/Caterpillar%20Inc_%20equipment-by%20pabradyphoto%20via%20iStock.jpg)

After years of overperformance from tech stocks, there are some shifting winds in the stock market this year. The reign of tech stocks—powered by hyperscalers and chipmakers—appears to be giving way to the much more mundane world of waste management, plumbing, and electrical wiring—companies found in the industrials sector.

Consider this: the S&P 500 Information Technology Sector Index ($SRIT) gained nearly 70% from 2024-25, by far outdistancing the 36% gain of the S&P 500 Industrials Sector ($SRIN). But so far this year, Industrials have the edge, 17.7% to 15.6%. And in the last month, Industrials are up 5% while the technology sector has tumbled nearly 5%.

The Industrials Sector Index reached an all-time high last week, with analysts attributing the change to investors’ bullish feelings toward the economy and manufacturing stocks. Industrials offer cyclical exposure, solid earnings, and long-term growth and are still undervalued compared to high-flying tech stocks.

If you think the U.S. is gearing up for a manufacturing boom, these three stocks are poised to deliver. All of them are showing solid gains so far this year.

Industrial Stock #1: Caterpillar (CAT)

Headquartered in Irving, Texas, Caterpillar (CAT) is a well-known manufacturer of construction and mining equipment, diesel and gas engines, and industrial turbines. It also benefits from the AI buildout, as Caterpillar makes fast-response natural gas generators used by data centers to provide a continuous power source. The company has a market cap of $460 billion.

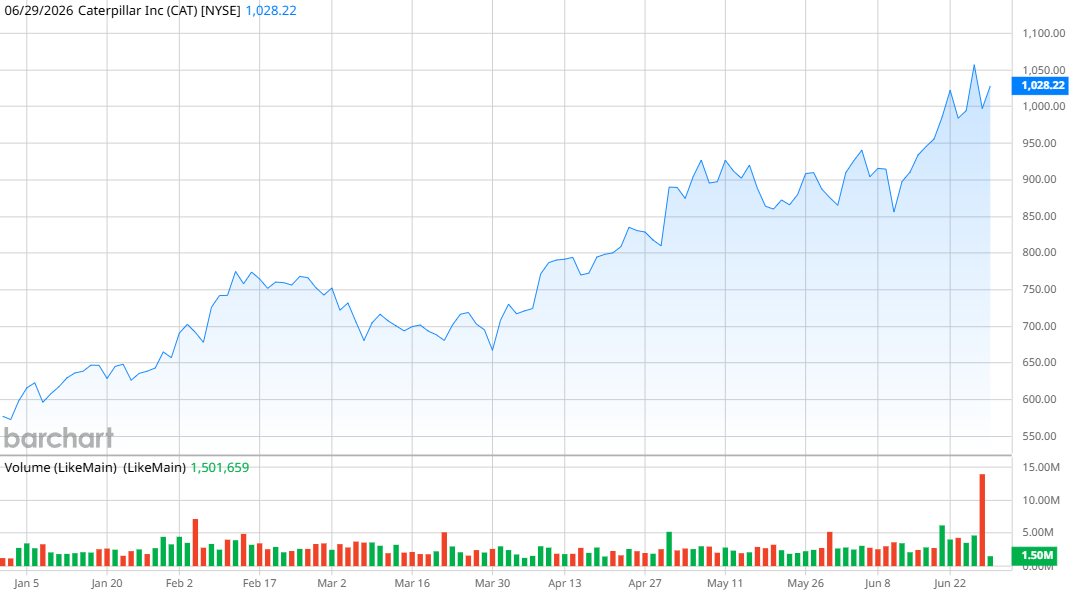

Shares in the last year are up a whopping 175%, by far outstripping the S&P 500 and the Industrials sector. Caterpillar also pays a quarterly dividend that equates to a yield of 0.6%.

However, CAT stock has started to become a little pricey—which is to be expected given how quickly the price has jumped. Shares trade at a forward price-to-earnings ratio of 41.6, which is double the five-year P/E mean of 20.2.

Revenue in the first quarter was $17.4 billion, up 22% from a year ago, and earnings came in at $5.47 per share. The company reported a record backlog of $63 billion, and EPS increased 30%, showing that demand is helping Caterpillar prosper despite rising costs and tariffs squeezing profit margins to 17.7%, down from 18.1% a year earlier.

