/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

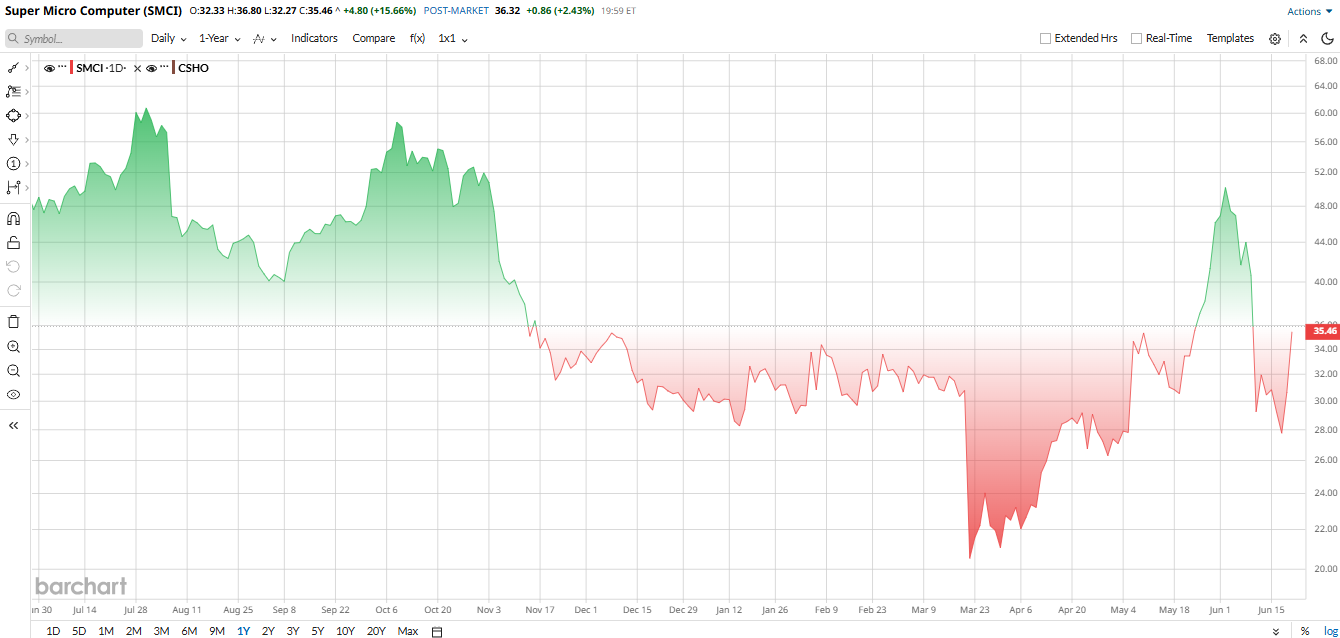

Supermicro (SMCI) just got a fresh jolt from Wall Street. GF Securities recently upgraded the stock to a “Buy” and slapped on a $48 target. SMCI stock jumped about 16% on the news. That kind of move tells you two things at once. Traders still want the AI server story, and they still believe this name can squeeze out more upside. The harder question is what will happen after the first pop. Earnings are close, expectations are high, and Supermicro stock has already had a wild run.

Supermicro sits right in the middle of the AI infrastructure trade. It builds high-density servers, storage systems, and liquid-cooled gear for data centers. The company has become a key partner for Nvidia (NVDA)-powered builds, and that keeps it tied to one of the hottest capital spending cycles in tech. But this is also a stock with baggage. That mix is why every upgrade matters.

Supermicro Stock Sees Wild Swings

SMCI stock has been all over the map in 2026. Even after a recent pullback, the stock is still up about 11% year-to-date (YTD). Despite this, shares are down about 24% over the past 12 months. That tells the story pretty well. Big swings. Big expectations. Big debate.

The positives are easy to see. Supermicro is still plugged into AI demand, and the market liked its latest product push tied to Nvidia’s Vera Rubin NVL4 platform. The negatives are just as clear. In June, the company's $7 billion financing plan spooked investors because of dilution risk, even though management said the money would help fund roughly $39 billion of AI orders. That is classic Supermicro — great growth, real execution risk, big moves in both directions.

