The cryptocurrency market is approaching a potentially pivotal moment, and investors in Coinbase Global (COIN) are watching July 17 closely. The U.S. Congress has scheduled a key hearing on the CLARITY Act, a proposed framework aimed at creating clearer rules for the digital asset industry. The legislation could become a major catalyst for the crypto sector by addressing long-standing regulatory uncertainty around market structure, asset classification, and oversight. Coinbase has emerged as a strong supporter of the bill, arguing that clearer regulation could help foster innovation and strengthen the U.S. digital asset ecosystem.

The bill aims to divide oversight of digital assets between the CFTC and SEC, creating a regulatory framework for cryptocurrencies such as Bitcoin (BTCUSD), Ethereum (ETHUSD), Solana (SOLUSD), and XRP (XRP). While the legislation has progressed through Congress, it still faces major challenges, including gaining Senate support, resolving differences between committee versions, and securing final approval.

A favorable regulatory environment may reduce compliance uncertainty, encourage greater institutional participation, and provide a clearer path for expanding crypto-related products and services. As the industry waits for lawmakers’ next move, July 17 could become a defining date for Coinbase and the broader future of cryptocurrency regulation in the U.S.

About Coinbase Stock

Coinbase Global is one of the world’s largest cryptocurrency platforms, providing a secure infrastructure for buying, selling, storing, and managing digital assets. Founded in 2012 and headquartered in San Francisco, California, Coinbase serves retail users, institutions, and developers through its crypto exchange, custody services, staking products, stablecoin ecosystem, and blockchain infrastructure solutions.

The company has expanded beyond traditional crypto trading by building a broader digital asset financial platform, aiming to become a leading gateway for the global crypto economy. Coinbase has a market cap of $41.67 billion.

