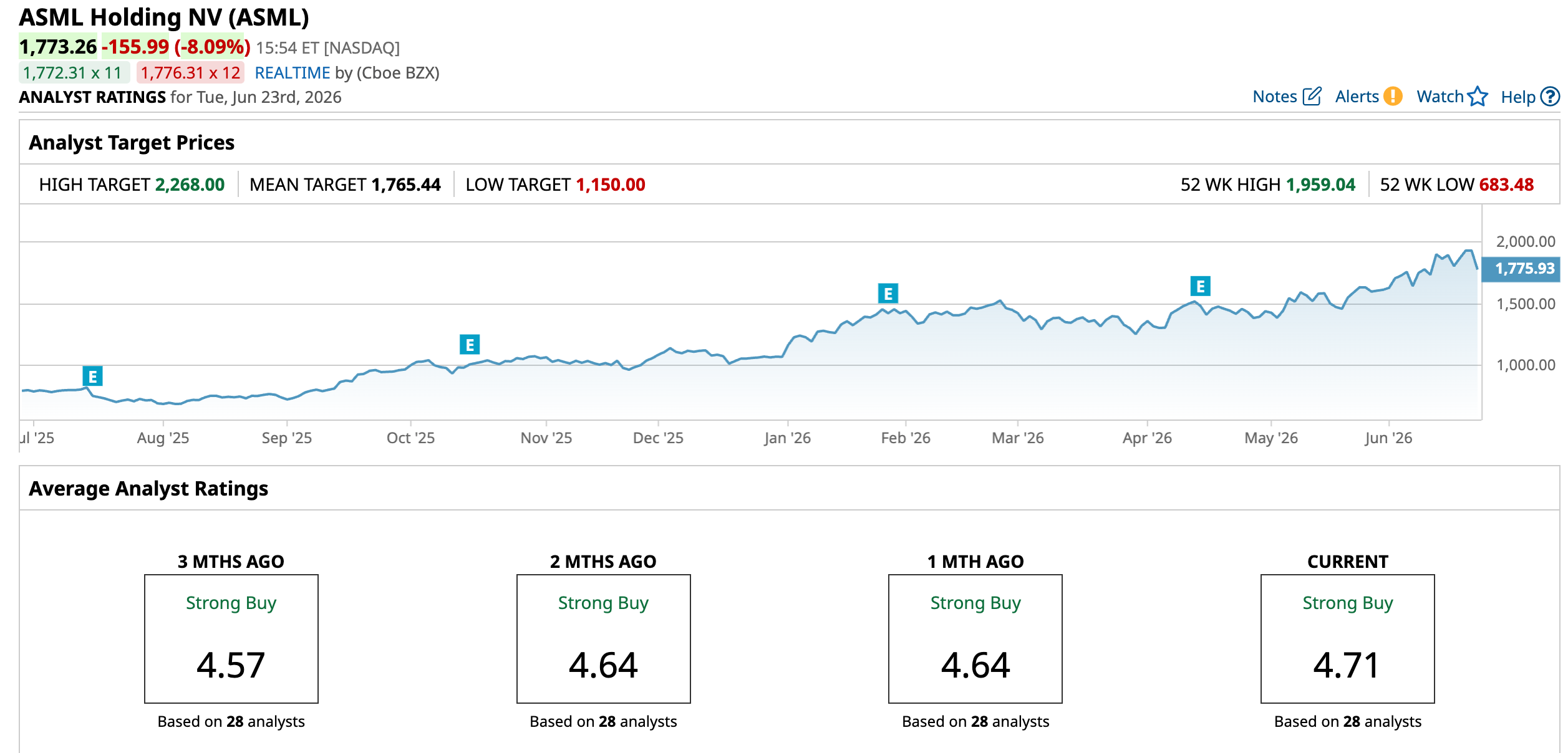

After watching faster moving chip names steal the spotlight through much of 2025 and the opening months of 2026, ASML Holding N.V. (ASML) has worked its way back into investors’ good books. The stock touched a fresh 52 week high of $1,959.04 on Monday, June 22 as analysts rolled out higher price targets.

