If you own Tesla (TSLA), July 2 could be one of the most important dates of the year. That's when the electric vehicle giant is expected to report its second-quarter delivery numbers, giving investors their first real look at whether demand is recovering after a volatile start to 2026.

A strong report could reignite the stock's rally. A disappointing one could quickly send shares lower. The good news is that Goldman Sachs just raised its Q2 EV delivery forecast, implying a solid gain over last year’s quarter.

Add in hype around Tesla’s humanoid robot Optimus 3 and the continued work on self-driving robotaxis.

Together, these catalysts make Tesla a high-watch stock now. The stock has underperformed the market this year as macro headwinds, heavy spending, and slowing EV sales have weighed on results. But a better‑than‑feared delivery number or other tech breakthroughs could spark a rally.

How Did Tesla Stock Perform

Tesla shares have gained 33.1% over the past year, although the stock remains down 15.27% from its December high of $498.83 as investors continue debating EV demand, valuation, and the pace of its AI ambitions. On Monday, June 30, shares surged 8.46% after optimism surrounding the upcoming delivery report intensified.

That makes July 2 more than just another data point. It could determine the market's next move.

Even after this year's volatility, Tesla remains one of the market's most expensive large-cap stocks.

The company trades at 319.44 times forward price-to-earnings and 15.08 times forward sales, valuations that are dramatically higher than those of traditional automakers. Investors clearly aren't paying for today's vehicle business alone. They're betting Tesla can become a leader in artificial intelligence, autonomous transportation, robotics, and energy storage.

July 2 Could Be a Make-or-Break Day for Tesla

The buzz this week is all about Tesla's Q2 delivery report due on July 2. Wall Street's average estimate currently calls for about 406,000 vehicle deliveries, according to the consensus compiled by Tesla from 22 sell-side analysts. Goldman Sachs is even more optimistic, recently raising its forecast to 420,000 deliveries, well above the broader consensus, after stronger-than-expected sales trends across key markets including Europe and China.

Yet, Goldman Sachs isn't the only bull on Wall Street. Barclays expects Tesla to deliver about 418,000 vehicles in the second quarter, while Morgan Stanley recently raised its forecast to roughly 413,000.

Morgan Stanley cited European registrations that more than doubled in May and improving demand in China as key reasons for its optimism.

However, the U.S. remains a potential weak spot. Cox Automotive estimates Tesla's domestic sales could decline about 20% year-over-year (YOY), partly due to the expiration of the $7,500 U.S. federal EV tax credit at the end of Q3 2025.

Moreover, Investors are also watching Musk’s timeline. He said Optimus robot production starts in July and the next‑gen robot reveal is likely later this year.

In short, traders should keep an eye on three things: surprising EV sales numbers, any news on robotaxis/humanoids, and margin improvements.

Tesla Beats Q1 Earnings

Tesla's latest earnings offered investors plenty to like, even if they weren't perfect. In the first quarter of 2026, revenue climbed 16% YOY to $22.4 billion, while both earnings and revenue came in modestly ahead of Wall Street’s expectations.

Automotive revenue rose to $16.2 billion, while the company's fast-growing services business, including Full Self-Driving subscriptions and charging, jumped more than 40% to $3.7 billion. And, Tesla generated $1.44 billion in free cash flow and finished the quarter with an impressive $44.7 billion in cash and short-term investments, giving it plenty of financial flexibility.

Still, investors aren't celebrating just yet. Tesla's profit margins remain well below their historical highs as the company continues pouring billions into future growth. CEO Elon Musk foresees 2026 as a very exciting year as Tesla ramps up spending on AI infrastructure, new factories, autonomous driving, and its Optimus humanoid robot. Wall Street expects another YOY revenue increase in the second quarter, with analysts projecting roughly $24.65 billion in sales and nearly $102 billion in revenue for all of 2026.