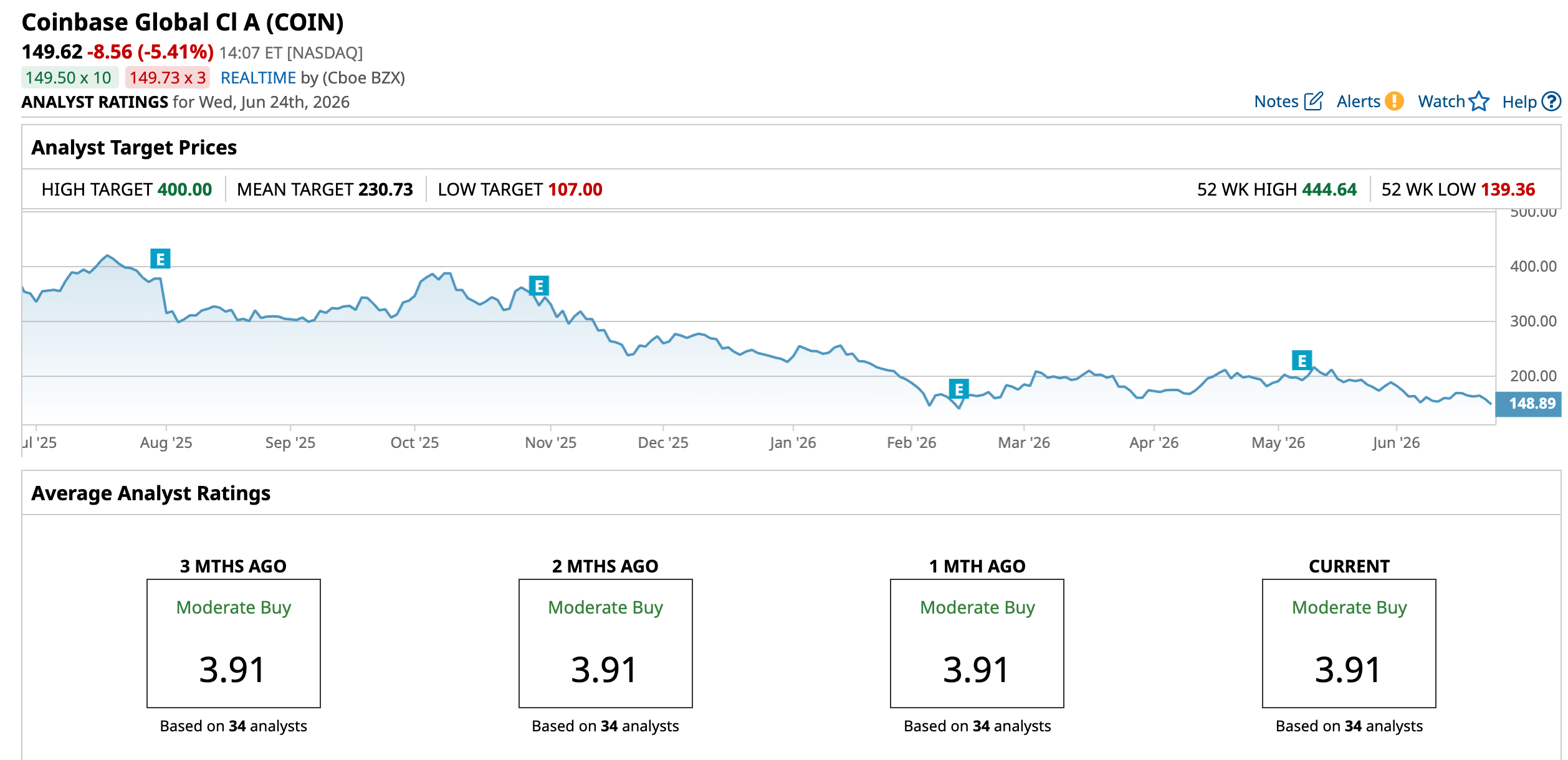

Coinbase Global shares have faced significant pressure over the past year as investors reassess the outlook for cryptocurrency trading activity, market volatility, and the company’s near-term earnings trajectory. The stock has declined 56.57% over the past 12 months and has remained under pressure in 2026, falling 33.78%, as concerns over weaker crypto volumes and a challenging operating environment weighed on sentiment. It is currently trading 66.1% below its 52-week high of $444.64 reached last July.

Despite the near-term weakness, investors continue to watch potential catalysts, including improving crypto market conditions and regulatory developments such as the CLARITY Act, which could provide greater certainty for the digital asset industry. Supporters believe clearer rules could benefit Coinbase by strengthening institutional adoption and expanding opportunities beyond traditional crypto trading.

Despite the weak momentum, the stock still seems to be trading at a lofty valuation at 94.81 times forward price-to-earnings.

Mixed Q1 Performance

Coinbase Global reported its first-quarter 2026 financial results on May 7. Revenue came in at $1.4 billion, down 31% year-over-year (YOY). The company posted a net loss of $394.1 million, compared with net income of $65.6 million in the year-ago quarter. Adjusted EPS declined sharply to a loss of $1.49 per share versus earnings of $0.24 per share in Q1 2025.

The weakness was primarily driven by lower transaction activity, which remains Coinbase’s largest revenue source. Transaction revenue fell to $756 million, down about 40% YOY, as cryptocurrency trading volumes and market activity softened. Subscription and services revenue also declined to $584 million, a 14% YOY decrease from the prior-year period.

Despite the earnings pressure, Coinbase highlighted several operational strengths. Crypto trading market share reached a record 8.6%, while derivatives trading volume increased significantly, with trailing-twelve-month derivatives volume up 169% YOY. On the other hand, adjusted EBITDA remained positive at $303.3 million, although it declined from $929.9 million in Q1 2025, reflecting the impact of lower revenue and higher operating costs.

Moreover, Coinbase provided a cautious but constructive outlook. For Q2 2026, management guided subscription and services revenue to approximately $565 million to $645 million and expects adjusted operating expenses of $820 million to $870 million. For the full-year 2026, the company expects adjusted operating expenses of approximately $4.3 billion to $4.6 billion.

Analysts expect the company’s EPS to decline 56.8% YOY to $1.74 in fiscal 2026 and rise 175.3% to $4.79 in fiscal 2027.