On earnings, SMCI stock does not look expensive. Barchart shows a forward price-to-earnings (P/E) multiple of 16.7 times for Supermicro, compared with 16.7 times for Hewlett Packard Enterprise (HPE) and 23.7 times for Dell Technologies (DELL). That puts the stock below Dell and roughly in line with the broader hardware pack. So the market is not pricing in perfection here. It is pricing in a strong cycle with some risk attached.

That said, the stock is not a clean bargain, either. With a fast-rising AI backlog, a lot of the good news is already known. The valuation says investors are paying for growth. It does not say the upside is unlimited.

Supermicro Topped the Earnings Estimate, Yet Missed on Revenue

Supermicro’s fiscal third quarter was strong overall. Revenue hit $10.2 billion, up from $4.6 billion a year earlier, yet missed analysts' estimate by $2.2 billion. Net income rose to $483 million from $109 million in the prior-year period. EPS came in at $0.84, well ahead of the $0.62 that Wall Street expected. The company also reported cash flow used in operations of $6.6 billion, while cash and cash equivalents were $1.3 billion at quarter's end.

Management also provided a strong outlook. For Q4, Supermicro guided for revenue of $11 billion to $12.5 billion and non-GAAP EPS of $0.65 to $0.79. For fiscal 2026, the firm expects revenue of $38.9 billion to $40.4 billion. “Supermicro's transformation into a total datacenter infrastructure provider is accelerating,” said CEO Charles Liang, adding that the company’s new U.S. facilities leave it well-positioned for AI demand.

Supermicro Expands Its AI Reach

This is not just a one-day analyst story. Supermicro continues to push into more AI infrastructure work. The firm announced its $7 billion financing plan to support the purchase of components for AI orders. In May, it signed a memorandum of understanding (MOU) with NANO Nuclear Energy (NNE) to explore microreactor integration for AI data-center systems. On top of that, GF Securities pointed to Supermicro’s SpaceX (SPCX) link as a possible opening in the neocloud market.

These are small headlines on their own. Together, they show management is trying to widen the company’s footprint while demand is hot.

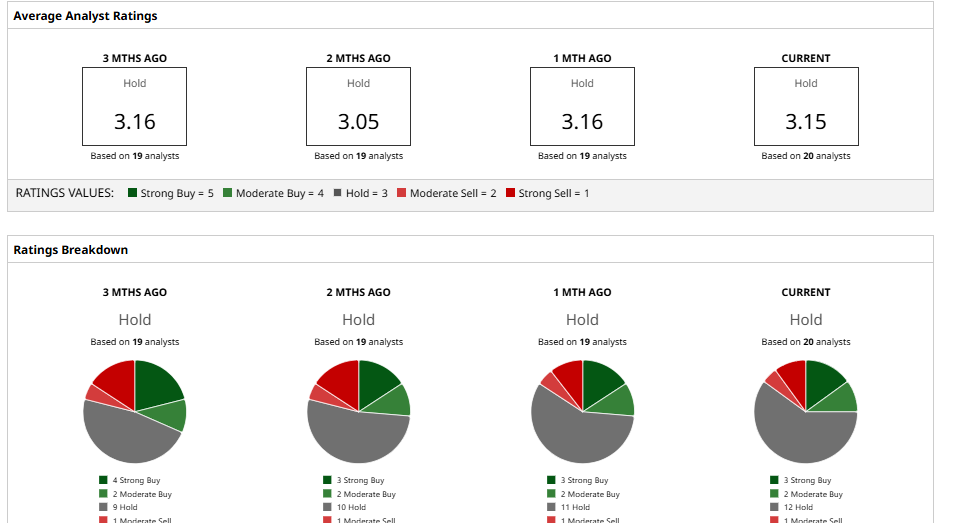

What Do Analysts Think of SMCI Stock?

The analyst community is mostly bullish, but with varied price targets. Citi and JPMorgan hiked their targets after the Q3 results. Outside of that, Raymond James recently dropped its target to $39 from $45, while Rosenblatt upped its target to $40 in May. Mizuho has SMCI stock at around $44 with a “Neutral” rating, and CJS Securities has a “Market Perform” rating after an upgrade. Meanwhile, Wedbush has a “Neutral” stance and believes that much of the upside has already occurred with SMCI stock.

Overall, Supermicro has a consensus “Hold” rating. The mean price target of $35.87 implies about 11% potential upside from here. In plain terms, some analysts see room to run, but not without risk.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)