/The%20Adobe%20logo%20on%20a%20smartphone%20screen%20by%20filins%20via%20Adobe%20Stock.jpeg)

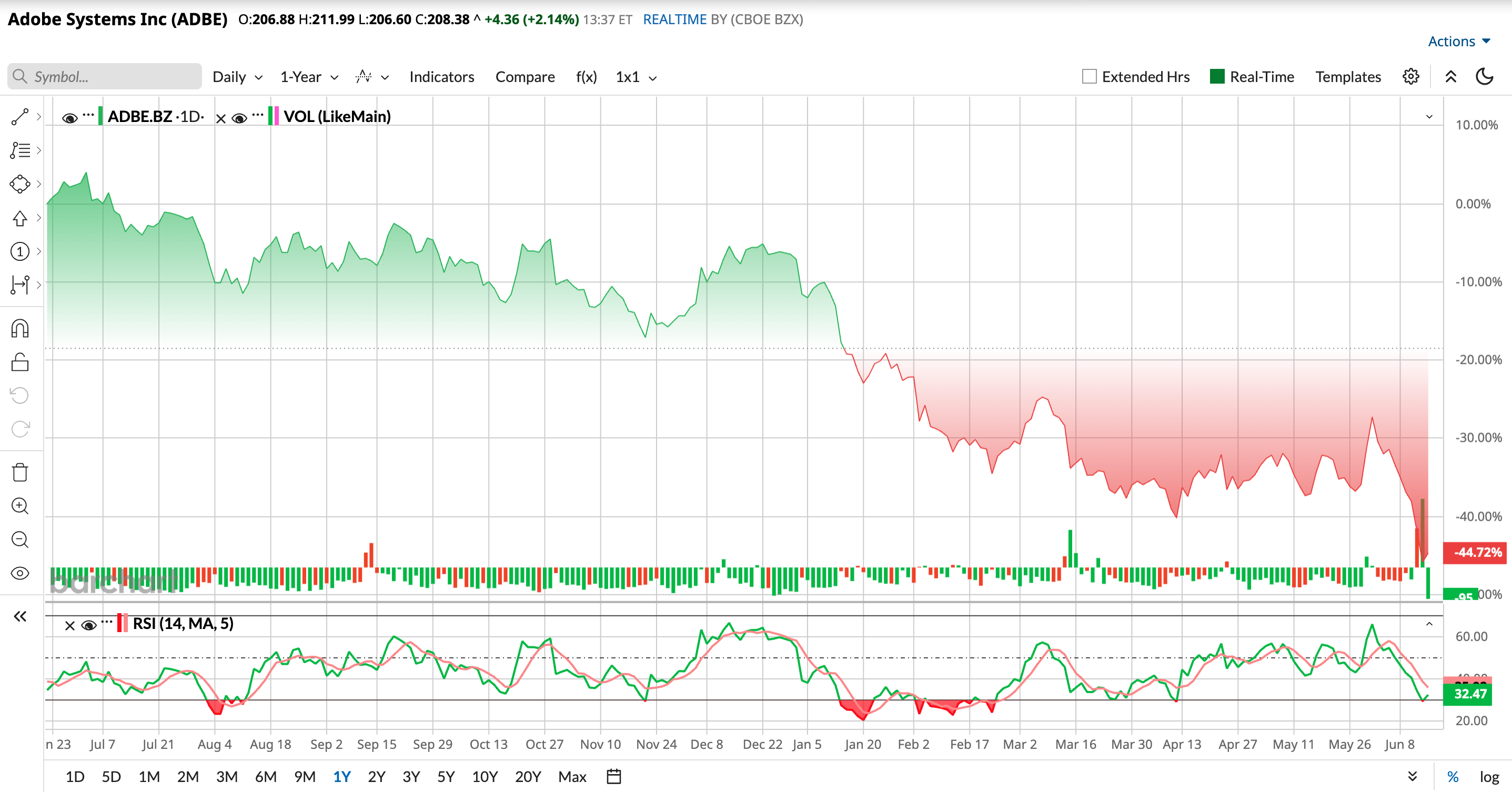

Adobe (ADBE) fall from grace has been striking. Once one of the market’s most reliable software winners, the stock is now trading near levels last seen in early 2019, giving back nearly all of its pandemic-era and AI-era gains. From a technical standpoint, the picture has steadily worsened.

