Centene has been on fire lately. In the past six months alone, the company’s stock price has rocketed 60.4%, reaching $64.89 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Centene, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Centene Not Exciting?

We’re glad investors have benefited from the price increase, but we’re sitting this one out for now. Here are three reasons you should be careful with CNC, plus one stock we’d rather own.

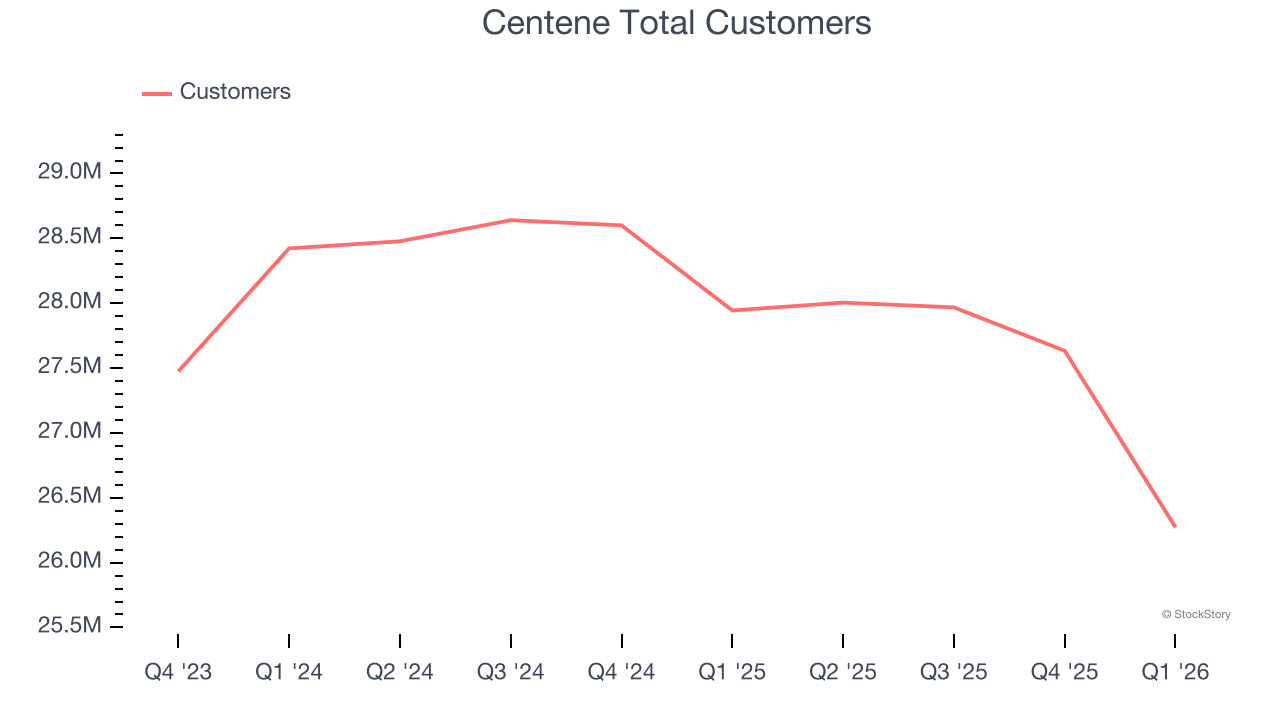

1. Declining Customer Base Reflects Product and Sales Weakness

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

Centene’s total customers came in at 26.27 million in the latest quarter, and over the last two years, their count averaged 1.8% year-on-year declines. This performance was underwhelming and shows the company lost deals and renewals. It also suggests there may be increasing competition or market saturation.

