/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

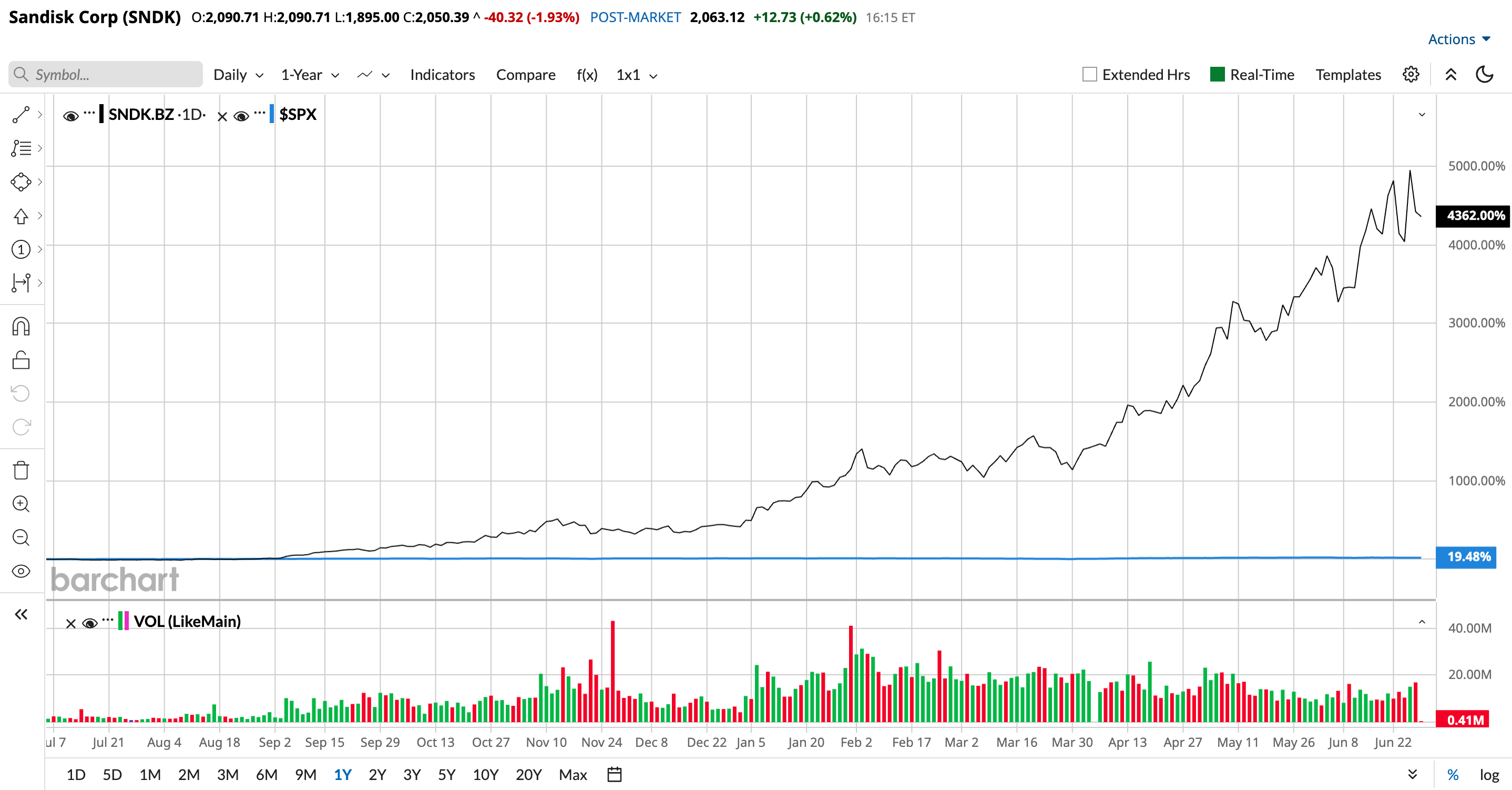

SanDisk (SNDK) has emerged as one of the hottest AI infrastructure plays in the market today. Shares are up a mind-blowing 4,262.7% over the past year and 766.4% so far this year. Sandisk stock has captured the same limelight that Nvidia (NVDA) did a few years ago. This optimism isn’t just based on hype alone. Analysts increasingly believe the company is entering one of the strongest NAND flash memory cycles in years, fueled by AI, enterprise storage demand, and tightening industry supply. This has led to many analysts raising the price targets for the stock.

