/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

Celestica (CLS) is growing faster than most investors currently realize. Yet, it doesn’t get the limelight it deserves. Often manufacturing and infrastructure partners for large tech companies that work behind-the-scenes get overlooked. But Celestica is no longer just assembling hardware for customers across end markets. It is becoming a key supplier to hyperscalers building next-generation AI data center infrastructure.

Let's examine the reasons Celestica deserves a spot in your portfolio.

About Celestica

Celestica doesn’t mainly sell a consumer product under its own brand. Instead, it helps other companies design, build, assemble, test, and supply complex technology products and systems. It operates through the following two business segments.

- Connectivity & Cloud Solutions (CCS): Builds hardware used by hyperscalers, cloud providers, and data center customers, including products tied to AI workloads and cloud computing.

- Advanced Technology Solutions (ATS): Celestica’s more diversified piece, tied to Aerospace & Defense, Industrial, HealthTech, and Capital Equipment, which includes semiconductor equipment and other specialized industrial/technology equipment.

The CCS Engine Is Doing the Heavy Lifting

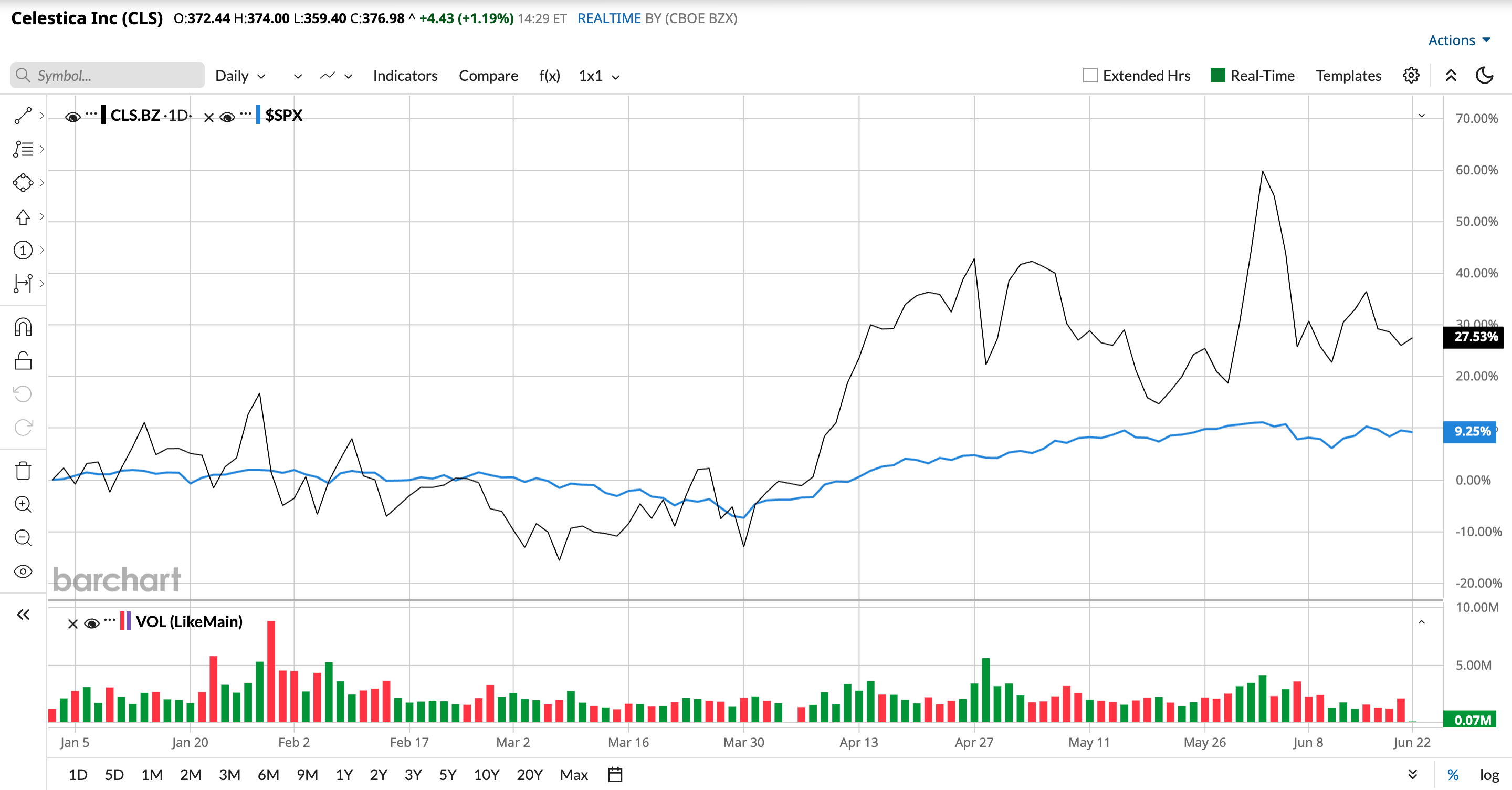

Celestica kicked off 2026 with one of the strongest quarters in its recent history. Its first quarter numbers were extraordinary, yet the stock performance doesn’t reflect that. CLS stock has surged 25.68% year-to-date (YTD), compared to the broader market gain of 9.28%. In the first quarter, revenue increased 53% year-over-year (YOY) to $4.05 billion, while adjusted earnings per share (EPS) surged 80% to $2.16, exceeding the high end of management’s forecast.