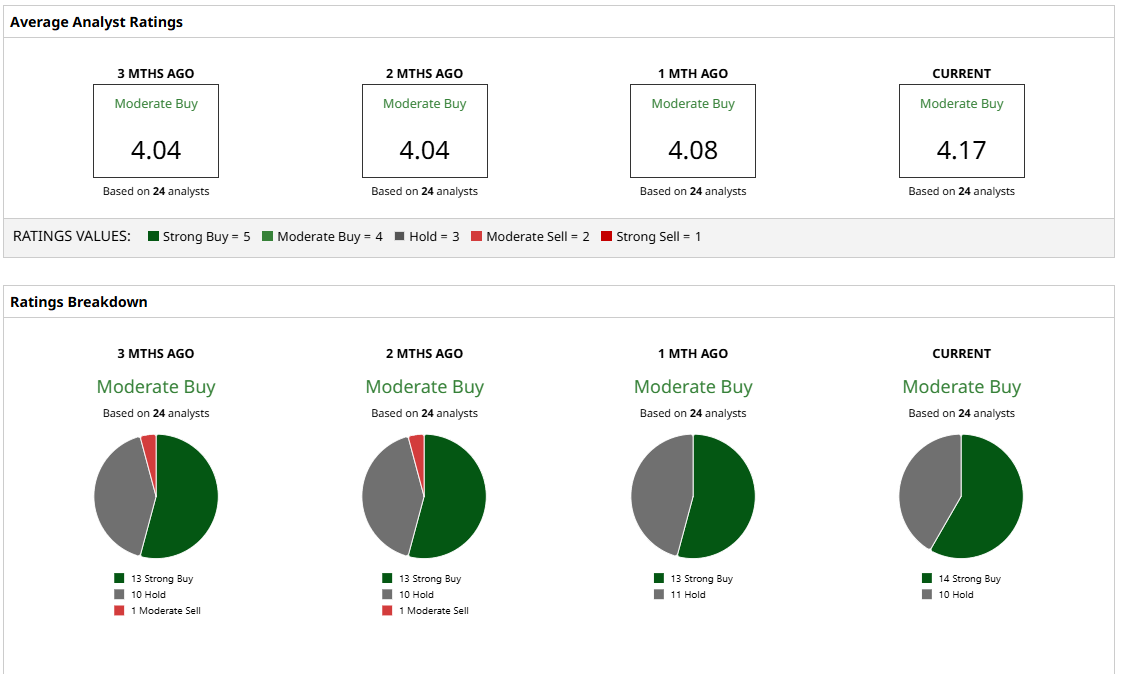

Analysts give CAT stock a consensus “Moderate Buy” rating. The mean price target of $969 is below the current share price due to the stock’s recent rerating, but that will change as analysts update their views. Wells Fargo increased its price target on June 23 from $1,050 to $1,155, and J.P. Morgan increased its price target on June 22 from $1,125 to $1,165.

Industrial Stock #2: Hubbell (HUBB)

Hubbell (HUBB) is deeply involved in the electrical trade, manufacturing the infrastructure needed to transmit, distribute, and control electricity safely. It makes electrical products for utilities and for industrial, commercial, and residential markets. The company, which is headquartered in Shelton, Connecticut, has a market cap of $27 billion.

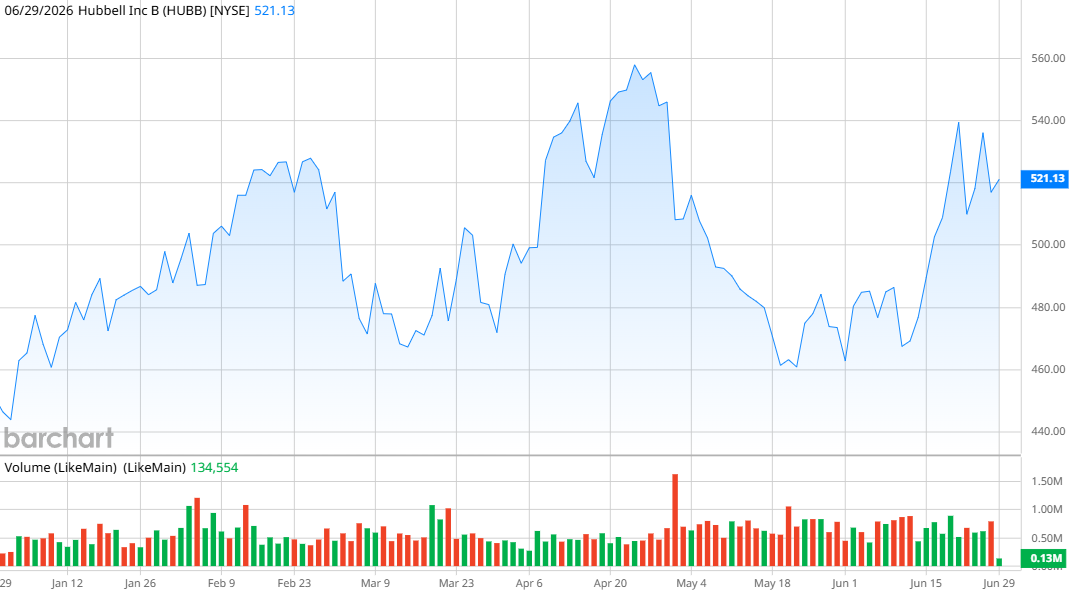

Shares in the last year are up 28%, including a jump of 10% in the last month. Hubbell is also a dividend stock, with a quarterly payout that equates to a 1.1% yield. The company also recently completed its $3 billion cash purchase of NSI Industries from Sentinel Capital Partners, adding NSI’s line of electrical components and wire management products to Hubbell’s portfolio.

