/A%20photo%20of%20a%20corporate%20Qualcomm%20sign%20by%20JHVEPhoto%20via%20Adobe%20Stock.jpeg)

Qualcomm (QCOM) is in the process of executing one of the most aggressive data-center pushes in its history, a move that will help the company diversify away from a handset market currently facing a historical decline. On its Investor Day held on June 24, the company laid out its ambitious AI infrastructure strategy. Where just a couple of years ago Qualcomm had zero data-center revenue, it now expects to go as high as $15 billion in annual data-center revenue by 2029.

News of the company’s recent acquisition is a step in this direction. Qualcomm is acquiring Modular, an AI infrastructure software company founded by Chris Lattenr and Tim Davis. Modular is the company that built Mojo, a Python-based programming language for AI. The firm has also built MAX, a next-generation AI developer platform built on top of Mojo, that helps streamline AI development and deployment.

Modular helps developers build infrastructure-agnostic AI. Instead of writing code for Nvidia’s (NVDA) CUDA or AMD’s (AMD) ROCm, they can develop software that can run efficiently across any vendor’s hardware. This dents a company like Nvidia significantly, which has had developers tied into its ecosystem for years.

Qualcomm CEO Christiano Aoan also pointed out the above, saying that the deal will help the company move toward openness rather than vertical lock-ins. The current state of the AI industry is quite disaggregated, something that was the motivation for Modular’s founders to build their product as well. Now that Qualcomm is acquiring the company, one can expect it to become a major force in data-center expansion in the U.S. and globally.

About Qualcomm Stock

Qualcomm is a semiconductor company that designs and develops wireless connectivity solutions for smartphones, automotive systems, data centers, and IoT devices. Its product portfolio includes its flagship Snapdragon processors, AI accelerators, radio frequency systems, and 5G modems. Founded in 1985, the company is headquartered in San Diego, California.

Over the last 12 months, QCOM stock has increased 17%, slightly underperforming the S&P 500’s ($SPX) 21% gain during the same period. The rise has primarily been driven by Qualcomm’s strategic decision to diversify beyond smartphones into data centers, automotive, and IoT. The stock is down 29% from its 52-week high, potentially offering investors an attractive entry point ahead of expected near-term growth.

Qualcomm’s valuation looks somewhat attractive on an earnings basis, considering the significant data-center growth opportunity, with its forward price-to-earnings (P/E) ratio at 23.7 times. Meanwhile, the price-to-sales (P/S) ratio of 4.5 times sits at a slight premium compared to the five-year average.

The premium on revenue feels justified with the scale of non-handset expansion expected. With CFO Akash Palkhiwala himself stating that handset revenue will reach its bottom in the next quarter, analysts expect an earnings decline of 20% in fiscal 2026, followed by a less than 1% gain in 2027. However, the long-term growth seems a lot more promising, with a 43% acceleration expected in 2029 as management has guided $40 billion in non-handset revenue by that year. Net debt of $5.47 billion also looks manageable for a company with a $198 billion market capitalization that has returned $3.7 billion to shareholders in a single quarter.

Qualcomm Beats Consensus Earnings Estimates

Qualcomm reported second-quarter fiscal 2026 earnings on April 29. The firm reported revenue of $10.6 billion, beating the analyst consensus. Non-GAAP EPS of $2.65 also beat estimates. While memory supply constraints caused handset revenue to decline 13% year-over-year (YOY), the firm was able to make up for it with its other segments. The automotive segment surpassed the $5 billion annualized revenue milestone for the first time in company history, whiel the IoT segment also increased 9% YOY.

For Q3, Qualcomm guided for revenue of $9.2 billion to $10 billion, with non-GAAP EPS of $2.10 to $2.30. CEO Christiano Amon confirmed that Qualcomm will begin delivering its first-ever custom-designed AI chips to a major cloud computing company later this year, a landmark moment for the firm in the data-center segment. The auto segment’s momentum is expected to continue as well, with 50% YOY growth estimated, putting Qualcomm on track to exceed $6 billion in annualized revenue for fiscal 2026.