The CCS segment is doing most of the heavy lifting for the company as its fastest-growing division. It reported 76% YOY growth in revenue to $3.24 billion, accounting for 80% of total revenue. In the segment, communications end market rose 69%, with the main driver being 800G networking switches, which saw huge demand from Celestica’s largest hyperscaler customers. The enterprise end market reported a 101% YOY increase, driven by the planned ramp of a next-generation AI/ML compute program with a hyperscaler customer.

To further boost the growth of the CCS segment, Celestica expects to begin mass production on 1.6T switch programs with two hyperscaler customers in the second half of 2026. Furthermore, Celestica is collaborating with Advanced Micro Devices (AMD) on the “design and manufacturing of a scale-up networking switch for the Helios rack-scale AI architecture.” The company also secured a “design and manufacturing deal of a 1.6T co-packaged optics Ethernet switch with a hyperscaler customer," with mass production set to begin in 2027.

While the ATS segment recorded flat YOY growth in Q1, management expects mid- to high-single-digit percentage growth in 2026. This is likely to be fueled by a resurgence in client demand for its capital equipment business. At the midpoint, management predicts a 49% increase in revenue to $17 billion to $19 billion, with a 68% increase in adjusted earnings per share for the full year 2026.

Heavy Spending Is Backed by Real Deals, not Just Hope

This year, capital spending has been a matter of concern for AI investors. However, Celestica’s capital spending of $230 million in the quarter was justified by meaningful results. The company expects capital spending of roughly $1 billion for the full year to support CCS growth, which will be fueled by strong demand from hyperscalers. Importantly, management also reaffirmed its 2026 free cash flow outlook of $500 million, despite a heavy investment cycle. The balance sheet also looks capable of supporting the expansion. At the end of Q1, Celestica had $378 million in cash and $719 million in gross debt

Currently, Celestica stock doesn’t look outright expensive if the company can deliver on the growth Wall Street expects. Based on its estimated earnings growth of 70.56% for 2026, the stock is trading at 39.22 times forward 2026 earnings. Analysts even expect a 45% increase in EPS to $14.96. That is no longer a cheap multiple for a contract manufacturer. However, Celestica is no longer being valued like a traditional electronics manufacturing stock. Investors will be paying a premium for a company tied to hyperscaler AI networking, AI compute, and data center infrastructure, with revenue and earnings still growing at an unusually fast pace. For existing long-term investors, it would be wise to hold on to this AI stock. New investors may want to wait for a better entry point to invest with a margin of safety.