HUBB stock trades at a forward P/E of 25.8, which is just below its mean of 26.6.

Revenue in the first quarter was $1.51 billion, up from $1.36 billion a year ago. Net income was $183 million, an increase from $164.5 million, and earnings per share of $3.42 was an improvement from $3.04 in Q1 2025. Management is projecting total revenue growth of 8% to 11% this year, with EPS in the range of $17.45 to $18.

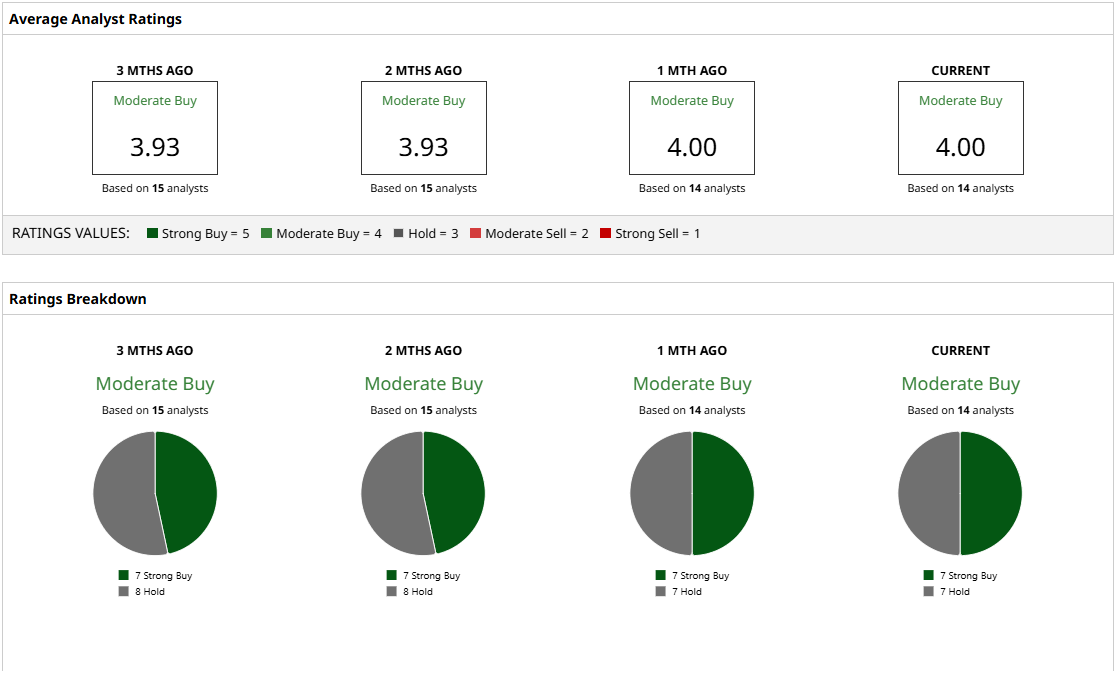

Analysts have a consensus “Moderate Buy” rating on HUBB stock, with a mean price target of $556 that represents potential upside of nearly 10%.

