/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

The semiconductor industry rarely offers an easy trade. But Wedbush may have pointed to a real opening for United Microelectronics (UMC).

The idea floated by Wedbush is simple. As geopolitical risk pushes chip buyers to spread out supply, more companies want older chips made in safer, more reliable locations. UMC already has factories in Singapore, Japan, and other markets, which puts it in a strong spot.

If TSMC (TSM) moves some mature-node work outside Taiwan, designers will need another source. UMC could be one of the clearest options.

It does not need to beat TSMC on advanced chips. It only needs to serve the older, essential parts that power cars, factory systems and edge devices.

That is where the upside could come from. These chips matter more than ever when supply gets tight. If some of TSMC’s work shifts away, UMC may be ready to absorb the demand.

Meet the Underdog UMC

United Microelectronics is no scrappy startup. It’s Taiwan’s second largest semiconductor foundry, cranking out millions of chips on mature nodes from 28 nanometers to 90 nanometers. While TSMC grabbed headlines with 3 nanometer wizardry, UMC quietly became the go to shop for automakers, industrial giants, and Internet of Things (IoT) chip designers who prize reliability over cutting-edge shrink. It’s the steady factory in the background.

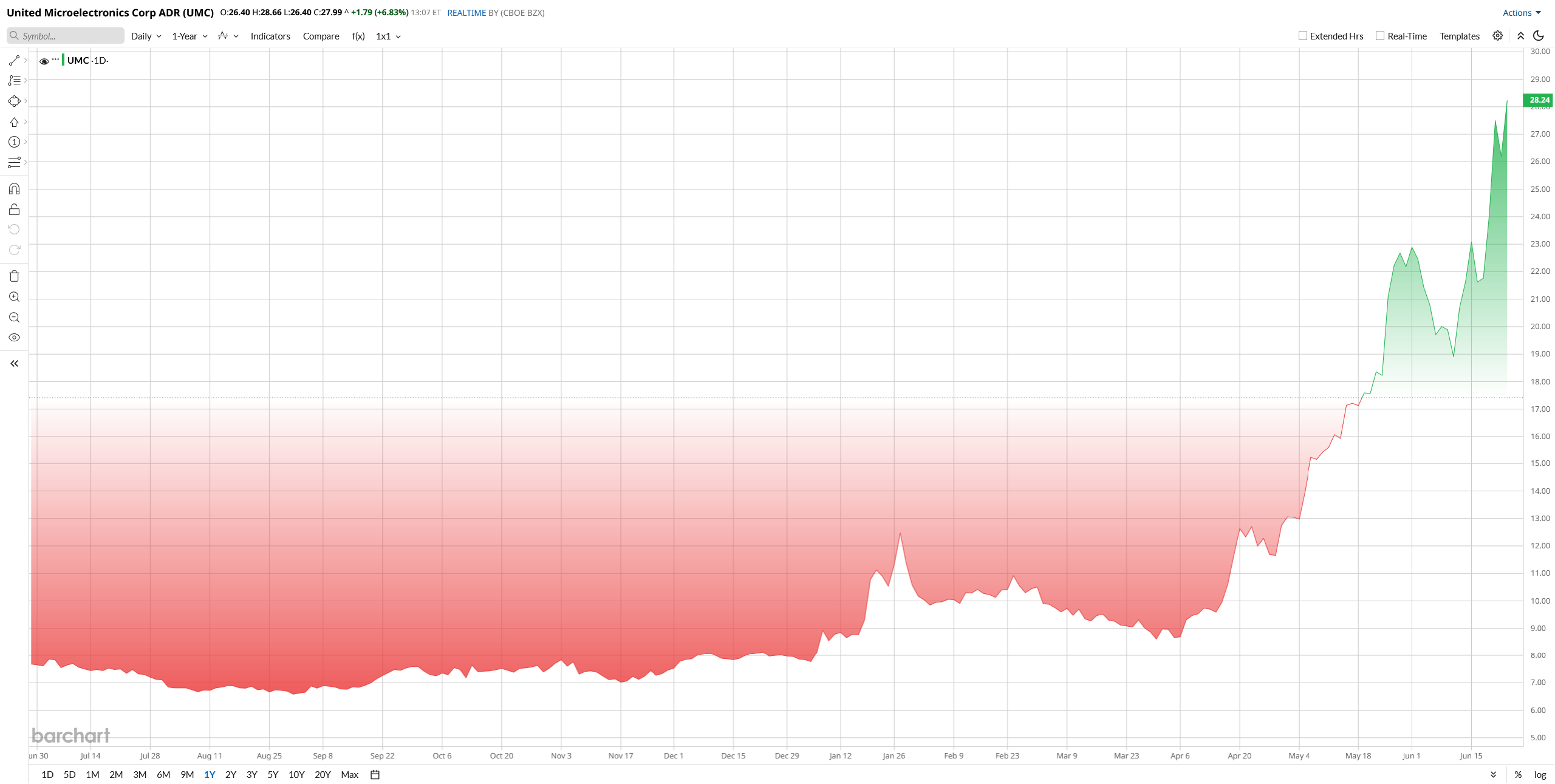

Shares of UMC have delivered more than a respectable ride. Over the past year, the stock climbed roughly 263% and the last five days alone have seen a 30% increase. The advance was fueled by a recovering chip cycle, a surge in edge AI device orders, and that budding TSMC relocation chatter. On the flip side, worries about weak smartphone demand and overcapacity from aggressive Chinese fabs occasionally knocked the wind out of the rally. Still, the broader trend has been friendly.