Should investors buy SanDisk stock now?

Wall Street is Strongly Bullish About SanDisk Stock

Several Wall Street analysts have been quietly increasing their price targets, indicating that they believe SanDisk's earnings power will continue to grow despite its massive gains. This month, Mizuho analyst Vijay Rakes became more bullish on SanDisk, raising its price target from $1,825 to $2,200, while maintaining an “Outperform” rating. Rakes now expects AI tensor processing unit shipments to reach 35 million units by 2028, roughly eight times the projected 4.3 million units in 2026, highlighting the significant growth potential of AI infrastructure demand.

Meanwhile, Cantor Fitzgerald turned even more bullish, lifting the price target to $2,900 from $1,800, while maintaining his “Overweight” rating. The firm believes the memory industry has entered a new AI-driven growth cycle with sustainable long-term demand, adding that the current rally is still in its early stages rather than nearing its peak. Similarly, BofA analyst Wamsi Mohan raised the price target to $2,100 from $1,550, with a “Buy” rating, as Mohan expects fiscal 2027 revenue to climb to $44 billion, alongside earnings per share (EPS) of $188.

More recently, Citi analyst Asiya Merchant recently increased her price target on SanDisk from $2,025 to $2,500 while maintaining a “Buy” rating, citing a favorable outlook for the NAND market and growing AI-related memory demand.