What Do Analysts Expect for Coinbase Stock?

Earlier this month, Cantor Fitzgerald reiterated an “Overweight” rating on Coinbase after the company announced plans to launch tokenized U.S. stocks, allowing users to gain blockchain-based exposure to equities, including potential dividend benefits.

Also, Benchmark reiterated a “Buy” rating and set a $270 price target on Coinbase after the company’s latest System Update event, highlighting its strategy to build an “Everything Exchange.”

Meanwhile, KeyBanc maintained a “Sector Weight” rating and $169 price target on Coinbase.

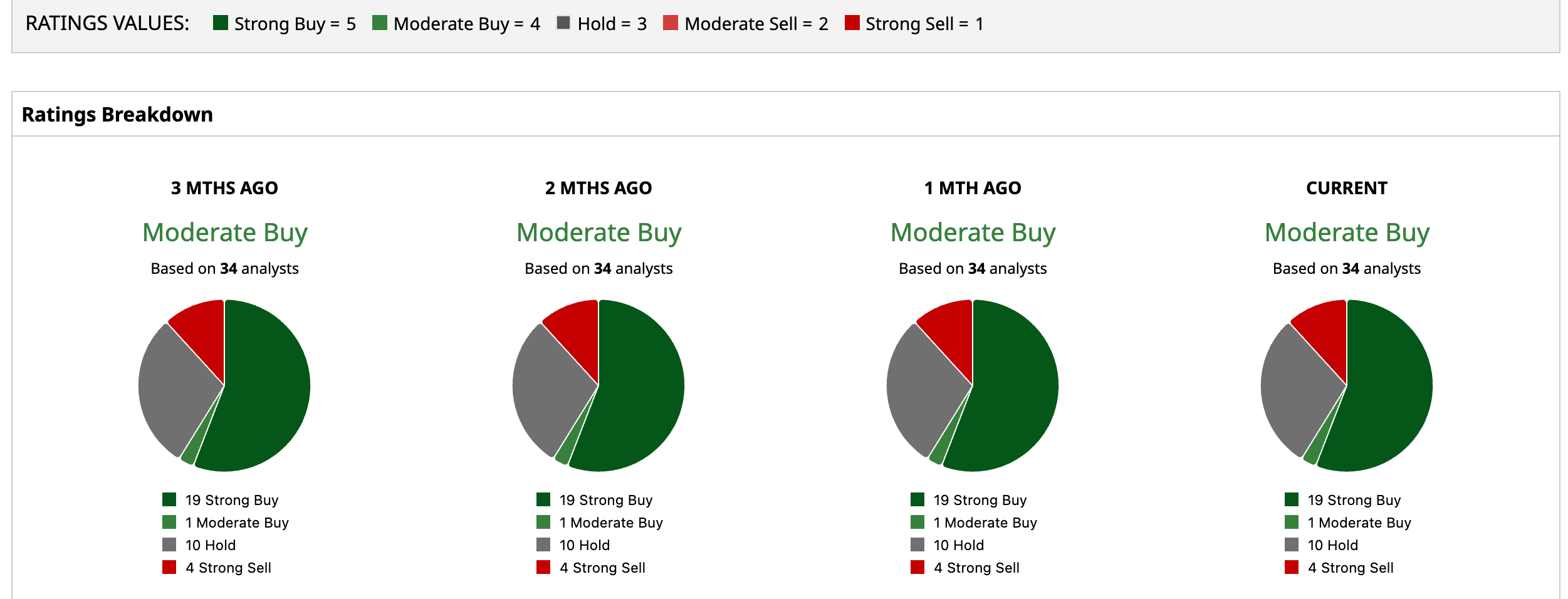

Overall, COIN has a consensus “Moderate Buy” rating. Of the 34 analysts covering the stock, 19 advise a “Strong Buy,” one gives a “Moderate Buy,” 10 recommend a “Hold,” and four analysts offer a “Strong Sell” rating.

While the average analyst price target of $230.73 indicates an upside potential of 54.2%, the Street-high target price of $400 suggests that the stock could rally as much as 167.3%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.