/Solventum%20Corp-%20healthcare%20phone-by%20ipopba%20via%20iStock.jpg)

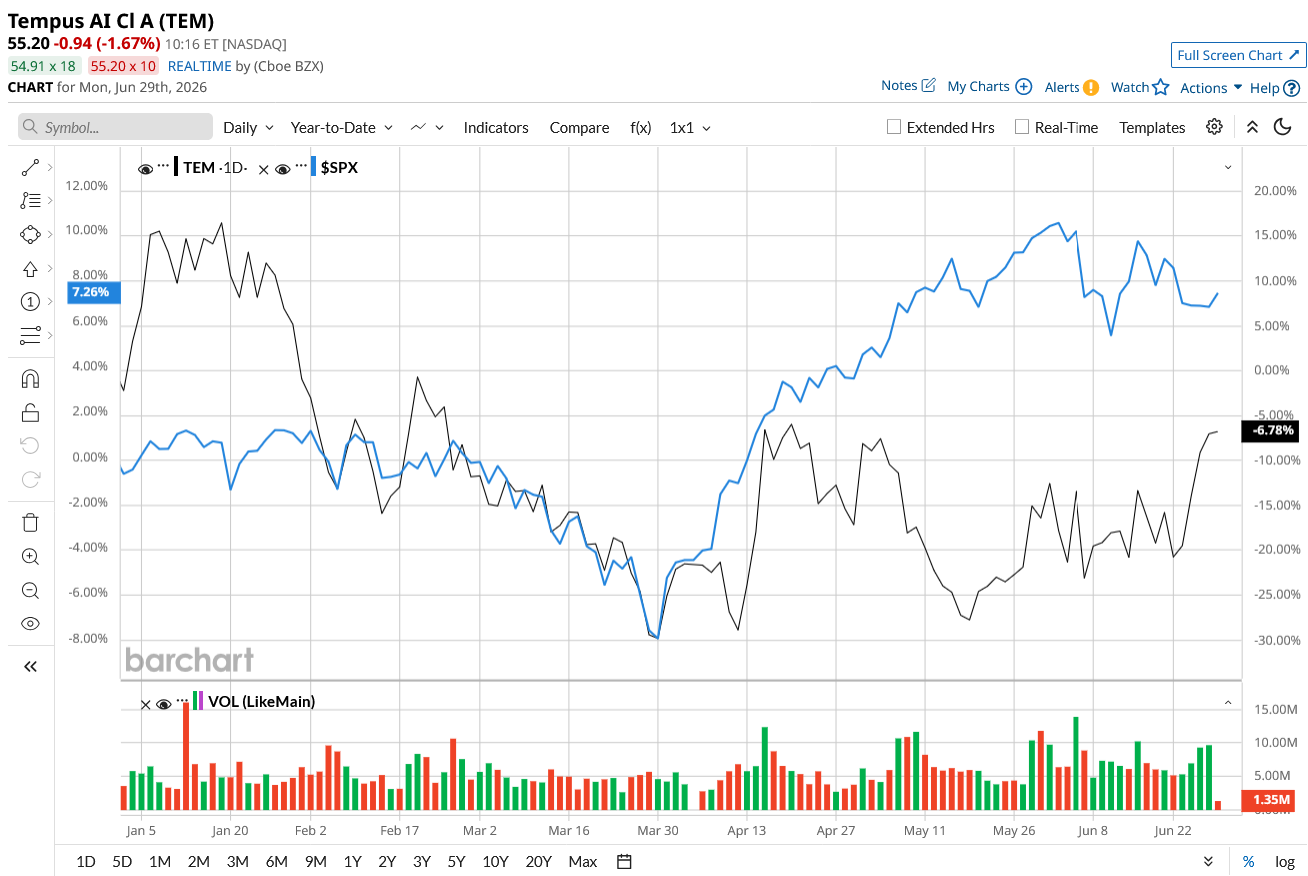

Tempus AI (TEM) may be building one of healthcare's fastest-growing artificial intelligence (AI) platforms, but the stock hasn’t given investors much to celebrate lately. Shares are down roughly 15% over the past year and about 4% year-to-date (YTD), even as the company continues to report strong revenue growth and expand its footprint in AI-powered precision medicine. TEM stock even has an approximately 4% weightage in Cathie Wood’s ARK Invest ETFs (ARKG) (ARKK). With the stock pulling back while the fundamentals continue improving, investors are left with a critical choice.