This comes as ASML is scheduled to report its Q2 FY2026 results on Wednesday, July 15 before the opening bell. Among the biggest votes of confidence came from Wells Fargo & Company (WFC). The firm lifted its price target on ASML stock to $2,200 from $1,750 while sticking with its “Overweight” rating.

Analyst Joe Quatrochi expects another solid quarter from chip equipment makers, ASML included. He also raised his 2027 Wafer Fab Equipment forecast to roughly $190 billion from an earlier estimate of about $180 billion. In fact, Wells Fargo boosted its 2028 industry estimate to $216 billion from $191 billion.

Quatrochi and his team believe ASML’s year-to-date (YTD) underperformance has created an attractive catch-up opportunity. They expect ASML to provide a clearer outlook for demand through 2027 across both Extreme Ultraviolet (EUV) and Deep Ultraviolet (DUV) lithography technologies.

He also expects management to reaffirm confidence in its low numerical aperture (NA) production roadmap. Current plans call for at least 60 systems in 2026 and at least 80 systems in 2027, while existing infrastructure already supports an annual capacity of up to 90 systems.

If the targets remain on track, investors could gain greater confidence in ASML’s long-term growth trajectory.

About ASML Holding Stock

Headquartered in the Netherlands city of Veldhoven, ASML Holding N.V. (ASML) ranks among the most important suppliers in the global semiconductor industry. The company develops advanced lithography, metrology, and inspection systems that chipmakers rely on to manufacture increasingly sophisticated semiconductors.

With a market cap of roughly $758.7 billion, ASML sits at the heart of modern chip production. Its EUV systems together with its DUV platforms help customers squeeze more performance and efficiency out of every new generation of chips. The company also earns revenue from software, system upgrades, refurbishment programs, and technical support services.

On the price performance front, ASML stock surged 127% during the past 52 weeks. The rally has gathered even more steam in 2026 with shares climbing 65.46% year-to-date (YTD). A 29.25% gain during the past three months followed by another 18.41% advance over the last month shows the bulls have kept their foot on the gas.

Even after the run, investors continue paying a premium for quality. ASML stock is currently trading at 52.50 times forward adjusted earnings and 16.39 times sales, both above broader industry averages.

Income investors have also enjoyed a steady stream of dividend growth. ASML has increased its dividend for 10 consecutive years. The company currently pays an annual dividend of $8.37 per share, which translates into a yield of 0.39%. Its latest dividend payment came in at $3.17 per share on May 5 for shareholders on record as of April 27.

A Closer Look at ASML Holding’s Q1 Earnings

ASML delivered a strong first quarter on April 15, reporting Q1 FY2026 results that showed demand remains in its corner. Total net sales climbed 13.2% year-over-year (YOY) to €8.8 billion ($10 billion), while gross profit increased 11.1% from the same period last year to €4.6 billion ($5.3 billion).

Gross margin came in at 53%, landing at the upper end of management's guidance range and hitting the mark with room to spare. The company carried that momentum straight down the income statement. Income from operations rose 15.3% from the year ago period to €3.1 billion ($3.6 billion), while net income advanced 17.1% from last year's quarter to €2.8 billion ($3.1 billion).

Net income per ordinary share also moved up 19.2% from the year ago figure to €7.15. ASML's balance sheet remained in excellent shape, with cash and cash equivalents totaling €8 billion ($9.1 billion) at the end of the quarter.

Management highlighted that order intake continues to run at a very strong pace, reflecting robust customer demand across the board. The company remains closely aligned with customers to support that demand through a combination of new system deliveries and performance upgrades across its installed base.

These favorable business dynamics have reinforced management's expectation that 2026 would deliver another year of growth across all of ASML's businesses. The management expects Q2 FY2026 total net sales to range between €8.4 billion ($9.6 billion) and €9 billion ($10.3 billion), with gross margin projected between 51% and 52%.

Strong demand trends have also kept the company's broader outlook on solid footing. The company now projects total net sales for 2026 to land between €36 billion ($41.2 billion) and €40 billion ($45.8 billion), alongside a gross margin ranging from 51% to 53%.