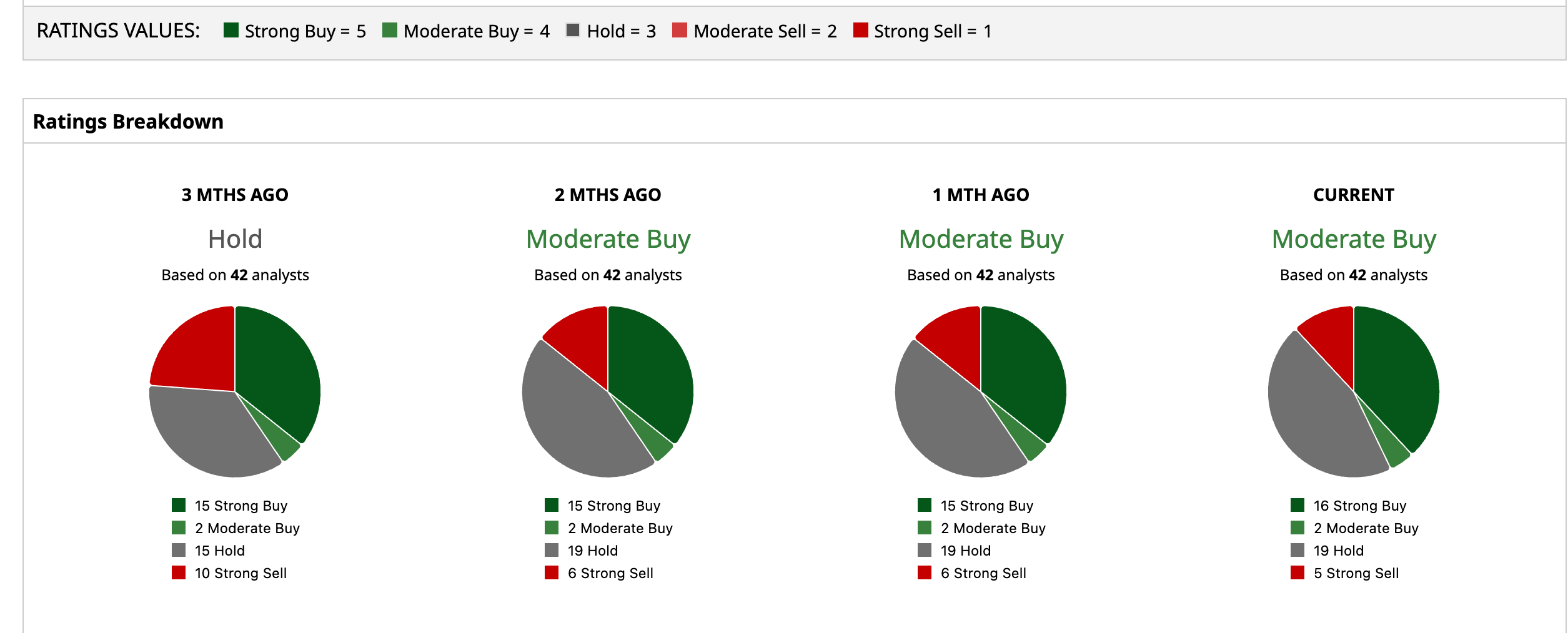

Wall Street Opinion on TSLA Stock

Wall Street is divided. Of 42 analysts, the overall consensus is a “Moderate Buy” rating. An average 12‑month target of $412.39, implies a 2.62% downside from current levels. Goldman Sachs currently gives a “Neutral” rating and says Tesla needs to make progress in autonomy and robotics to justify its valuation.

Morgan Stanley likewise holds an "Equal-Weight" rating with a $415 price target, noting that near-term delivery volumes might slow before longer-term gains kick in.

By contrast, Barclays is bearish with an “Underperform” call, setting a $360 target and warning that EV demand and competition could limit Tesla’s profits.

All told, bulls believe Tesla's technological progress and future advances in AI, while pessimists fear overvaluation and challenges due to the market. Tesla stock is almost priced for perfection, according to current analysts, as well as the average price target suggests. However, even more bullish price targets of $600 imply as much as 41.68% upside if Tesla delivers significant improvements.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)