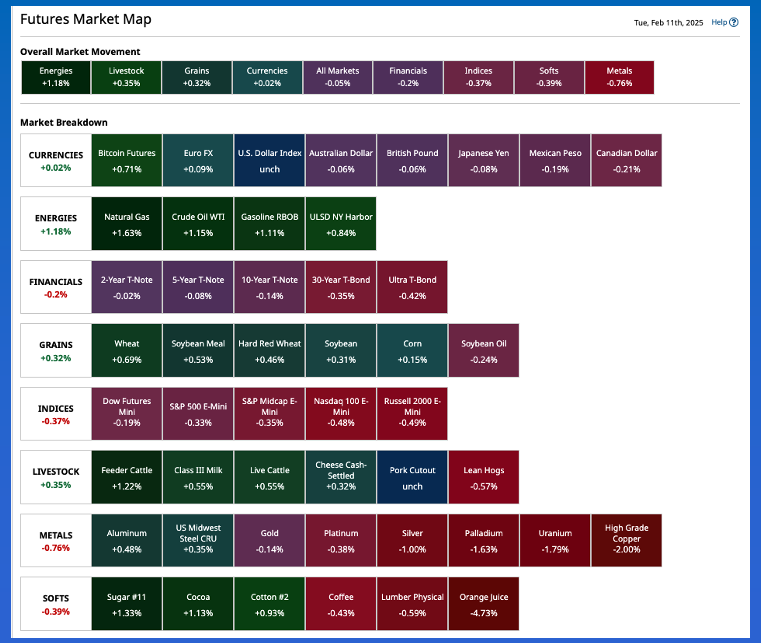

Morning Summary: It took a while Monday, but the US president eventually got around to putting the much-ballyhooed 25% tariffs on all steel and aluminum imports to the United States. Now we’ll wait to see what the retaliation is from US trade partners, then the retaliatory announcements from the US president to the retaliation, and so on in and endless circle. What are markets doing since the latest announcement? After firming Monday, the US dollar index is slightly weaker pre-dawn Tuesday. The same thing can be said for US stock index futures as markets showed small losses at this writing. As for the 3 Kings of Commodities, the latest from the US president didn’t have much of an effect. WTI crude oil extended Monday’s rally overnight with the spot-month contract adding as much as $1.01 (I always feel that $0.01 is important). Additionally, gains of 1.2% to 1.4% were consistent across the Energies sector. King Gold took a breather following Monday’s climb with the more heavily traded April contract down $2.80 to start the day. It’s interesting to note April (GCJ25) initially saw follow-through buying overnight, rallying as much as $34.10 and extending the early week gain to $80.90 before pulling back a bit.

Corn: The third King of Commodities – King Corn – had a quiet overnight session with contracts sitting fractionally lower early Tuesday morning on light trade volume. The nearby March issue posted a 2.5-cent trading range, from up 0.5 cent to down 2.0 cents while registering less than 17,000 contracts changing hands. May is showing fewer than 12,000 contracts traded as it also posted a 2.5-cent trading range. Will things spring to life around midday Tuesday? Most likely. The latest round of USDA’s monthly Supply and Demand imaginary numbers are set for release at noon (ET), as if Watson didn’t have enough to do trying to relearn to ignore the madness from Pennsylvania Avenue. Fundamentally, the corn market hasn’t changed much. I had a question come in Monday evening regarding corn’s latest available stocks-to-use readings. At the end of January, with the National Corn Index ($CNCI) priced near $4.50, corn’s available stocks-to-use was 12% as compared to the end of December’s 12.3%. Monday evening saw the Index calculated near $4.5875 putting the latest available stocks-to-use figure at roughly 11.9%. My Monday evening national average basis calculations came in at 32.75 cents under March and 45.75 cents under May futures, generally unchanged from last Friday’s figures.

Soybeans: The soybean market was quietly in the green to start the day. The nearby March issue posted a 7.0-cent trading range overnight, from down 3.5 cents to up 3.5 cents on trade volume of 12,500 contracts and was sitting 2.0 cents higher at this writing. In fact, March through July were all showing a gain of 2.0 cents with trade volume readings falling to 7,200 contracts for May and 2,000 contracts of July. Given we are nearing the midpoint of February with the Goldman Roll and Brazil’s harvest ongoing, attention is turning to the first deferred May issue (ZSK25). There continues to be chatter about harvest delays across parts of Brazil due to rain. This hasn’t had much of an effect on the May-July soybean futures spread[i], though. Recall last Friday saw the deferred spread covering 55% calculated full commercial carry as compared to the previous week’s close when it covered 53%. For the record, the two week’s prior saw the May-July covering 40% and 37% respectively, meaning we can see a clear trend. On the other hand, my Monday evening national average basis calculations came in at 64.25 cents under March and 80.25 cents under May futures, both roughly 0.25 cent firmer than last Friday’s figures.

Wheat: The wheat sub-sector was higher across the board. This is not a shocking development given all three markets closed lower to start the week. Fundamentally, not much has changed with the three markets as all seem to be trying to make their way through the relatively dull winter season. If there is something to watch with old-crop it would be the ongoing Variable Storage Rate tracking period (through Friday, February 21) for winter wheat, with the spotlight on the SRW March-May futures spread. Through Monday’s close, the running daily average was 56% calculated full commercial carry, holding above the low end 50% that would trigger a decrease in the official rate come March 19. (Can you tell there really isn’t much to talk about with wheat?) Anyway, both new-crop winter markets remain neutral-to-bearish with the SRW July-September spread covering 61% while the same spread in the HRW market covered 76% at Monday’s close. Keep in mind the bearish threshold is 67%. Further out, the September-December HRW spread covered 68% as we wait for the crop to come out of dormancy. For the record, March SRW was sitting 4.0 cents higher to start the day, 0.5 cent off its session high on light trade volume of about 5,300 contracts.

[i] However, these same Brazilian soybean harvest delays are having an effect on the May-July corn futures spread as planting of Brazil’s second corn crop – the safrinha crop – is pushed back as well. This is part of Rule #4A (A market that can’t go down won’t go down) that I’ve talked about recently in corn.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)