Shares have remained trapped in a long-term downtrend since peaking in 2021, with each rally producing lower highs. The sell-off last week pushed Adobe below the key $225 support zone that had held several times over the past year, leaving the stock vulnerable to a test of the next support area around $200 to $220.

What’s surprising is that the decline is not being driven by weak business performance. Adobe delivered another record quarter, with Q2 revenue rising 13% annually and the bottom line topping expectations. Instead, investors are focused on several concerns.

The rapid rise of generative AI has fueled fears that new competitors could challenge parts of Adobe’s creative software empire. Meanwhile, Adobe’s decision to expand its freemium strategy has raised questions about near-term subscription growth. Leadership uncertainty has only added to the pressure. CFO Dan Durn is departing, CEO Shantanu Narayen is preparing to step down, and investors appear reluctant to give Adobe the benefit of the doubt until a new leadership team is firmly in place.

With sentiment scraping the bottom and the stock hovering near key support, what needs to happen for the bulls to regain the upper hand? Let’s dig into Adobe’s latest results, challenges, and potential catalysts.

About Adobe Stock

Founded in 1982 and headquartered in San Jose, California, Adobe has grown into one of the world’s leading software companies, helping people create, edit, and share digital content. The company built its legacy through innovations such as PostScript printing technology, Photoshop, and the PDF format, which became a global standard for digital documents.

Beyond creative software, Adobe also serves businesses through its Experience Cloud platform, offering marketing, analytics, and customer experience solutions. Today, Adobe’s products are used by millions of creators, professionals, and enterprises worldwide. The company is also embracing the artificial intelligence (AI) revolution through its Firefly generative AI platform, which has already generated billions of images. Adobe currently has a market capitalization of $82.5 billion.

While Adobe is investing heavily to position itself for the AI era, investors have yet to fully embrace that story. Instead, many wonder whether Adobe will emerge as a winner in AI, or will a new generation of AI-powered tools chip away at its dominance in creative software. That skepticism has taken a toll on the stock. Adobe’s shares are now trading near multi-year lows and rank among the worst-performing stocks in the S&P 500 Index ($SPX) this year. ADBE stock is down 40.8% year-to-date (YTD).

The stock has fallen roughly 64% over the past five years, is down 47.1% over the last 52 weeks, and sits 48.6% below its June 2025 high of $405. Even more recently, shares have tumbled 15.39% in just the past five trading sessions.

Ironically, the latest sell-off came right after Adobe delivered a strong second-quarter earnings report. Revenue, earnings, and guidance all topped expectations, but investors were more focused on management changes than financial results. The company announced the departure of its CFO, adding to concerns that surfaced earlier this year when longtime CEO Shantanu Narayen revealed plans to step down.

Losing both a CEO and a CFO within a span of three months is rarely viewed positively by the market. Even though Adobe’s business remains strong, leadership uncertainty has created another reason for investors to stay on the sidelines.

The chart shows a stock that's still under pressure, but a few cracks may be forming in the downtrend. Trading activity has picked up as investors step in after the recent sell-off. At the same time, the 14-day Relative Strength Index (RSI) has slipped very near into oversold territory, a sign that pessimism is running high and sellers may be starting to run out of steam.

When it comes to valuation, Adobe looks surprisingly cheap. Despite posting record revenue, growing its AI business, and generating billions in cash flow, the stock still trades at just 8.39 times forward adjusted earnings and 3.12 times sales. Those multiples sit well below both its historical averages and many peers. The market is pricing Adobe more like a mature software company than a business that's still finding new growth drivers through AI.

Adobe Beats Q2 Street Estimates

The company reported its fiscal second-quarter 2026 report on June 11, and it delivered record Q2 revenue of $6.62 billion, up 13% year-over-year (YOY). Non-GAAP EPS rose 17.8% annually to $5.96, comfortably ahead of Wall Street's expectations. Management credited the strong performance to healthy subscription bookings, solid revenue conversion, and growing demand for its AI-powered products across both consumers and enterprise customers.