Does this pullback represent a buying opportunity or a warning sign?

Why Tempus AI Stands Out

Previously, diagnostic companies cared mostly about selling more tests, improving reimbursement, and expanding laboratory operations. However, when generative AI entered the picture, it changed how investors viewed diagnostic companies. These companies now build massive proprietary datasets using AI. Collectively, millions of patient records have now become an incredibly valuable training dataset for AI models.

Valued at $10 billion, Tempus AI is a mid-cap precision medicine and healthcare AI company that combines genomic testing, clinical data, and AI to help doctors make better treatment decisions and help pharmaceutical companies develop drugs faster. Diagnostic testing remains the largest part of its business, where it generates most of its revenue. Its advanced laboratory tests include solid tumor genomic profiling, liquid biopsy, hereditary genetic testing, and rare disease testing, among others.

But what specifically makes it stand out is that every diagnostic test generates valuable molecular and clinical data with the help of AI. Tempus then licenses this de-identified data to pharmaceutical and biotech companies on multi-year contracts. This is probably why Tempus AI is now valued as a healthcare data and AI platform rather than just a traditional diagnostic company.

Business Is Getting Stronger, Not Weaker

While Tempus AI's stock performance might indicate that the business is getting weaker, the reality is quite the opposite. In the most recent first quarter, revenue grew 36% year-over-year (YoY) to $348.1 million. Its diagnostics business revenue grew 35% YoY to $261.1 million. Oncology, in particular, was the growth engine, with solid tumor testing and liquid biopsy services receiving widespread support. Management believes Tempus’ technology platform will allow it to outgrow competitors as physicians increasingly rely on its integrated workflow and decision-support capabilities.

However, data and AI are driving the true growth story. Its Data and Applications business generated $87 million in revenue, an increase of 40.5% YoY. Within that segment, Insights, Tempus' data licensing and AI modeling business, expanded more than 44%. This quarter marked the third consecutive quarter in which Tempus generated more than $100 million in bookings. Big pharma companies like Merck (MRK), AstraZeneca (AZN), Gilead Sciences (GILD), GSK (GSK), and Bristol Myers Squibb (BMY) are collaborating with Tempus AI. The company now has around $100 million-plus multi-year strategic agreements, as companies are now building proprietary AI models directly on Tempus' platform. This growing visibility matters because this segment generates higher margins and more predictable recurring revenue than diagnostics alone.

The main reason these companies are choosing Tempus AI is that it now holds more than 500 petabytes of connected clinical and molecular data. Interestingly, these million-dollar opportunities are just in the U.S. alone, so international expansion remains an untapped opportunity for the company. Essentially, Tempus entered 2026 with roughly $350 million of total contract value (TCV), showing investors what the future revenue picture looks like.

Profitability Is Finally Moving in the Right Direction

Perhaps one reason investors have dumped TEM stock is that profitability remained a growing concern. The company reported a net loss of $125.9 million in the quarter. However, adjusted EBITDA has improved every quarter for five to eight consecutive quarters on a YoY basis. In Q1, adjusted EBITDA loss narrowed to $2.8 million compared to $16.2 million in the prior quarter.

Management is confident of generating positive adjusted EBITDA of $65 million in 2026. According to consensus estimates, full-year revenue will increase by 25.3% YoY to $1.6 billion, followed by $1.95 billion in 2027, another 22.2% increase. Despite those growth expectations, the stock currently trades at 6.18 times forward sales, which is reasonable. If Tempus continues growing revenue at this pace or higher while translating its expanding AI ecosystem into sustained profitability, buying TEM stock at the dip now could eventually work in investors’ favor.

What Does Wall Street Say About TEM Stock?

