/Amazon%20box%20delivery%20by%20Tumisu%20via%20Pixabay.jpg)

Amazon (AMZN) is heading into Prime Day with a simple problem and a simple opportunity. The problem is that investors still worry about big AI spending, slower consumer demand, and whether all of this infrastructure will pay off fast enough. The opportunity is that Prime Day gives Amazon a clean read on shopper demand right when the company wants to show that its retail machine, ads business, and cloud platform are still firing together.

This year’s event runs from June 23 to June 26, and Amazon is also using the moment to push its new Alexa for Shopping tool, which could make Prime Day more than just a sales event. It could become a test of how much AI can help Amazon sell.

Abput Amazon Stock

Amazon is still the rare company that can sell paper towels, cloud computing, ads, groceries, and satellite internet in the same breath. That is why AMZN stock never stays in one box for long. It is both a consumer story and a tech story. It is also a margin story now, because the market wants to know how much profit Amazon can squeeze out of Amazon Web Services (AWS), advertising, and automation while it keeps spending on the next wave of growth.

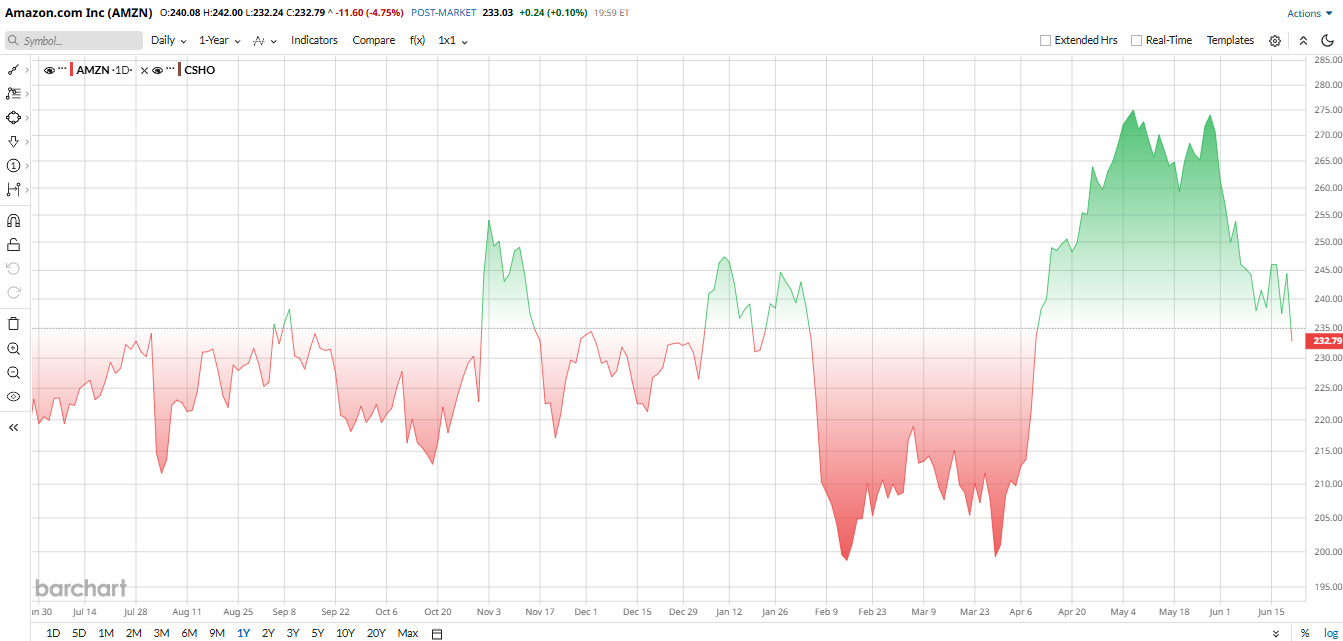

AMZN stock has been choppy in 2026, but not weak in any lasting sense. The stock was up 9% for the year back in April before the market started worrying more about the company's huge $200 billion capex plan. Since the May peak, shares have fallen about 16%, most recently sustaining a nearly 5% drop ahead of Prime Day on June 22. That wiped out the year-to-date (YTD) gains, with AMZN stock now up just 2% in 2026.