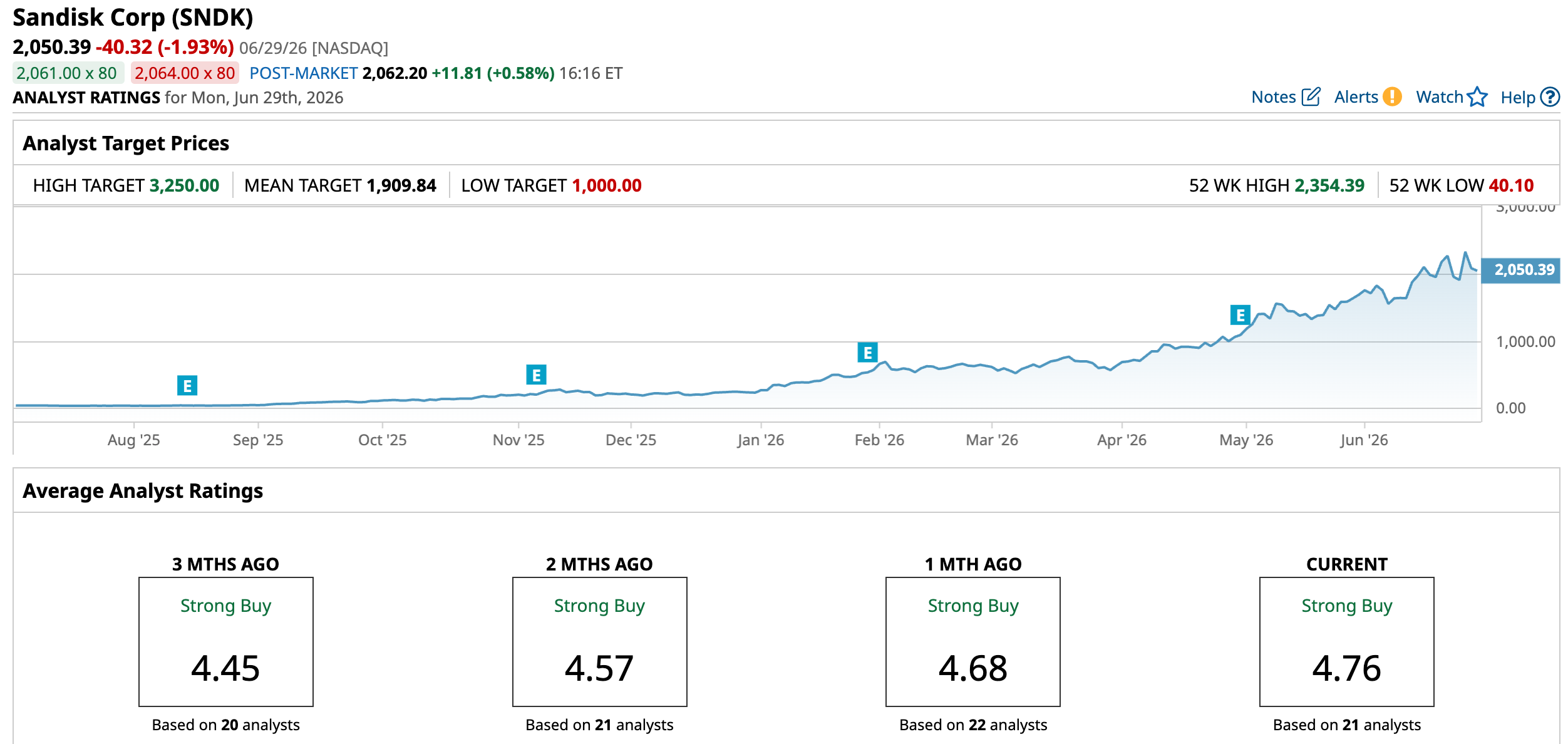

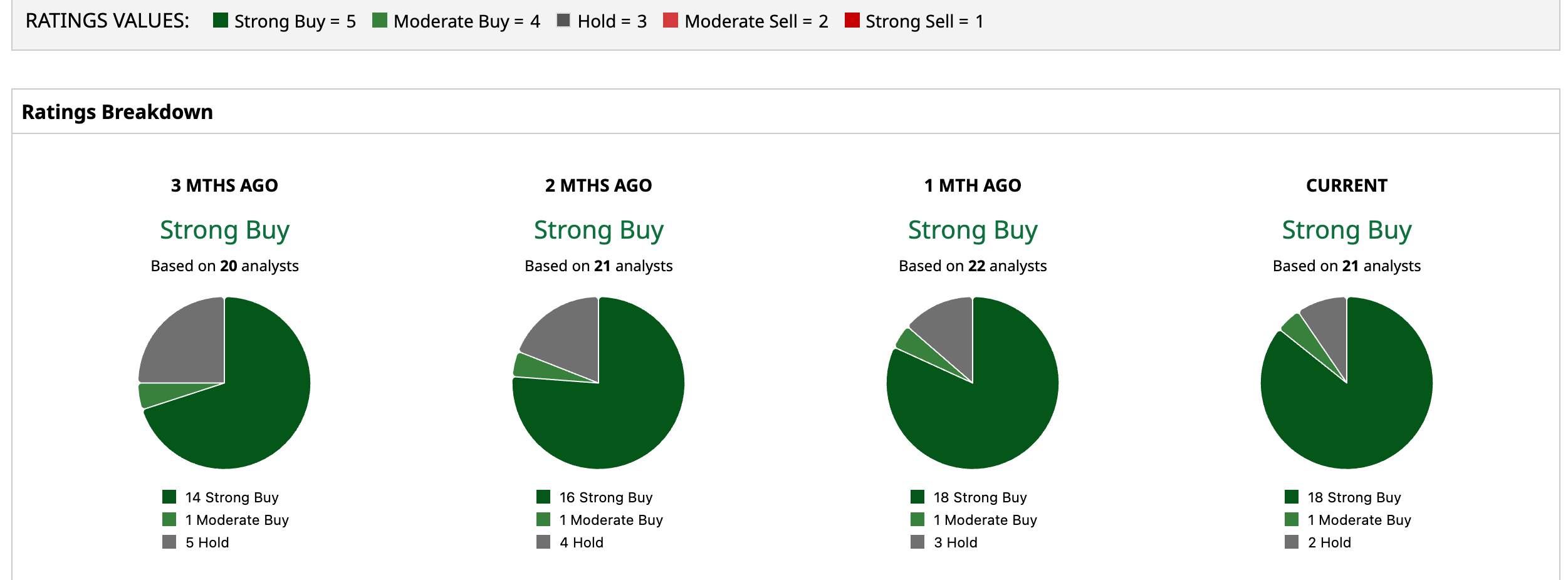

Overall, SanDisk stock holds a consensus “Strong Buy” rating. Of the 21 analysts covering the stock, 18 rate it a “Strong Buy,” one says it is a “Moderate Buy,” and two rate it a “Hold.” The stock has already rallied past its mean target price of $1,909.84. And analysts now expect it to skyrocket even higher by 58.5% to hit $3,250 over the next 12 months.

AI Is Creating a New Memory Supercycle

Much of this optimism stems from the growing realization that AI requires far more storage than many investors initially expected. Not just GPUs, but every AI model needs enormous amounts of high-speed storage to hold training datasets, checkpoints, inference models, and enterprise workloads. That has made NAND flash memory an increasingly important piece of AI infrastructure, with suppliers such as SanDisk more critical to the AI boom.

SanDisk’s revenue grew 251% year-over-year (YOY) to $5.9 billion in the third quarter of fiscal 2026, fueled by stronger NAND pricing and growing demand from higher-value customers. Adjusted earnings per share (EPS) jumped to $23.41 from a $0.30 loss a year earlier. The data center business, in particular, stood out, with a sequential revenue increase of 233% to $1.4 billion, as AI workloads drove demand for high-performance flash storage.

The company strongly hinted that memory is no longer cyclical. It believes that the new multiyear supply partnerships, which management refers to as "new business models" (NBMs), are a significant growth driver. These agreements are designed to give customers guaranteed access to NAND flash supply while providing SanDisk with committed revenue and stronger financial visibility. The company has already signed five multiyear agreements, with the longest contract extending as long as five years. Plus, the five deals signed so far include more than $11 billion in financial guarantees. Looking ahead, management expects the momentum to continue, forecasting $7.75 billion to $8.25 billion in fourth-quarter revenue, 79% to 81% in adjusted gross margin, and adjusted earnings of $30 to $33 per share.