The business continues to be powered by subscriptions. Subscription revenue reached $6.42 billion, accounting for nearly 97% of total revenue and growing 13.7% YOY. Product revenue contributed $89 million, while services and other revenue amounted to $113 million.

Perhaps the biggest highlight was Adobe’s AI business. The company’s AI-first annual recurring revenue more than tripled from a year earlier, surpassing the $500 million mark. Total Adobe ARR reached $27.1 billion at quarter-end, including roughly $480 million added through the Semrush acquisition.

Meanwhile, Adobe’s Remaining Performance Obligations, a measure of future contracted revenue, climbed to $22.27 billion, providing strong visibility into upcoming growth.

Adobe ended the quarter with $5.62 billion in cash and short-term investments and reduced its long-term debt to $4.8 billion. The company also generated a healthy $2.16 billion in operating cash flow, highlighting the strength of its underlying business despite continued investments in growth initiatives.

Also, Adobe’s strong performance prompted management to raise its outlook for both the current quarter and the full year. For Q3, the company expects revenue between $6.67 billion and $6.72 billion, with Business Professionals and Consumers subscription revenue projected between $1.87 billion and $1.89 billion. Creative and Marketing Professionals subscription revenues are expected to come in between $4.61 billion and $4.64 billion. And, Adobe expects non-GAAP EPS between $6.05 and $6.10.

Looking ahead to fiscal 2026, Adobe now expects total revenue of $26.5 billion to $26.6 billion. The company forecasts Business Professionals and Consumers subscription revenue of $7.44 billion to $7.48 billion, while Creative and Marketing Professionals subscription revenue is expected to reach $18.21 billion to $18.27 billion. Furthermore, Adobe raised its full-year non-GAAP EPS outlook to $24.35 to $24.45 and expects ending ARR to grow 10.2% YOY.

Analysts tracking Adobe expect the company’s profit to reach $19.14 per share in fiscal 2026, up 11.3% YOY, and grow another 14.47% to $21.91 per share in fiscal 2027.

What Do Analysts Expect for Adobe Stock?

If Adobe’s latest quarter proved anything, it’s that investors are no longer focused solely on the company’s current performance, but on what comes next. The management mentioned the company would grow a bit more slowly this year. Investors are worried about how Adobe plans to monetize AI and whether that strategy could slow growth before it starts paying off.

JPMorgan still likes the stock and kept its “Overweight” rating, but lowered its price target to $340 from $420. The firm sees Adobe sacrificing some near-term subscription growth to pursue a much bigger AI opportunity down the road. The company lowered its outlook for organic ARR, a key subscription metric, by roughly two percentage points. In JPMorgan's view, Adobe is essentially trading short-term gains for long-term market share. The problem is that investors have little patience right now.

Goldman Sachs sees even more reason for caution. The firm maintained its “Sell” rating and $190 price target, arguing that Adobe is prioritizing user growth over immediate profits. Adobe is pouring resources into expanding the reach of Firefly, its AI platform, through a freemium model. While that could create more valuable customers over time, it also means lower ARR growth in the near term and potentially higher expenses tied to marketing, sales, and AI infrastructure.

Evercore ISI also turned more cautious, downgrading the stock to “In Line” from “Outperform” and cutting its target to $225 from $325. Analysts there believe Adobe’s explanation for slower growth is reasonable, but they argue investors are unlikely to embrace the story until the company completes its leadership transition. With the CEO preparing to step down and CFO departing, Evercore believes the market wants to see a permanent management team establish a clear strategy and prove it can execute.

Stifel reached a similar conclusion, downgrading Adobe to “Hold” from “Buy” and slashing its target to $200 from $350. The brokerage firm had expected steady improvements in subscription growth throughout the year, but Adobe’s new outlook suggests that won’t happen anytime soon.