Analysts are also increasingly upbeat on the company's earnings trajectory. They forecast Q2 FY2026 EPS to surge 75.4% YOY to $7.98. For the full year, they project earnings growth of 31.3% to $36.69, followed by another 35.1% leap to $49.55 in FY2027.

What Do Analysts Expect for ASML Holding Stock?

Wells Fargo is not the only firm growing more enthusiastic about ASML. Demand for the company’s EUV systems continues to strengthen the long term earnings story. Analyst Didier Scemama at BofA raised his price target to $2,345 from $2,268 while maintaining a “Buy” rating.

The firm expects ASML’s order book for 2027 to be fully spoken for by the time management reports second quarter results on July 15. Such a development could prompt investors to shift their attention toward 2028 earnings potential.

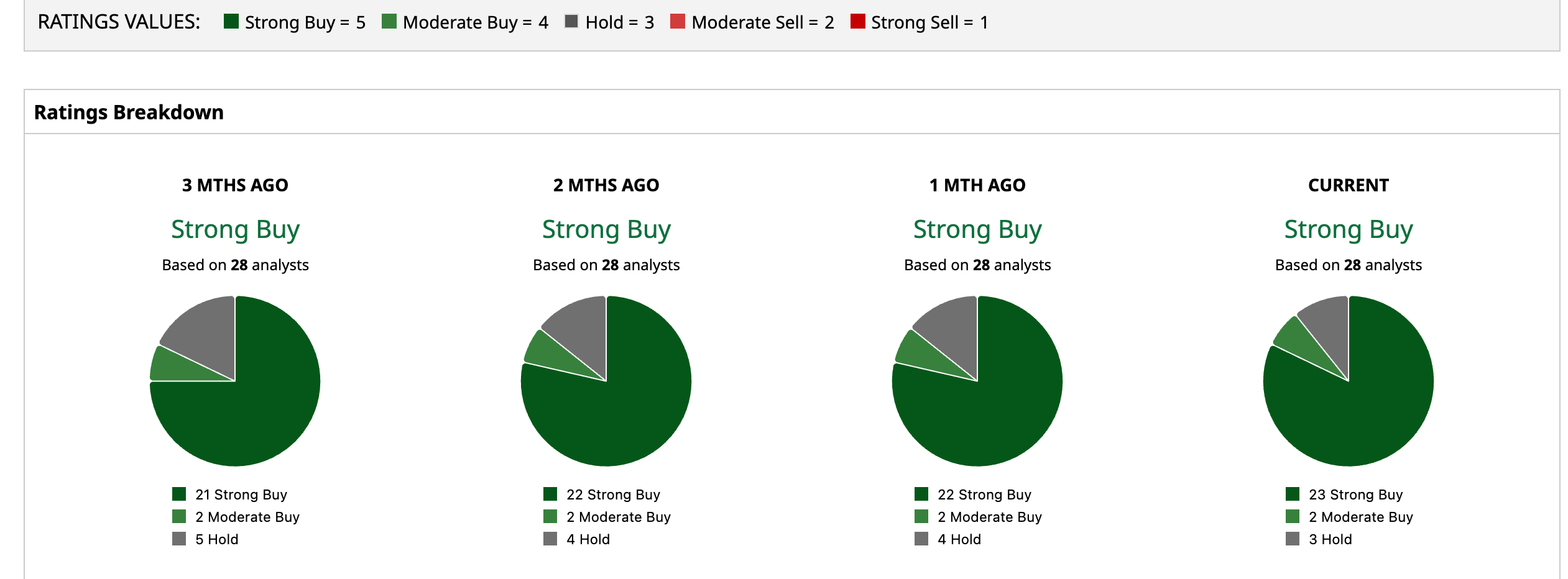

Analyst sentiment now leans heavily in ASML’s favor with an overall rating of “Strong Buy.” Among 28 analysts covering the stock, 23 recommend “Strong Buy” ratings, two analysts carry “Moderate Buy” ratings while three analysts remain on the sidelines with “Hold” ratings.

To that end, the stock is already trading above its average price target of $1,765.44. However, the Street-High target of $2,268 suggests a gain of 27.9% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)