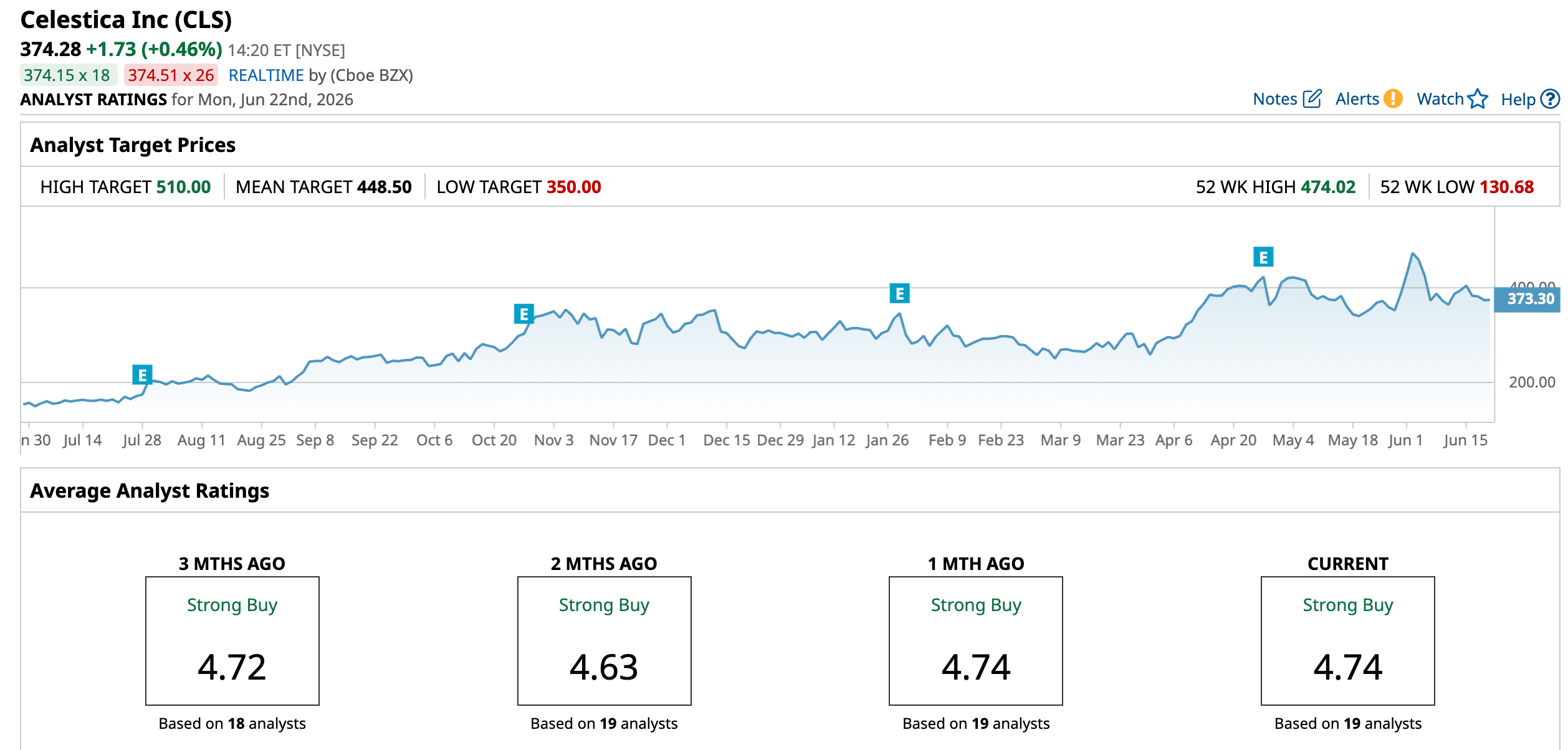

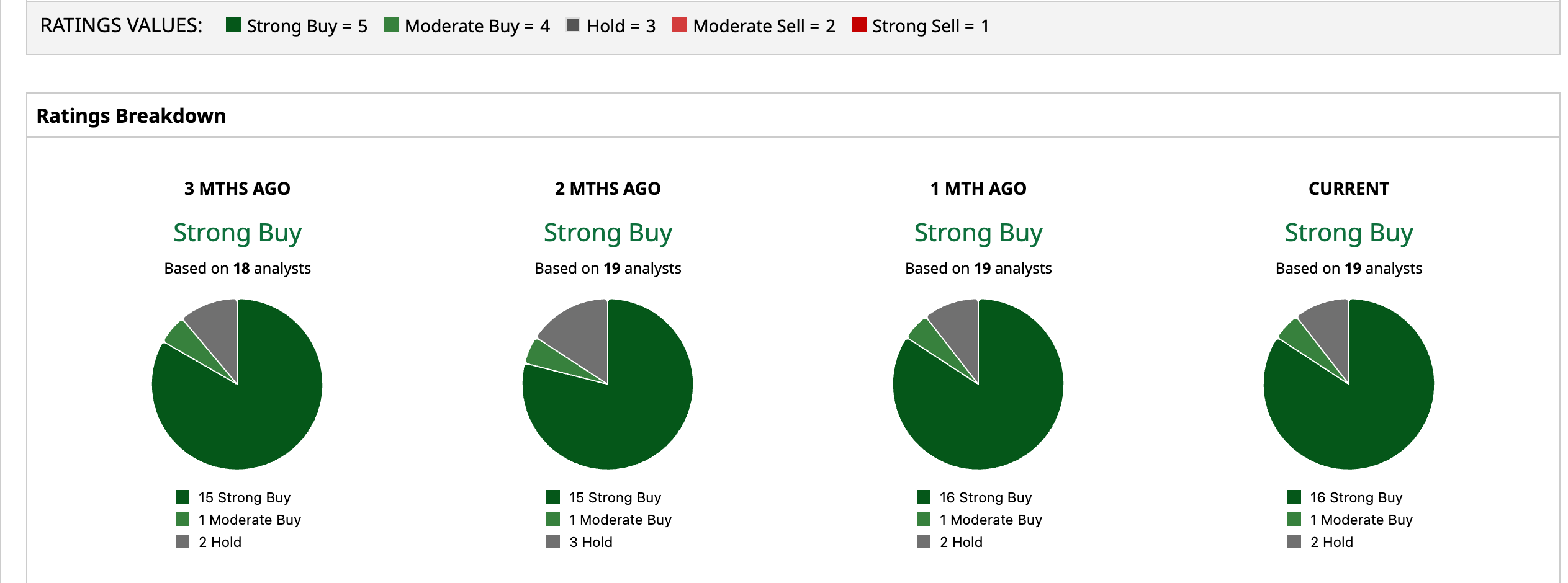

Overall, Celestica holds a consensus “Strong Buy” rating. Of the 19 analysts covering the stock, 16 rate it a “Strong Buy,” one says it is a “Moderate Buy,” and two rate it a “Hold.” The average target price of $448.50 suggests the stock can climb another 19.8% from current levels. Plus, the high price estimate of $510 implies the stock has an upside potential of 36.3% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)