Pennsylvania-based Universal Health Services, Inc. (UHS) is one of the largest healthcare providers in the United States, operating a broad network of hospitals and care facilities across multiple markets. Through its subsidiaries, the company delivers a wide range of healthcare services, including acute care, behavioral health, outpatient treatment, and ambulatory care. The company’s market capitalization stands at roughly $8.55 billion.

Companies with market capitalizations below $10 billion are generally categorized as mid-cap stocks, and Universal Health Services comfortably falls within that group. With a significant presence spanning the U.S., Puerto Rico, and the United Kingdom, UHS has established itself as a major player in the healthcare industry, serving millions of patients through its extensive and diversified care platform. Despite its sizeable presence in the healthcare sector, the stock has faced intense selling pressure in recent months.

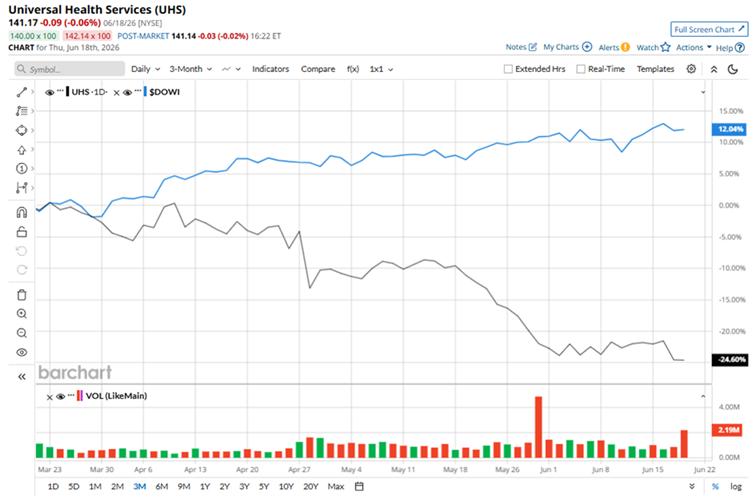

Shares currently trade about 42.7% below their 52-week high of $246.32, reached in November last year, underscoring the magnitude of the downturn. The weakness has been particularly pronounced in the near term. Over the past three months, the stock has plunged 25.5%, sharply underperforming the broader Dow Jones Industrial Average ($DOWI), which has advanced 12% during the same period.

The longer-term picture is equally challenging. The shares have fallen 35.3% year-to-date in 2026 and are down 17.6% over the past 12 months. By comparison, the Dow has gained 7.3% so far this year and delivered a robust 22.3% return over the past year, highlighting the stock's significant underperformance against the broader market.

The technical backdrop remains firmly bearish. Since early March, the stock has consistently traded below both its 50-day and 200-day moving averages, a signal that reflects sustained downward momentum and weak investor sentiment.

Universal Health delivered a strong operational performance for the first quarter of 2026 on Apr. 27. Net revenues grew 9.6% year-over-year to $4.50 billion, beating Wall Street's expectation of $4.39 billion, while adjusted net income jumped to $5.65 per share, up from $4.80 in Q1 2025, topping the analyst consensus of $5.46. Top-line growth was propelled by robust demand across both operating divisions, with same-facility revenue rising 8.2% in acute care and 7.3% in behavioral health, largely due to solid pricing and favorable reimbursement trends that helped offset softer, weather-impacted seasonal volume.

The stock's struggles become even more apparent when compared with industry heavyweight HCA Healthcare, Inc. (HCA). Although HCA has experienced some pressure, its shares have declined only modestly over the past year and are down 19.6% year-to-date. In contrast, UHS has posted significantly steeper losses across both time frames, highlighting its weaker performance relative to a key healthcare peer

Despite the stock's prolonged slump, Wall Street hasn't completely given up on UHS. In fact, analysts remain broadly optimistic about its long-term prospects, with the stock currently carrying a consensus "Moderate Buy" rating. Among the 20 analysts covering UHS, the average price target stands at $216, implying a potential upside of 53% from current levels.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)