What Are Analysts Saying About Qualcomm Stock?

Morgan Stanley analyst Joseph Moore raised Qualcomm’s price target significantly from $146 to $231 following the firm’s Investor Day, while upgrading his rating from “Underweight” to “Equal Weight.” DZ Bank analyst Ingo Wermann also increased his price target from $195 to $265 while upgrading to a “Buy” rating. The positive shifts in analyst ratings indicate that Qualcomm’s Investor Day has been a success in winning Wall Street’s confidence.

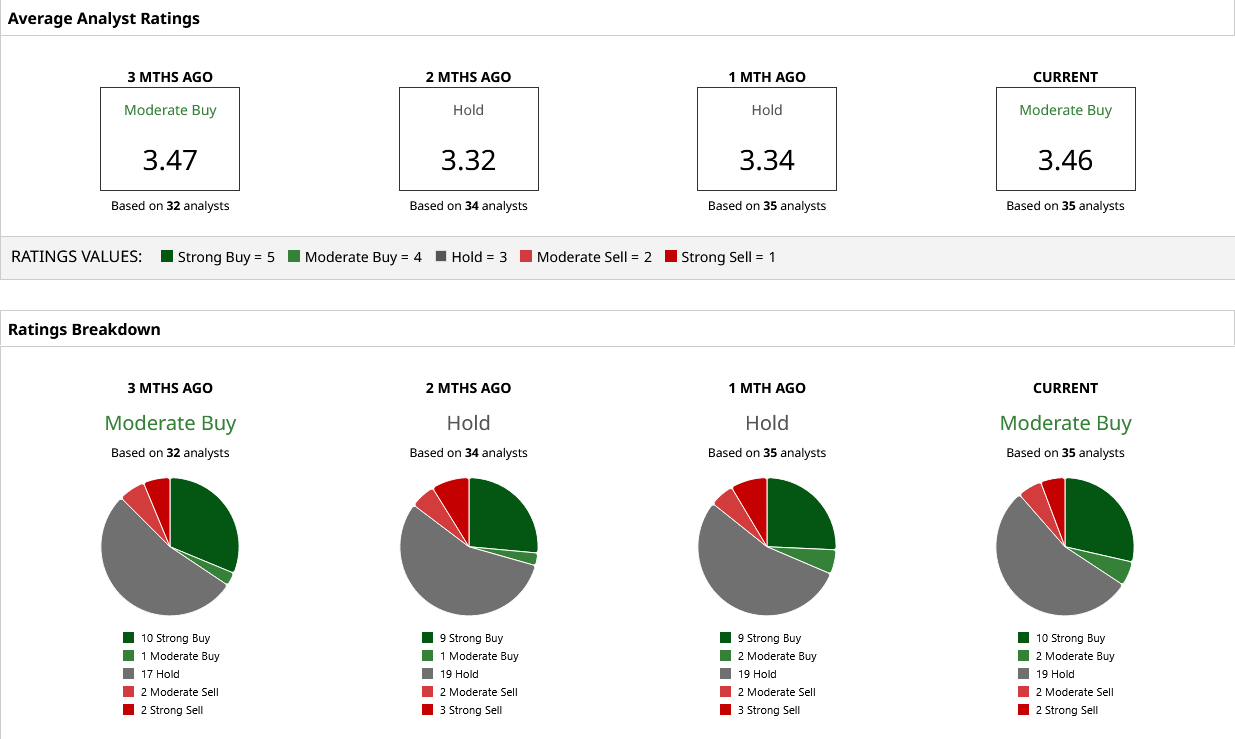

Based on the 34 analysts with coverage, QCOM stock holds a consensus “Moderate Buy” rating. The mean price target of $212.33 indicates potential upside of 15% from current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)