/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

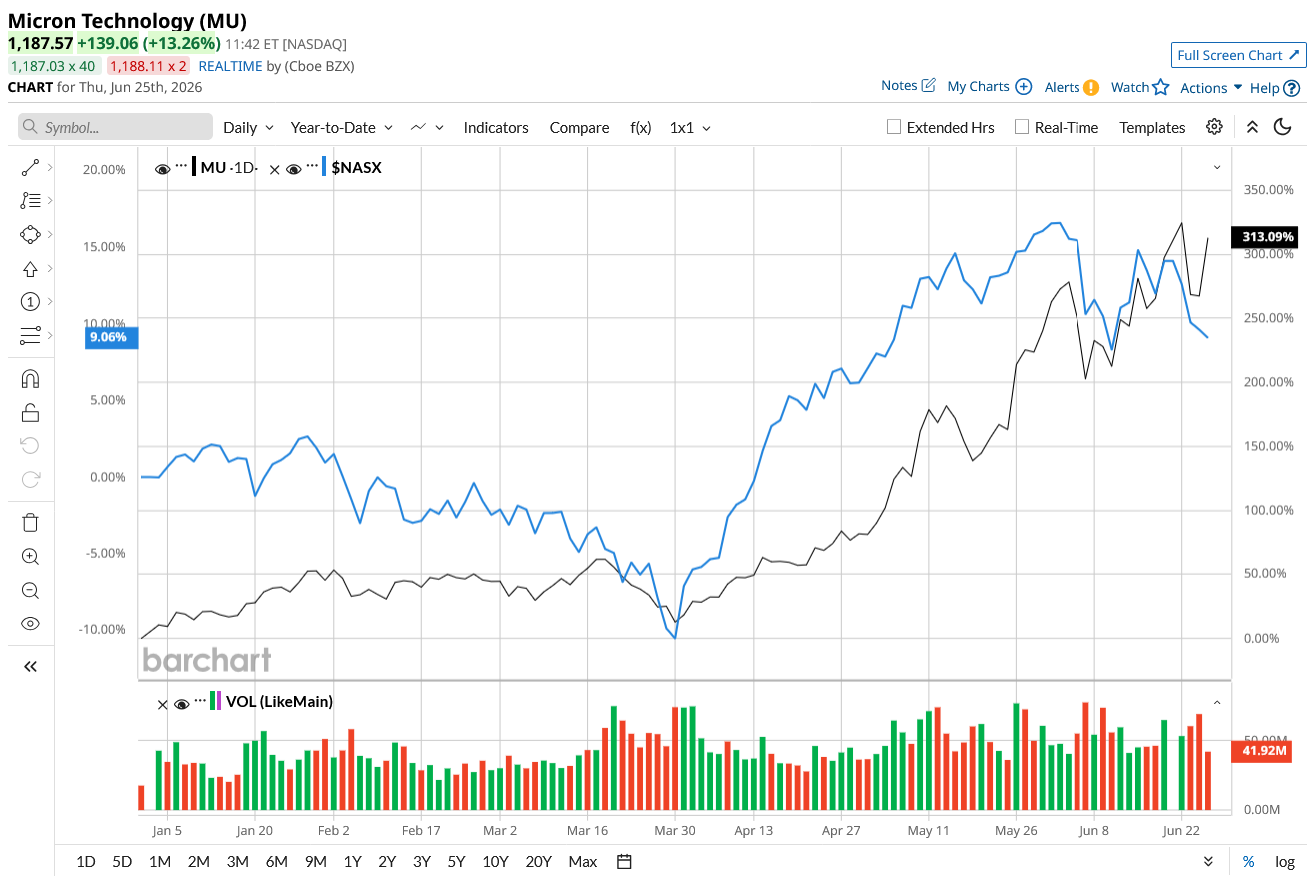

Micron Technology’s (MU) fiscal third-quarter 2026 results were not simply another strong quarter in a hot semiconductor cycle. The numbers showed investors what an AI-driven memory market with skyrocketing demand and tight supply could look like. For a company long associated with the booms and busts of the memory cycle, Micron’s Q3 carried an even bigger message for investors, and MU stock is up over 13% today. Let’s find out what the message was that got MU climbing the chart and investors looking toward the future.