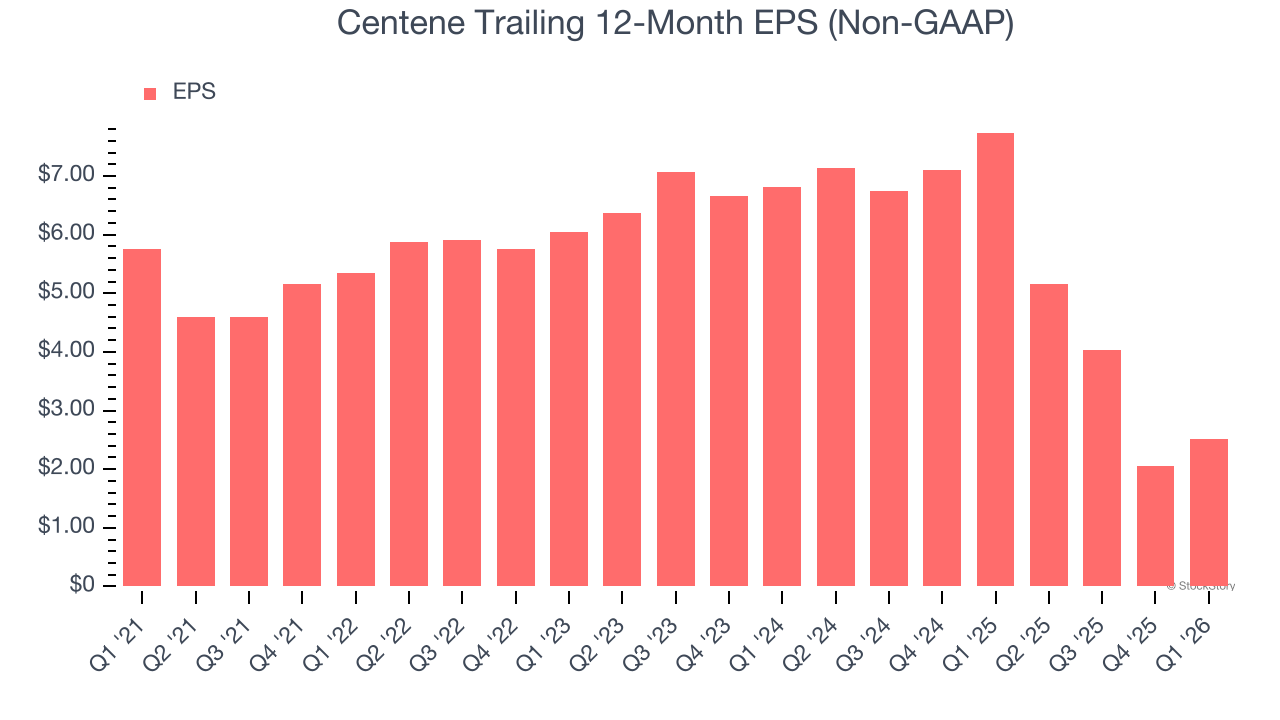

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Centene, its EPS declined by 15.2% annually over the last five years while its revenue grew by 11.5%. This tells us the company became less profitable on a per-share basis as it expanded.

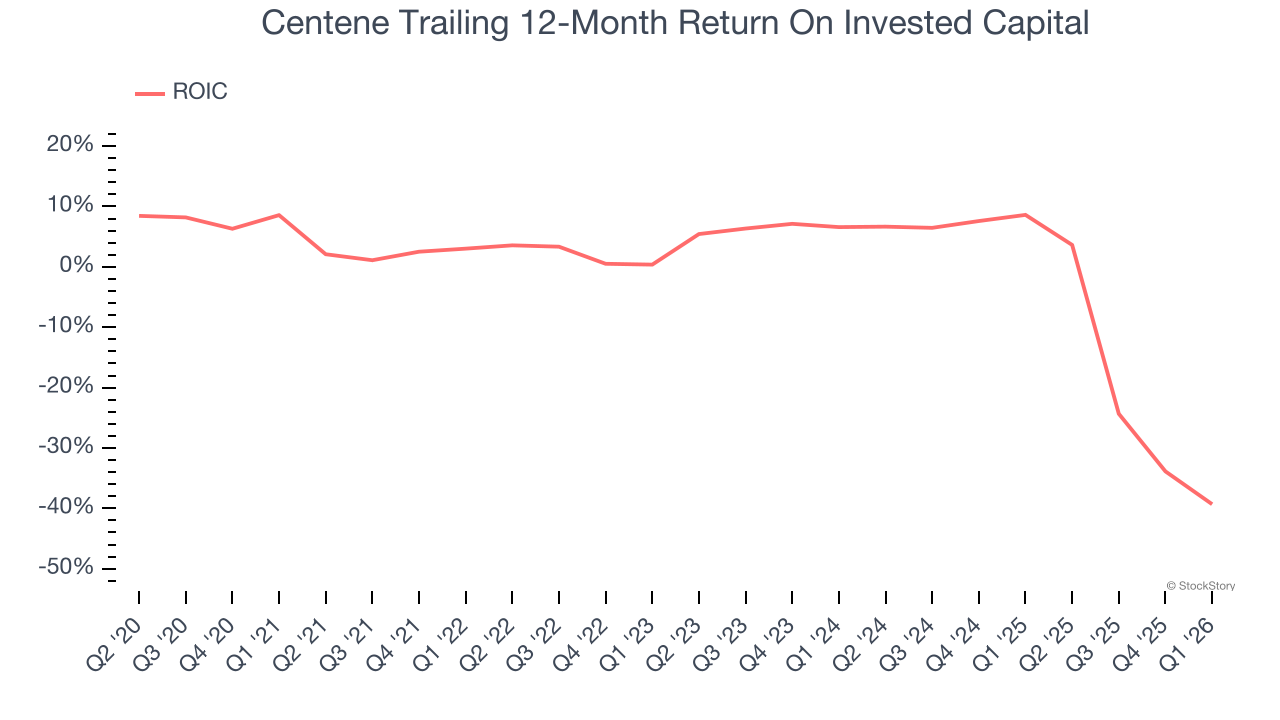

3. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

Over the last few years, Centene’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Centene isn’t a terrible business, but it isn’t one of our picks. Following the recent rally, the stock trades at 17.6× forward P/E (or $64.89 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Centene

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)