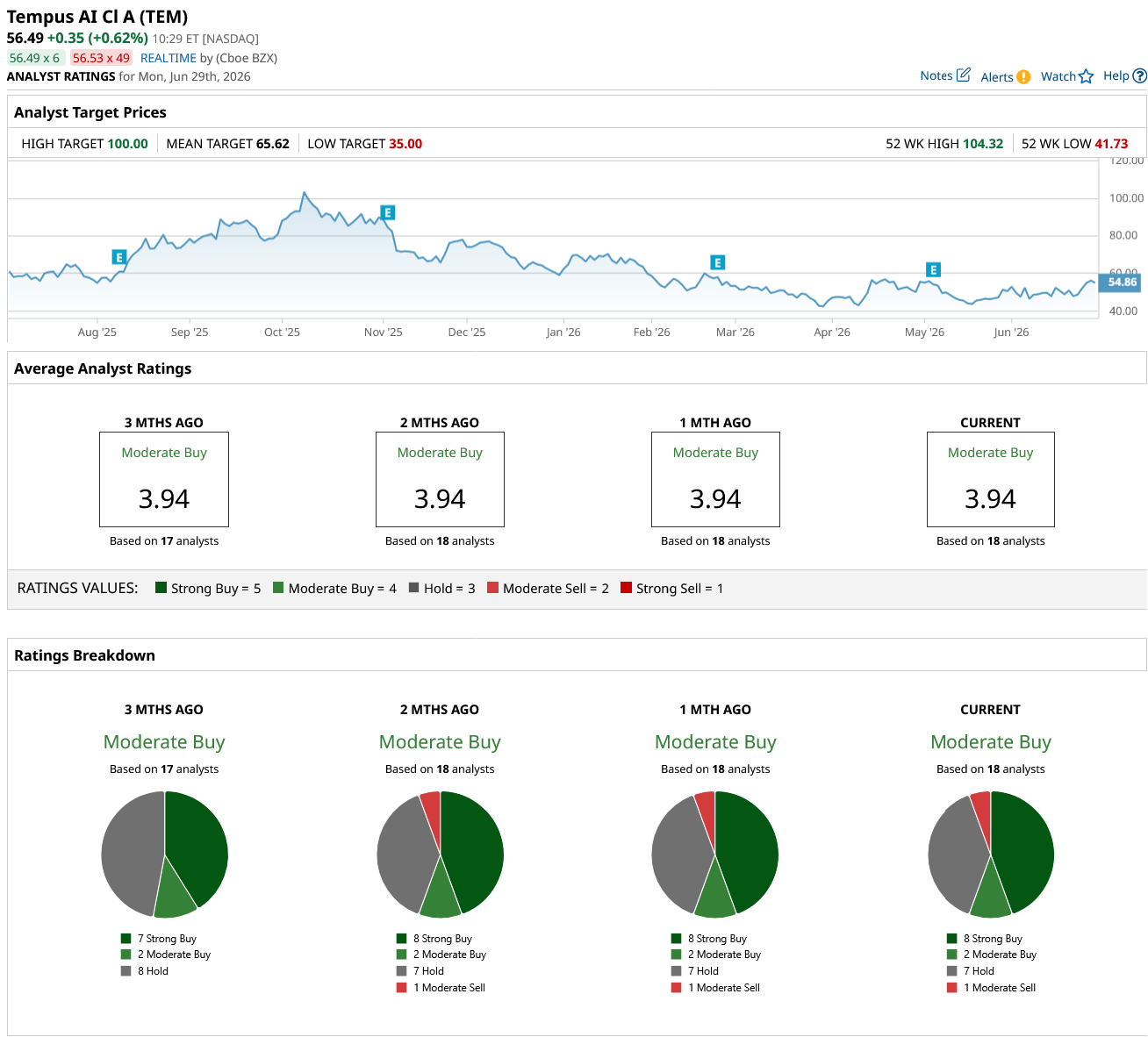

Overall, Wall Street remains moderately bullish about Tempus AI. Among the 18 analysts covering the company, eight give it a "Strong Buy" rating, two recommend a "Moderate Buy," seven suggest holding, and one says it is a “Moderate Sell.” While TEM stock is down roughly 4% so far this year, analysts see potential upside of 16% from current levels if it hits its average price target of $65.62. Plus, the high price target of $100 implies the stock could surge by as much as 76% over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)