Micron’s revenue in the third quarter climbed an eye-popping 346% year-over-year (YoY) to $41.5 billion, marking its fifth consecutive quarterly revenue record. Management said the $17.6 billion sequential revenue increase was the biggest increase in company history. Adjusted diluted earnings per share (EPS) surged 106% YoY to $25.11, while adjusted gross margin climbed to 85%.

AI is now the force reshaping the memory and storage industry. Micron generated more than $25 billion in data center revenue, putting the business on an annualized run rate above $100 billion. Micron's data center revenue comes from both its DRAM portfolio and NAND-based storage solutions. On the DRAM side, Micron is benefiting from rising demand for server DRAM, particularly HBM (high-bandwidth memory), a premium type of DRAM paired with AI accelerators like GPUs. Meanwhile, data center SSDs are driving a significant increase in NAND revenue, which has surpassed $5 billion and more than doubled sequentially.

Overall, DRAM revenue climbed 343% YoY and 67% sequentially to reach $31.3 billion, accounting for 76% of total revenue. Similarly, NAND revenue reached $9.9 billion, up 99% sequentially and 361% YoY, representing 24% of total revenue. The bigger driver was pricing, with DRAM prices up in the low-60% range and NAND prices up in the mid-80% range.

Within Micron’s other reporting segments, the Cloud Memory Business Unit generated $13.8 billion in revenue, up 78% sequentially, while the Mobile and Client Business Unit generated $11.5 billion in revenue, up 49% sequentially. Additionally, the Automotive and Embedded Business Unit also generated $4.6 billion in revenue.

Strategic Customer Agreements Were the Highlight of Q3

Perhaps the company’s new strategic customer agreements, or SCAs, may be the biggest reason to believe this cycle is different. Micron has entered into 16 strategic customer agreements (SCAs) spanning the data center, consumer, and automotive end markets. Most of these contracts run from calendar 2026 through 2030, while automotive agreements are typically shorter at around three years. Notably, these deals involve four very large and three medium-sized customers. At the end of fiscal Q3, remaining performance obligations (RPO) stood at more than $5 billion.

Importantly, management stated that 14 of the 16 signed agreements will generate around $100 billion in revenue at the minimum price per contract over the remainder of the period. Additionally, Micron anticipates receiving $22 billion in cash deposits and related financial commitments under the SCAs signed so far. These agreements reveal that Micron’s customers increasingly view memory supply as strategic and are willing to commit capital and volumes years in advance.

AI Demand Is No Longer a Niche Tailwind for Micron

Micron had been benefitting from higher demand for HBM. Investors assumed that this demand could be just related to the AI boom and might weaken and go through the cycles again. But Micron’s data center growth is no longer just an HBM story. Interestingly, the quarter showed that Micron is benefiting from a much bigger AI buildout, as AI data centers don’t just need super-fast memory attached to GPUs. They also need huge amounts of storage to hold data, models, prompts, context, outputs, and workloads.

That is why data center SSD revenue soared in the quarter. This means that AI demand now spans high-value DRAM, HBM, and NAND-based SSD storage across the full AI server and cloud infrastructure stack. Essentially, Micron claims that memory performance and capacity are not just critical for the GPUs but also for ASICs (custom AI chips) and CPUs. So this means the AI opportunity is much bigger for Micron even years from now compared to what was earlier anticipated.

Micron argued that customer agreements, extraordinary pricing gains, data center momentum, and tightening industry supply all support the idea that this AI boom may have far more staying power than investors once assumed.

Why Investors Suddenly Have More Reason to Believe This AI Boom Can Last

To summarize, Micron’s Q3 was much more than just staggering sales and earnings growth. It showed investors what this AI-era memory leader looks like when demand is expanding while supply is constrained and customers are signing multi-year contracts backed by meaningful cash commitments. The company has now guided to $50 billion in revenue for the next quarter. For the full fiscal year, analysts predict revenue climbing by 246% to $129 billion, followed by earnings growth of 784% to $73.31. In fiscal 2027, revenue and earnings are expected to increase by 70% and 86%, respectively.

The AI boom has been greatly beneficial for Micron. While memory has always been a cyclical industry, this quarter showed that Micron could be a more durable, visible, and structurally attractive business than the market once believed. This is why investors are pouring money into the stock, as they have a new reason to believe this AI memory boom has staying power.