The valuation of Amazon is not cheap, but it is not absurd either. Amazon stock now trades at about 30 times forward earnings, which is well below its five-year average of around 45 times. Another useful read is Amazon's PEG ratio of 1.7 times, which is below the 1.9 median for a basket of Big Tech and retail peers. So, AMZN stock still commands a premium, but not the kind of premium that usually comes with a company in trouble. It looks more like a quality name with a multiple that is still rich but no longer running away.

Prime Day Is the Near-Term Catalyst

Prime Day is the near-term story for Amazon, but the bigger point is what it says about demand. Adobe Analytics expects record online spending of $26.3 billion across the four-day event, and eMarketer thinks Amazon will capture about 60% of that figure. Investors like that because Prime Day can lift sales, ad clicks, and membership value all at once.

The catch is timing. By moving the event into June, Amazon is pulling some demand into the second quarter, which should help Q2 revenue but make comparisons a little messy later in the year. That is why the stock reaction has been mixed. Traders like the setup, but they also know this event needs to hit.

The Latest Quarter Shows Both Muscle and Pressure

Amazon’s Q1 was strong on the top line. Revenue rose 17% to $181.5 billion. North America sales climbed to $104.1 billion, International sales reached $39.8 billion, and AWS jumped 28% year-over-year (YOY) to $37.6 billion. Operating income came in at $23.9 billion, while net income rose to $30.3 billion, or $2.78 per diluted share.

Amazon also had $101.8 billion in cash and cash equivalents at quarter-end, with $1.2 billion in free cash flow over the trailing 12 months after all the AI spending.

The headline number was good, but the real message came from management. CEO Andy Jassy noted that AWS grew 28%, the chips business topped a $20 billion revenue run rate, and that advertising was running at more than $70 billion in trailing 12-month revenue. Jassy also said that Amazon is in the middle of some of the “biggest inflections” of its lifetime.

For Q2, Amazon guided for sales of $194 billion to $199 billion and operating income of $20 billion to $24 billion. Wall Street has not been shy about liking the setup, with Prime Day now folded into the forecast.

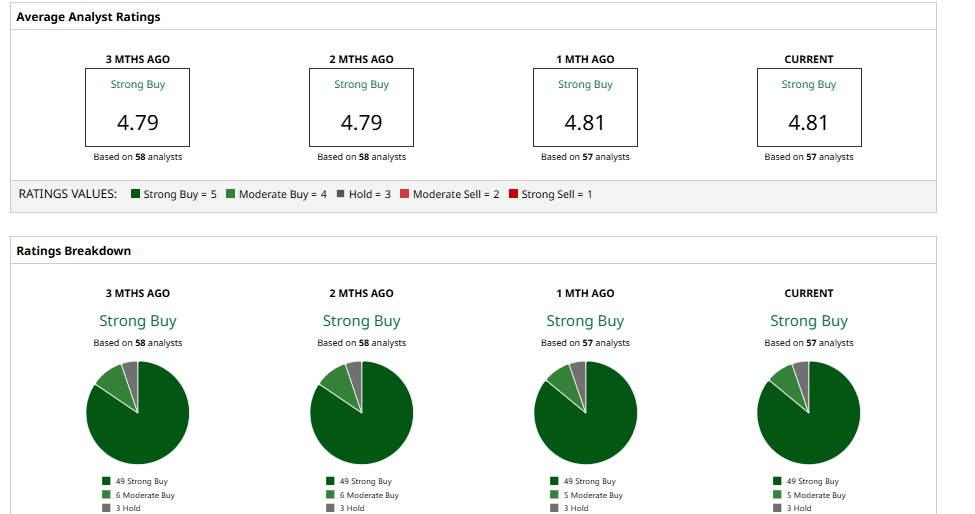

What Does Wall Street Think of AMZN Stock?

Analysts are still mostly on the bull side. In April, KeyBanc raised its price target to $325 from $285 and said that AWS, grocery demand, and Amazon Leo could keep the story moving. Meanwhile, Morgan Stanley has called Amazon its top internet pick, pointing to AI and AWS as key upside drivers. BofA has also remained constructive, saying the company’s AI shopping tools and cloud momentum could keep conversion and growth moving higher.

At the same time, Wedbush has argued that Amazon can still break out in 2026 thanks to automation, ads, and AWS re-acceleration. The common thread is simple. Analysts are less worried about Prime Day itself and more concerned about what it proves about the rest of Amazon’s engine.

Overall, AMZN stock has a consensus “Strong Buy” rating. The average price target at $316.04 suggests potential upside of 35% from here.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)