/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

Microsoft (MSFT) is a global technology powerhouse and one of the world's largest companies by market capitalization. Under visionary CEO Satya Nadella, the firm has orchestrated one of the most consequential corporate pivots in technology history, transforming from a legacy software vendor into a definitive AI enterprise platform. Operating across three world-class segments — Productivity and Business Processes, Intelligent Cloud, and More Personal Computing — Microsoft's AI flywheel is accelerating at an extraordinary pace.

Microsoft Stock Under Pressure

MSFT stock has fallen roughly 25% in the past 12 months and 23% on a year-to-date (YTD) basis, placing it among the weakest performing “Magnificent Seven” stocks this year despite the S&P 500's ($SPX) more than 9% gain so far this year. Shares have fallen approximately 33% from their 52-week high of $555.45 to around $370 per share, giving investors their best entry point into Microsoft since 2023.

Against the S&P 500 Information Technology Index's ($SRIT) strong gains in 2026, MSFT stock has dramatically underperformed the broader tech sector, with investor concerns centered on $190 billion in 2026 capital expenditures and near-term margin compression. However, over the past decade, MSFT stock has delivered an annualized return of about 24%, nearly double the S&P 500's roughly 13% average, underscoring the long-term compounding power of this business when viewed through the right time horizon.

Microsoft Posted Strong Results

Microsoft reported third-quarter fiscal 2026 total revenue of $82.9 billion, up 18% year-over-year (YOY), beating the $81.4 billion analyst consensus estimate. Meanwhile, diluted EPS of $4.27 surpassed the $4.06 estimate by approximately 5%, up 23% YOY. Azure and other cloud services surged 40% YOY, with Intelligent Cloud revenue jumping 30% to $34.7 billion and Productivity and Business Processes growing 17% to $35 billion. Despite the decisive beats across revenue and EPS, shares of MSFT fell modestly post-earnings as investors fixated on forward capex guidance rather than historical results.

Microsoft Cloud gross margin came in at 66%, declining from the prior year due to AI infrastructure investments and growing AI product usage, while operating income grew 20% to $38.4 billion at a 46.3% operating margin. The company returned $10.2 billion to shareholders through dividends and buybacks in the quarter, maintaining its dividend growth streak. Capital expenditures reached $31.9 billion in Q3, with full-year 2026 capex projected at approximately $190 billion.

For Q4 2026, CFO Amy Hood guided for revenue of $86.7 billion to $87.8 billion, Azure growth of 39% to 40% at constant currency, and capex exceeding $40 billion for the quarter alone. Copilot commercial seats are expected to grow sequentially in Q4, driving continued average revenue per user growth. Management's unwavering $190 billion capex commitment signals that, whatever the near-term margin pressure, Microsoft is betting its entire future on AI becoming the defining computing paradigm of the next decade.

Microsoft Hikes Xbox Prices

Microsoft is raising Xbox console prices worldwide starting Aug. 1, driven by a surge in storage and memory component costs, with further increases expected through late 2027. The tech giant will increase prices by $100 for 512GB models and $150 for 1TB models, while discontinuing its 2TB console entirely. This follows a $20 to $70 U.S. price hike announced in October 2025.

Microsoft acknowledged that gaming consoles face unique vulnerability to component cost pressures, as they are typically sold near manufacturing cost. After exhausting supplier negotiations, the company determined price increases were unavoidable. To soften the impact, Microsoft is introducing buy-now-pay-later options (BNPL) through its own stores, interest-free financing via Amazon (AMZN), trade-in programs through retail partners, and discounted refurbished consoles.

Should You Buy MSFT Stock?

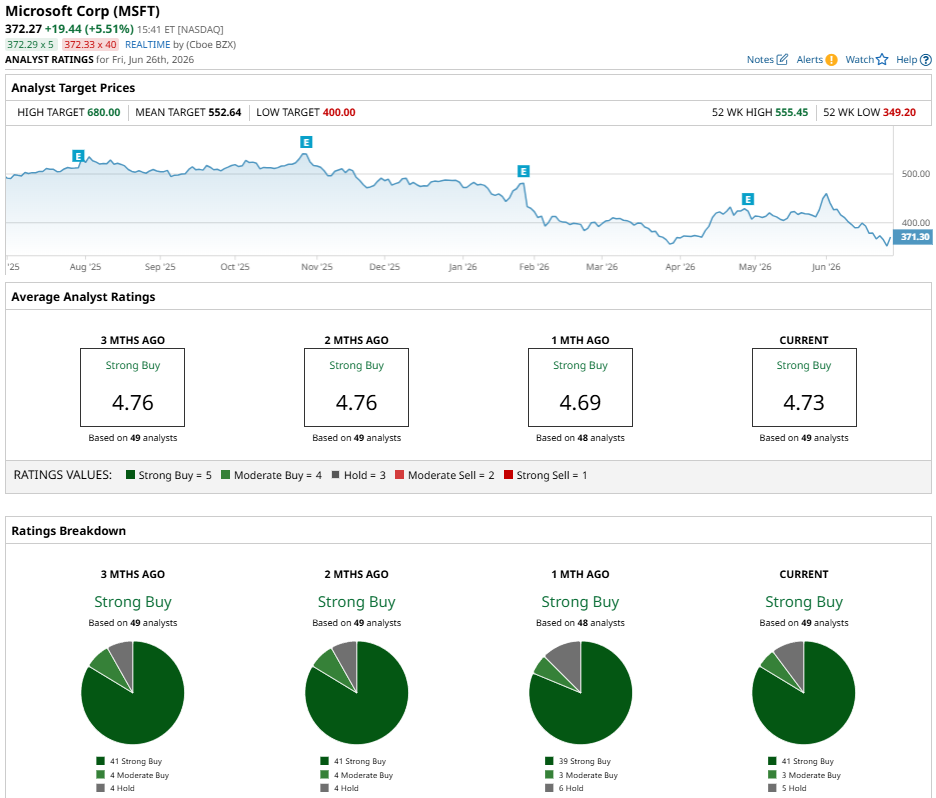

Despite the Xbox price hikes reflecting real cost pressures, Microsoft's challenges appear manageable within its broader business. Wall Street remains overwhelmingly bullish, with MSFT stock carrying a consensus "Strong Buy" rating from 49 analysts with coverage, including 41 "Strong Buy" ratings, three “Moderate Buy” ratings, and just five "Hold" ratings. The mean price target of $552.27 suggests roughly 49% potential upside from current levels.

For investors, short-term console headwinds are unlikely to derail a company of Microsoft's scale and diversification.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)