/Automation%20machine%20equipment%20quality%20testing%20circuit%20board%20by%20zyabich%20via%20Adobe%20Stock.jpeg)

In the last 52-weeks, any business remotely connected to artificial intelligence has skyrocketed. Of course, there are strong reasons that back the rally and structural tailwinds are likely to ensure that the positive momentum sustains.

Amidst this positivity, Qualcomm (QCOM) is among the few technology names that has been relatively subdued. However, as the company pursues innovation driven organic growth and potential acquisitions, it might not be long before QCOM stock surges.

In today’s news, Qualcomm has agreed to acquire Modular. The latter is a provider of an “AI-native software stack that enables AI to run efficiently across hardware architectures.” This acquisition is likely to boost Qualcomm’s software foundation for its data center strategy. Further, the acquisition enables the company to deliver a silicon-agnostic compute layer, which is likely to improve performance-per-watt and increase hardware flexibility.

It was also recently reported that Qualcomm is in discussion to acquire Tenstorrent for a consideration of $8 to $10 billion. Potential acquisition of the AI chip start-up will be another long-term catalyst for Qualcomm.

About Qualcomm Stock

Headquartered in San Diego, Qualcomm is involved in the development and commercialization of foundational technologies for the wireless industry globally. This includes on-device artificial intelligence, high-performance and low-power computing, and advanced wireless connectivity.

Qualcomm holds intellectual property (including patents) applicable to products that implement cellular technologies (including 4G and 5G). Based on the products and services, Qualcomm has three business segments: QCT (Qualcomm CDMA Technologies), semiconductor business, and QTL (Qualcomm Technology Licensing) licensing business.

For the first half of FY26, Qualcomm reported revenue of $22.9 billion. For the same period, the company reported healthy operating cash flows of $7.4 billion. While Qualcomm reported net debt of $9.4 billion as of Q2 FY26, strong cash flows ensure that the company has a healthy credit profile and ample flexibility for organic and acquisition-driven growth.

Despite some choppy price action this week, in the last six months, QCOM stock has trended higher by 12%. Considering an attractive forward price-earnings ratio of 27.84, the uptrend is likely to sustain.

Growth Acceleration Catalyst

It’s important to note that for the first half of FY26, Qualcomm has delivered muted top-line growth. That’s a key reason for QCOM stock remaining relatively subdued. However, Qualcomm has indicated that “QCT handset revenues from Chinese customers will reach a bottom in the third quarter and return to sequential growth in the following quarter.” This is the first catalyst for an impending rally.

Further, Qualcomm is positioning as an AI infrastructure player beyond handsets. The potential growth areas include wearables, 6G, robotics, data center custom silicon. To put things into perspective, the company is already working on over 40 designs of new AI devices. A recent report also indicates that the company is in talks to provide chip-design services to China's ByteDance.

In the data center segment, Qualcomm expects first shipment of custom silicon to a hyperscaler towards the end of the year. The acquisition of Modular is likely to support the company’s expansion in the data center market. Amidst these positives, it’s a matter of time before QCOM stock witnesses a meaningful rally. Qualcomm has already been creating value through steady dividend growth coupled with aggressive share repurchases.

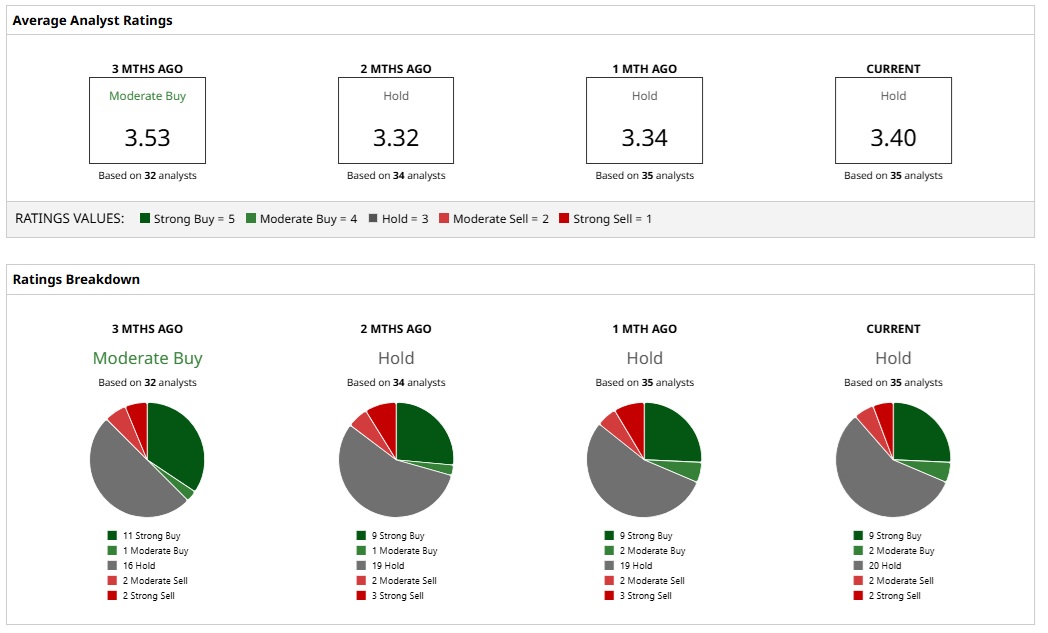

What Do Analysts Say About QCOM Stock?

Based on 35 analysts with coverage, QCOM stock has a consensus “Hold” rating. While nine analysts have a “Strong Buy” rating for QCOM stock, two have a “Moderate Buy,” and 20 have a “Hold” rating. Among the bears, two analysts have a “Moderate Sell” with another two having a “Strong Sell” rating.

The mean price target of $188.97 represents a potential downside of 3.1% from current levels. However, the most bullish price target of $300 suggests that QCOM could climb as much as 54% from here.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)