/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

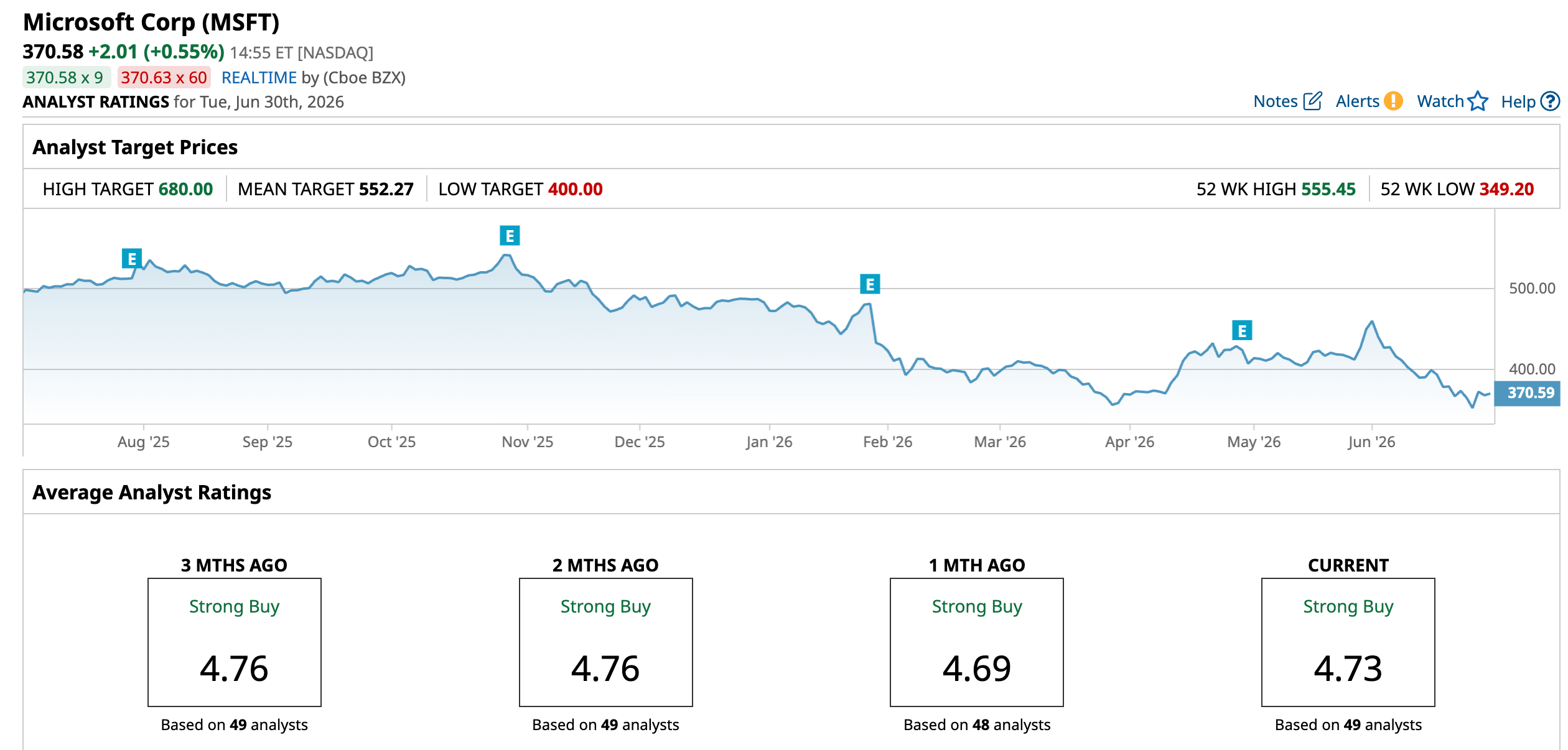

Microsoft (MSFT) stock has fallen 23.35% year-to-date (YTD) and is now trading slightly above its 52-week low, making it the worst-performing Magnificent 7 stock this year.

The biggest concern weighing on Microsoft stock is its massive investment in artificial intelligence (AI). The tech giant plans to spend $190 billion on capital expenditures through 2026, with higher AI infrastructure and component costs leading to an increase in planned spending.

While these aggressive investments position Microsoft to strengthen its leadership in AI and cloud computing, they are also putting pressure on profit margins in the near term. Further, investors have been hoping that its aggressive AI spending will accelerate Azure’s growth, but that hasn't happened yet.

Instead, Azure's growth is expected to improve only gradually in the near term. Management says ongoing supply constraints, particularly limited AI infrastructure capacity, will likely persist through at least 2026, limiting Azure’s growth despite strong interest in its AI offerings.

As a result, the combination of surging capital spending, margin pressure, and slower-than-expected cloud growth has weighed heavily on investor sentiment, pushing Microsoft shares sharply lower.

Even so, the recent sell-off has made Microsoft's valuation attractive. Meanwhile, the company continues to deliver solid underlying growth. Let's take a closer look at two compelling reasons for buying Microsoft stock today, which could prove to be a smart move.

Reason 1 – Demand Outpaces Capacity

At first glance, Azure's growth guidance disappointed investors. However, Microsoft isn't struggling with demand, it's struggling to add capacity fast enough to meet demand. Across enterprise workloads and customer segments, demand for Azure infrastructure continues to exceed available supply.

The underlying business remains exceptionally strong. Enterprises continue to accelerate AI adoption, cloud workloads continue to expand, and demand for compute capacity remains robust.