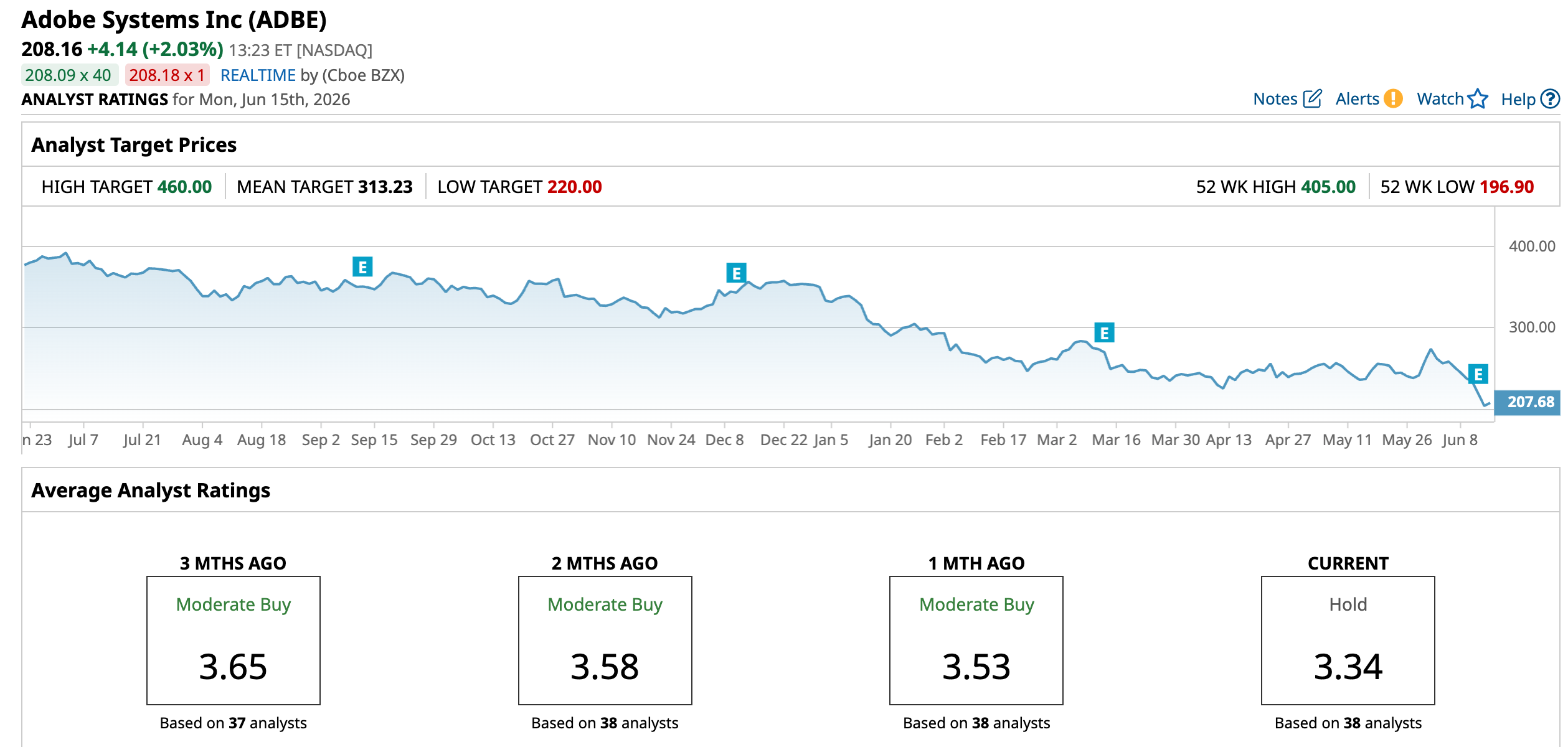

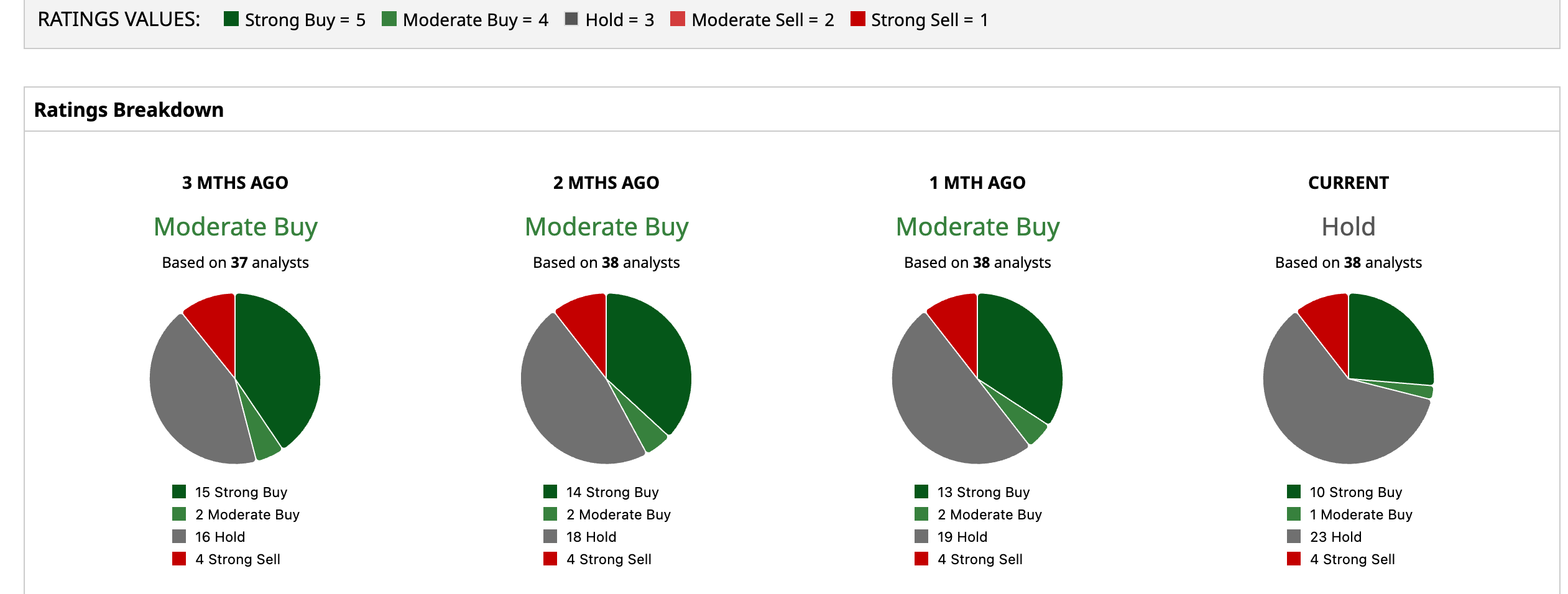

Adobe stock has a consensus “Hold” rating overall, a downgrade from a “Moderate Buy” rating a month back. Out of the 38 analysts covering the stock, 10 recommend a “Strong Buy,” one advises a “Moderate Buy,” 23 suggest a “Hold,” and the remaining four give a “Strong Sell” rating.

The mean price target of $313.23 suggests upside potential of 50.5% from the current price levels. The Street-high target price of $460 for Adobe implies the stock could rally as much as 121%.

Conclusion

So, what do Adobe bulls need to turn things around? Right now, it is less about the company’s numbers and more about changing the story investors are telling themselves.

Adobe continues to post solid results, generate strong cash flow, and trade at a valuation that looks inexpensive compared to its history. Yet the market remains unconvinced. Investors worry that AI could reshape the creative software landscape, while Adobe’s move toward a freemium model has raised concerns about near-term growth.

Leadership uncertainty is adding to the pressure. The abrupt departure of the CFO, with Steve Day stepping in on an interim basis, and the ongoing search for a successor to long-time CEO Shantanu Narayen have unsettled investors. Bulls need a permanent, highly capable leadership team that can restore confidence and clearly communicate Adobe’s long-term vision.

In the end, Adobe’s challenge is not performance, but it is perception. Until the company proves it can win in the AI era and removes the uncertainty around leadership, the stock may remain stuck in the penalty box. For patient investors, the opportunity remains, but a catalyst is needed before sentiment can truly change.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)