UMC Delivers Solid Q1 Growth as Mature Nodes Drive Demand

The most recent results, covering the first quarter of 2026, show a UMC in firm control of its trajectory. Revenue hit $1.93 billion, up 7% from the same period a year earlier. The wafer fabrication business splits neatly. The 22 and 28 nanometer segment contributed roughly 36% of total sales, while the 40 nanometer and above chunk constituted the rest. That high mix of proven, profitable nodes is precisely where industrial and automotive demand lives.

Net income surged to $511 million, a 10% year-over-year (YoY) jump. Free cash flow remained robust at $210 million, giving management plenty of dry powder. Cash and equivalents stood at a fortress-like $3.44 billion.

During the earnings call, CEO Jason Wang struck a confident tone. He said, “Our mature node utilization is firming up faster than many expected, and we are seeing a genuine pull from edge AI and automotive chip designers who want supply chain resilience, not just transistors.”

The guidance was equally steady. Management expects second quarter revenue to rise mid single digits sequentially. For the full year they forecast high single digit revenue growth. Analysts, on average, project full-year revenue of $7.9 billion and adjusted earnings per ADR of $0.70, in line with the company’s upbeat posture.

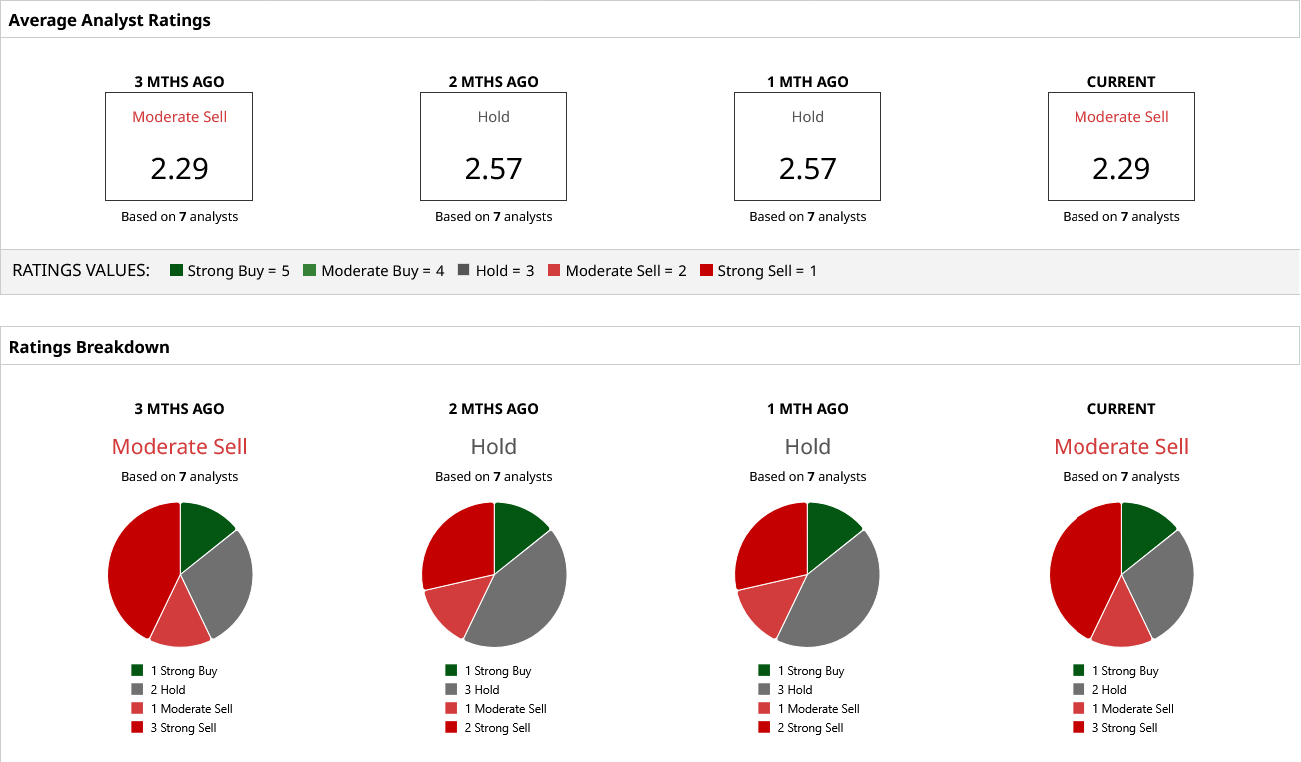

What the Street Is Saying About UMC Stock

Analyst sentiment paints a picture of cautious optimism. Wedbush rates UMC stock “Outperform” with a $12 price target, arguing the relocation dynamic isn’t priced in. Morgan Stanley’s team is more measured but still constructive. The bank's analyst noted, “UMC is an underappreciated play on the reshoring of mature semiconductor supply chains, but we need a clear catalyst.” They carry an “Overweight” rating and a $11 target. Goldman Sachs is the sober voice, maintaining a “Neutral” stance and a $9.50 target. Their comment was blunt: “The thesis is interesting, but timing is everything and relocation moves slowly.”

Needham rounds out the group with a “Buy” rating and a $10 target. The consensus rating according to Barchart comes in as a “Moderate Sell.” The average price target sits at $11, implying more than 60% downside from recent levels. The Street is curious but not yet fully convinced, which is undoubtedly when disciplined long-term investors get interested.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)