MSFT’s quarterly numbers highlight solid demand. In the latest quarter, Microsoft generated $82.9 billion in revenue, up 18% year-over-year (YOY). Azure and other cloud services grew 40%, driven by broad-based enterprise AI adoption across industries and geographies.

Microsoft's AI business is also scaling at an extraordinary pace. AI revenue run rate now exceeds $37 billion annually, growing 123% YOY. Adoption of Microsoft 365 Copilot also continues to accelerate. The company now has more than 20 million paid Microsoft 365 Copilot seats, and the number of customers with more than 50,000 seats has jumped significantly over the past year.

Microsoft's commercial remaining performance obligation (RPO), which represents contracted future revenue, continued to expand. RPO nearly doubled, rising 99% to $627 billion, with about one-quarter expected to be recognized as revenue over the next 12 months. Even more encouraging, longer-duration commitments increased 138%, suggesting customers are making multi-year investments in Microsoft's AI and cloud platform rather than pulling back on spending.

Looking ahead, management expects the momentum to continue. Intelligent Cloud revenue is projected to reach as much as $38.25 billion next quarter, representing growth of up to 28%, while Azure is expected to maintain growth near 40% in constant currency.

Overall, Microsoft is witnessing strong demand, and as new AI infrastructure capacity comes online, Azure’s growth could accelerate, leading to a rebound in MSFT stock.

Reason 2 – MSFT’s Valuation Remains Compelling

Microsoft’s attractive valuation further strengthens its investment appeal. Despite its strong position in the AI market and solid growth prospects, MSFT trades at a lower valuation than many of its large-cap technology peers and relative to its earnings growth.

Microsoft is currently valued at a forward price-to-earnings (P/E) ratio of 22.26 times. That appears reasonable given analysts' expectations for earnings per share (EPS) growth of 22.9% in fiscal 2026, followed by 15.1% in fiscal 2027. By comparison, Alphabet (GOOG) (GOOGL) trades at a forward P/E of 23.59 times, while Amazon (AMZN) commands a significantly higher multiple of 30.16 times.

MSFT’s compelling valuation offers an opportunity to buy now.

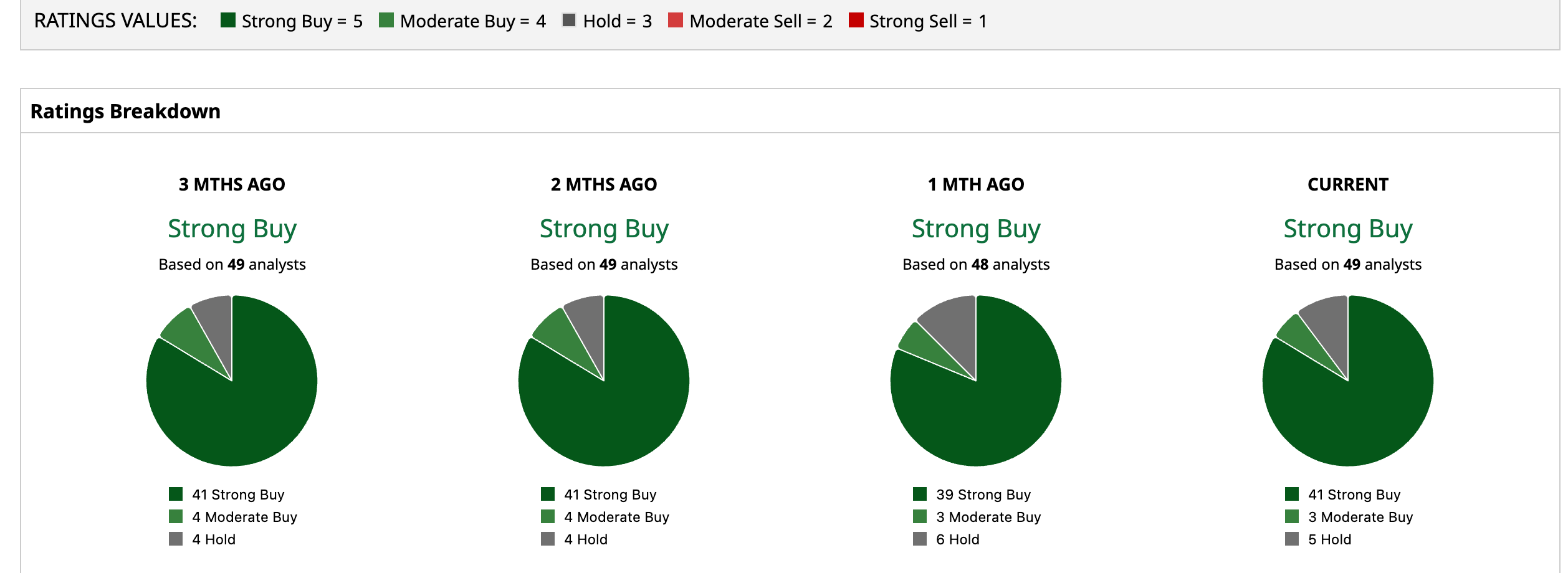

Microsoft Rates As a “Strong Buy”

In the near term, Microsoft's significant investments in AI infrastructure and ongoing capacity constraints could continue to pressure profit margins and weigh on investor sentiment. However, the company's underlying fundamentals remain strong. Demand for Azure and AI services continues to grow, long-term customer commitments are expanding, and earnings are expected to remain healthy.

Given its strong long-term growth outlook and attractive valuation, Microsoft appears to be a convincing buy at current levels. Analysts currently rate MSFT stock a “Strong Buy.”

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)