Furthermore, Micron’s (MU) earnings released last week further reinforced the bull case for memory suppliers like SanDisk. Micron delivered stronger-than-expected fiscal third-quarter 2026 results, which revealed an optimistic outlook for AI-driven memory demand. The Q3 print showed investors and analysts that the current memory cycle isn't limited to just one company but reflects broader industry strength. These trends have boosted confidence that this cycle has more room to run.

Analysts See SanDisk Earnings Moving Higher

A jump in price targets often follows upbeat earnings expectations. Over the last three months, analysts have revised SanDisk’s revenue and earnings estimates 17 times. Analysts now expect an eye-catching 3,496% increase in fiscal 2026 earnings to $64.01, followed by another 181% increase to $179.82 per share in fiscal 2027. These higher earnings projections provide a clearer justification for increasing price targets rather than just investor enthusiasm.

Turning to valuation, despite its impressive rally, SanDisk stock may not be as expensive as expected. Based on fiscal 2027 estimates, the stock trades at a forward price-to-earnings multiple of 11 times. If these earnings projections materialize, SanDisk is essentially trading at a discount now to its future earnings power. This explains why several analysts continue to raise their price targets.

Even so, after such a rapid rally, the stock could see periods of profit-taking. The stock has already dipped 9.84% over the last five days due to a broader sell-off in AI and tech stocks.

While investors should expect some volatility after such a massive run, the factors driving analysts’ optimism are rooted in improving memory industry conditions rather than anything cyclical. If AI infrastructure investment remains strong and NAND pricing stays favorable, SanDisk could continue benefiting for years to come.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)