Western Digital (WDC) shares printed a new all-time high on June 16 after a senior Morgan Stanley analyst, Joseph Moore, aggressively raised his price target on the data storage giant to $650.

As Moore reiterated his “Overweight” rating this morning, WDC’s relative strength index (14-day) climbed into the mid-70s, indicating overbought conditions that often precede a near-term pullback.

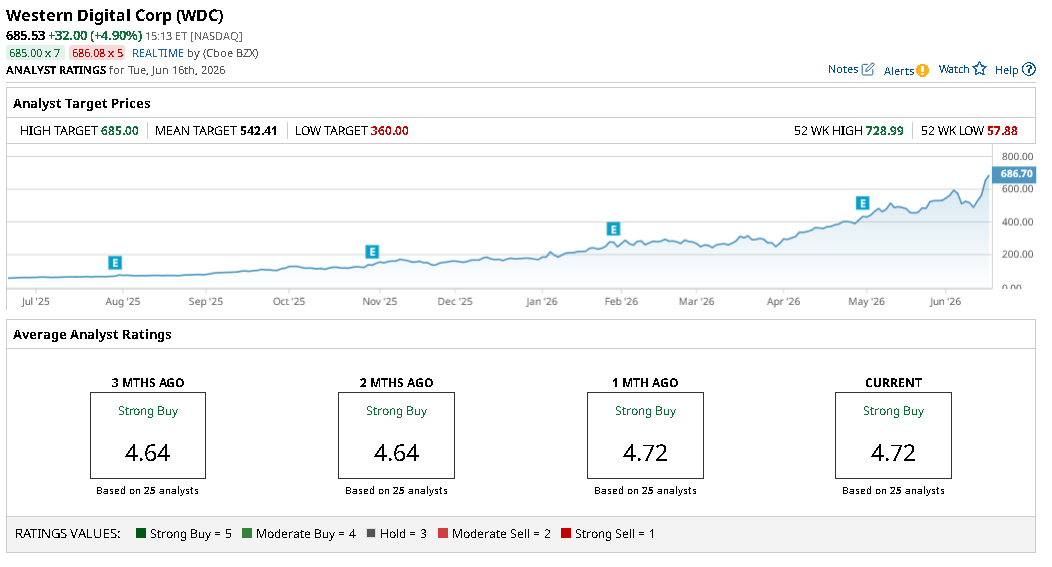

Western Digital stock has been a blockbuster investment in 2026, currently up about 250% versus the start of this year.

AI Demand Makes Western Digital Stock Worth Owning

Moore’s constructive call on WDC shares is rooted in the artificial intelligence (AI) infrastructure’s hardware demands.

According to him, complex AI modeling, machine learning applications, and expanding hyperscale data centers are seeing storage demand compound at an annual clip of at least 40%.

And as a major, vertically integrated supplier of enterprise-grade storage solutions, Western Digital is uniquely positioned to capture this windfall.

In short, Morgan Stanley is positive because the market is waking up to the reality that processors or GPUs alone can’t power the AI revolution; high-tier memory architecture is just as critical.

Upcoming Rollouts to Drive WDC Shares Higher

Following deep, industry-wide production cuts over previous cycles, manufacturing is wrestling to keep pace with the massive AI-driven resurgence of enterprise orders in 2026.

This structural bottleneck has handed WDC immense pricing power, allowing the HDD maker to win upward adjustments to its contractual pricing structure, Moore wrote in his research report.

He recommended sticking with Western Digital shares also because the highly anticipated rollouts of high-capacity UltraSMR and HAMR architecture could supercharge the firm’s operating margin over the next two years.

Why Caution is Still Warranted in Playing Western Digital

Investors are still recommended caution as WDC stock already sits handily above Moore’s, or any other Wall Street analyst’s price target at writing.

While the consensus rating on Western Digital remains at “Strong Buy,” the mean price target of about $542 signals massive downside potential from current levels.

Moreover, WDC’s meteoric run and its stretched valuation (about 58x forward earnings) are starting to turn options pricing against it as well.

The put-to-call ratio on contracts expiring July 24 sits at 1.7x currently — indicating a strong bearish skew — with the lower price on those contracts also warning of a potential crash to $551 over the next four to six weeks.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)