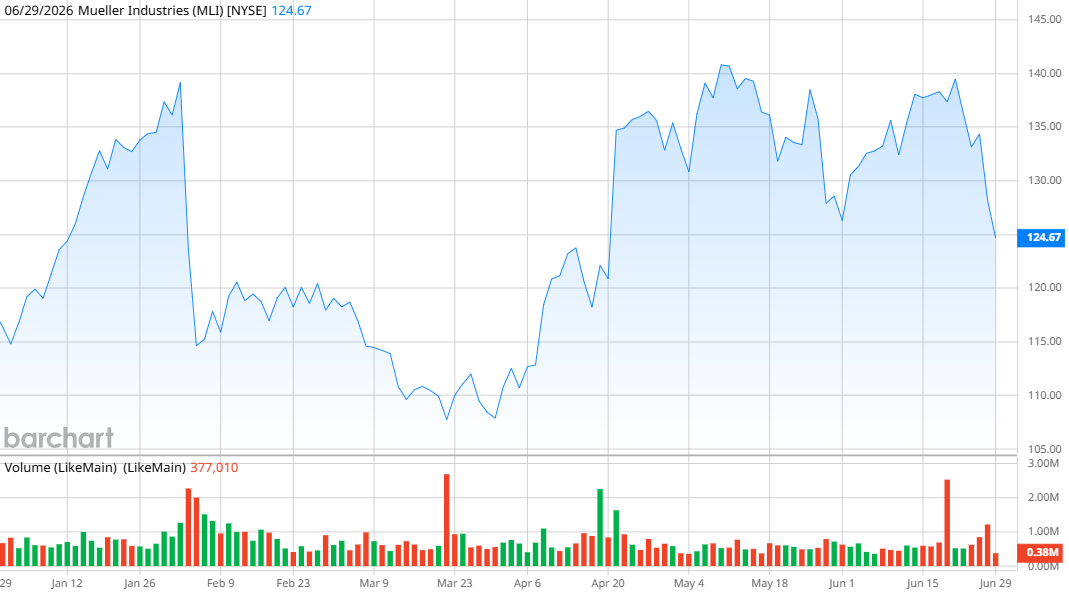

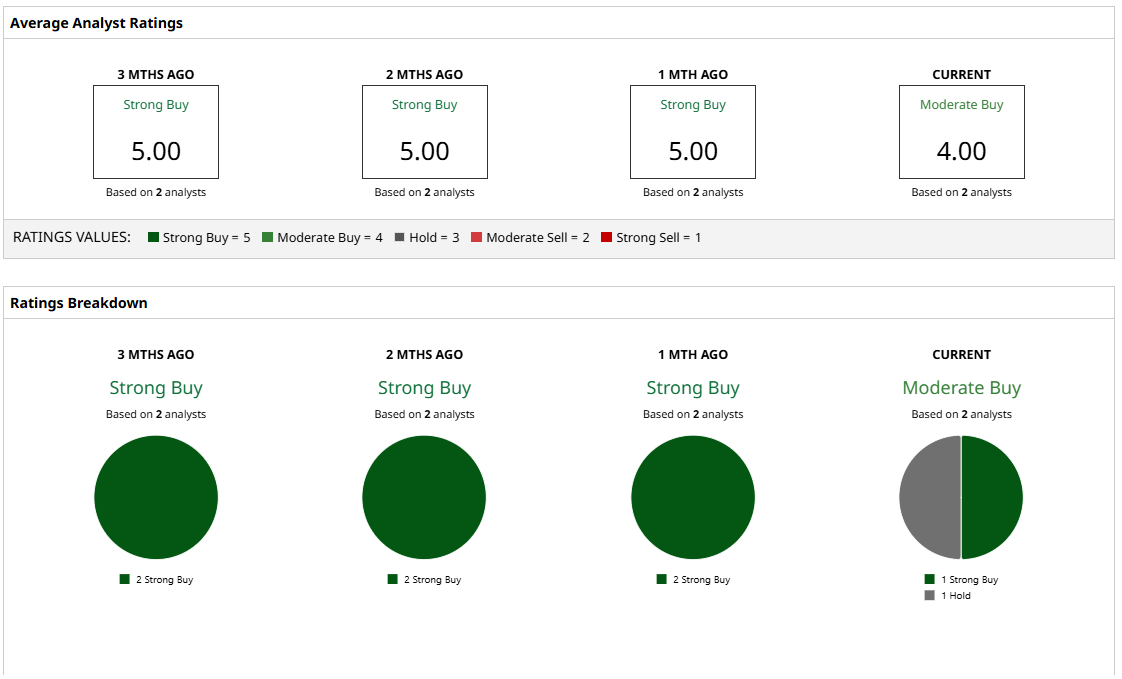

Industrial Stock #3: Mueller Industries (MLI)

Mueller Industries (MLI) is an industrial manufacturing company. Based in Collierville, Tennessee, Mueller makes components for plumbing and HVAC, including copper, brass, and plastic plumbing tubes and fittings. It has a market cap of $14.2 billion.

Shares are up 54% in the last year, although they remain 13% off Mueller’s all-time high. Investors also benefit from the quarterly dividend that yields just more than 1%.

MLI stock also carries the cheapest valuation of the stocks relative to its peers on this list, with a forward P/E of 14.8. However, keep in mind that it’s pricey for Mueller, which has a five-year mean P/E of 10.5.

Earnings for the first quarter included revenue of $1.19 billion, up from $1 billion a year ago. Net income increased to $259 million from $157.4 million, and EPS of $2.16 was an improvement from $1.39 in the first quarter of 2025. The company ended the quarter with $1.38 billion in cash and no debt.

Mueller is also growing—it completed its purchase of Bison Metals Technologies at the end of the first quarter. Management said the purchase will benefit Mueller’s copper tube manufacturing capacity. “Out of the gate, the integration has been seamless and successful,” Mueller CEO Greg Christopher said.

Analysts give a consensus “Moderate Buy” rating to MLI stock, with a mean price target of $149 that represents potential upside of about 20%.

On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)