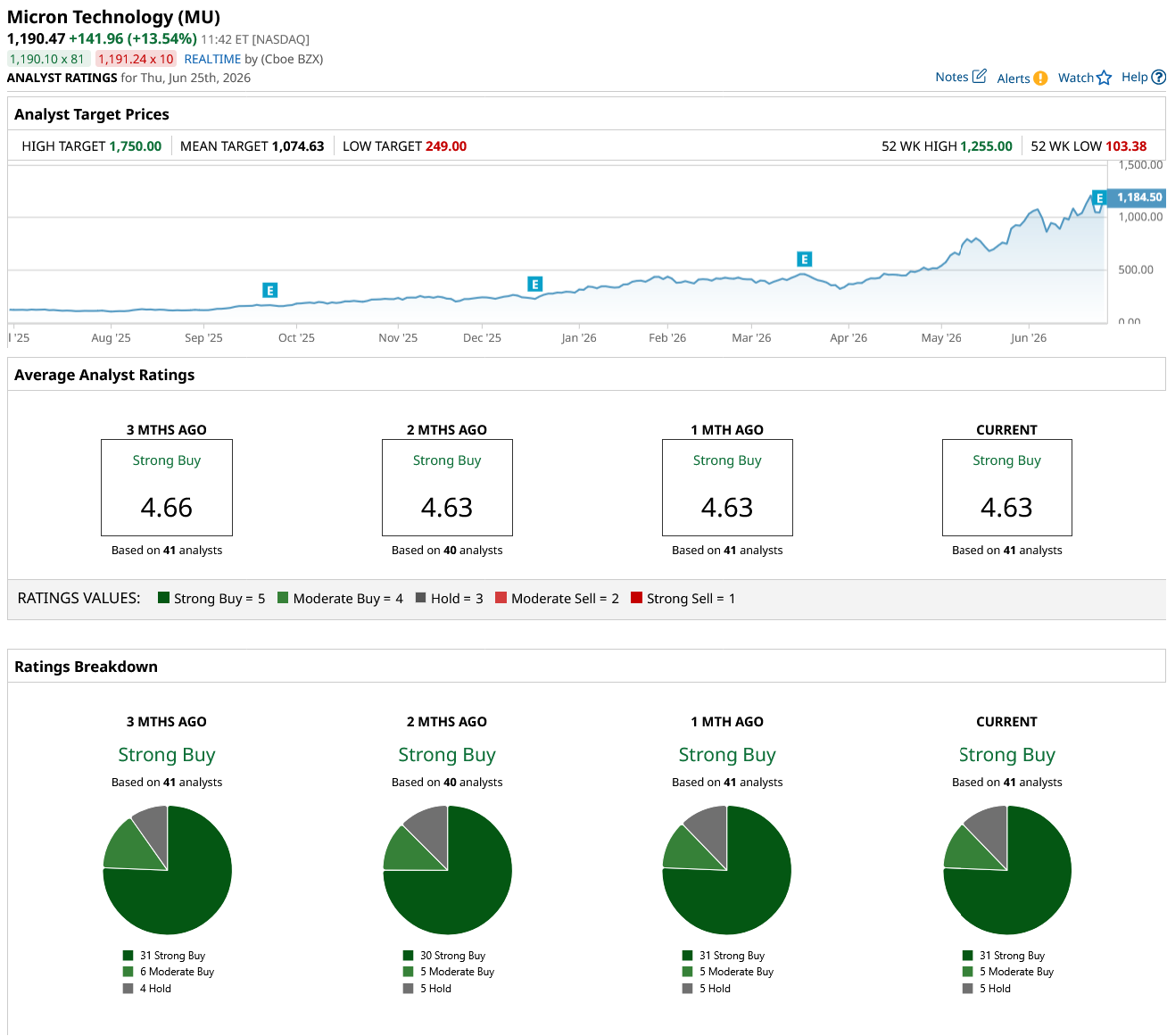

Finally, Wall Street also remains strongly bullish about MU stock. Out of the 41 analysts covering MU, 31 rate it a “Strong Buy,” five rate it a “Moderate Buy,” and five recommend a “Hold.” The stock has soared an impressive 315% year-to-date (YTD) and is trading above its average target price of $1,074.63. But the high price target of $1,750 suggests MU stock has an upside potential of 47% from current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)